What I learned after reading the Pidilite Industries Q1FY25 Earnings Call.

Industry-wise

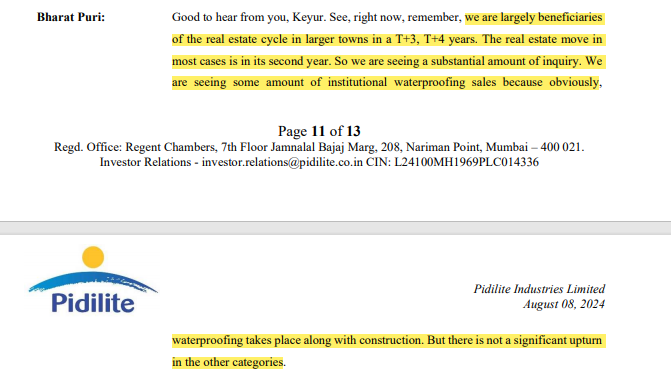

Investors should keep an eye on this. If it’s a widespread trend, it could impact other consumer goods companies too.

Could be a good sign for Pidilite’s bottom line. Let’s see how this plays out.

Company-wise

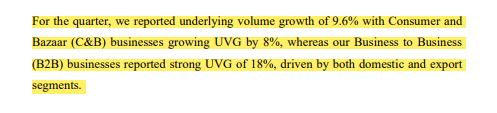

C&B at 8% is steady, but B2B shining with 18% is impressive. Exports & domestic demand driving the B2B engine. This is a positive sign for the company’s overall performance. Let’s see if this momentum can be sustained.

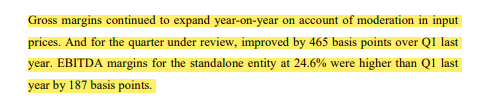

If this trend continues, Pidilite’s profitability could reach new heights.

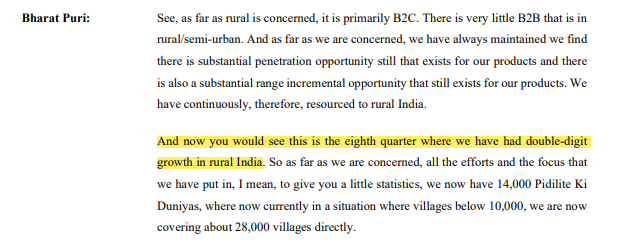

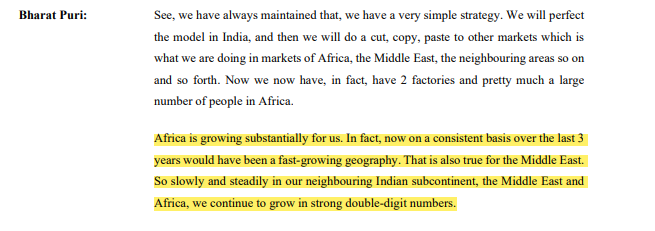

Eight quarters of double-digit growth is no small feat. This shows the increasing purchasing power in rural India and Pidilite’s strong distribution network.

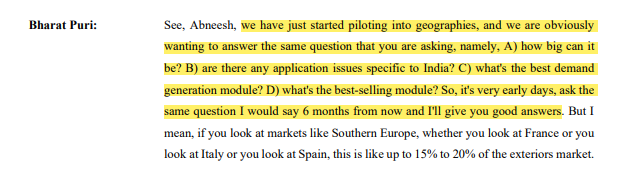

Pidilite’s new product launch is still in pilot mode. They’re playing it cautious, testing the waters.This is where the real work begins.

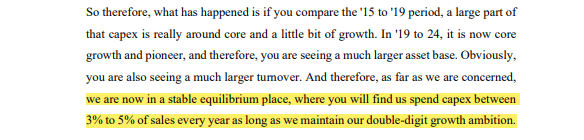

Pidilite’s capex plans are steady as she goes. 3-5% of sales for growth seems reasonable. This indicates a balance between expansion and financial prudence.

Let’s see how deep they can penetrate these markets.

| Subscribe To Our Free Newsletter |