The article makes some startling revelations:

Nearly everyone on the top management team made less than INR 20 lakhs a year at the time of the IPO, which is weird, given these guys’ work experience/qualifications. Perhaps we have a skewed idea of salaries, but you generally wouldn’t expect a CFO of an INR 600 crs + sales company (at the time of IPO) to make INR 12 lakh a year (the CFO is a wizened CA, which makes it even more surprising).

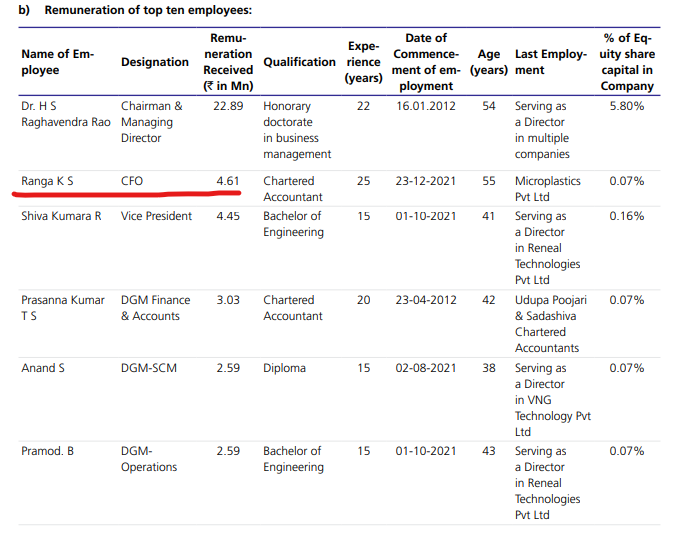

Quite surprising, given the company does not declare any dividends. Why would a top-management caliber person in electronics manufacturing want to work at such low salaries? I cross-checked this with the AR for FY23 and found that some of these findings are incorrect. As the image below indicates the CFO draws a salary of Rs 46 lakhs.

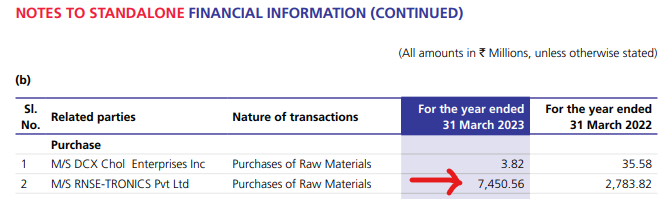

In FY22, around 25% of the raw materials were sourced from the promoter-owned firm, which promptly increased to 50% in FY23. Of INR 1200 crores in raw material costs, INR 700 crores seems to have been supplied by the promoter-owned firm.

This is correct. As per the FY23 AR around Rs 750 crores worth raw material was sourced from a promoter owned company.

This is a big red flag. Need to dig deeper into this. Usually such kind of things are done so that the majority of the “juice” is squeezed by the unlisted promoter owned entity. No wonder DCX has an OPM of only around 6% for FY24.

| Subscribe To Our Free Newsletter |