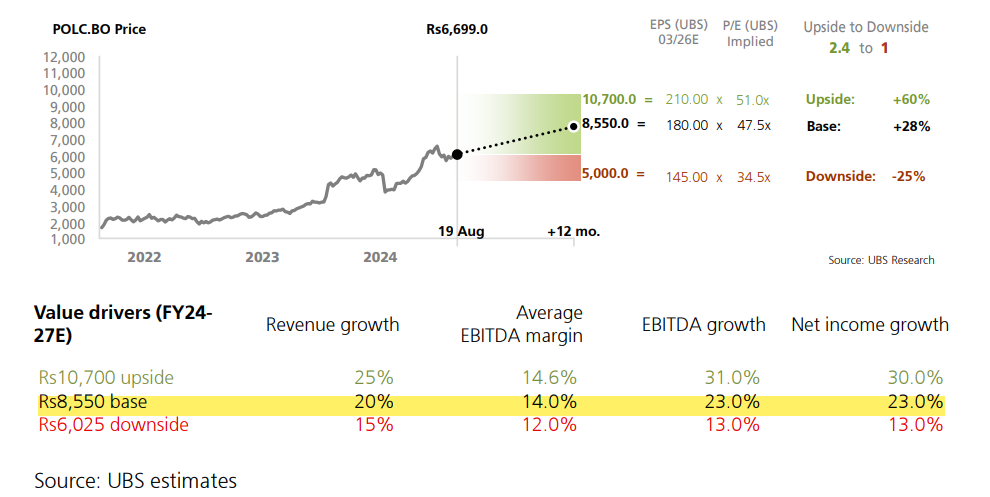

UBS has initiated research on Polycab and they have given target of 8,550 (25% upside in 1 year)

CMP – 6,800

Market cap – 1,02,000cr

P/E – 58 times

Key Points from Report –

- significant capacity expansion, allowing it to cater to a wide array of users;

- investment in distribution ramp-up, with advertising and sales promotion;

- a significant focus on institutional and B2B business.

Polycab’s strategy in the current growth-levered environment provides a significant edge, as evidenced by the company tracking ahead of its Rs200bn top-line target by FY26; Polycab may revise that target, with a strategic focus on long-term value creation.

- They forecast revenue/earnings growth of 20%/23% in FY24-27.

FY24 Revenue/PAT is of 18,000cr/1,800cr; they are expecting FY27E Revenue/PAT of 31,100cr/3,350cr.

FY27 Forward P/E – 30

Additionally company has guided for margin expansion in future.

| Subscribe To Our Free Newsletter |