I think below statement from the article will required to be closely watched;

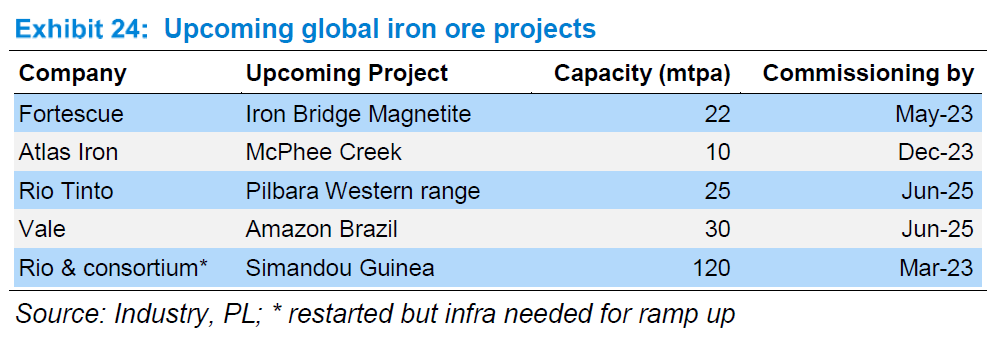

The slowdown in China comes, crucially, as a new generation of large, low-cost mines in Australia and Africa start production. That mix is the problem because it means the iron ore market, already oversupplied in the first half of this year, would remain in surplus in 2025, 2026, 2027 and probably 2028, too. Macquarie Bank Ltd., an Australian lender, says that the current surplus is “one of the worst” ever.

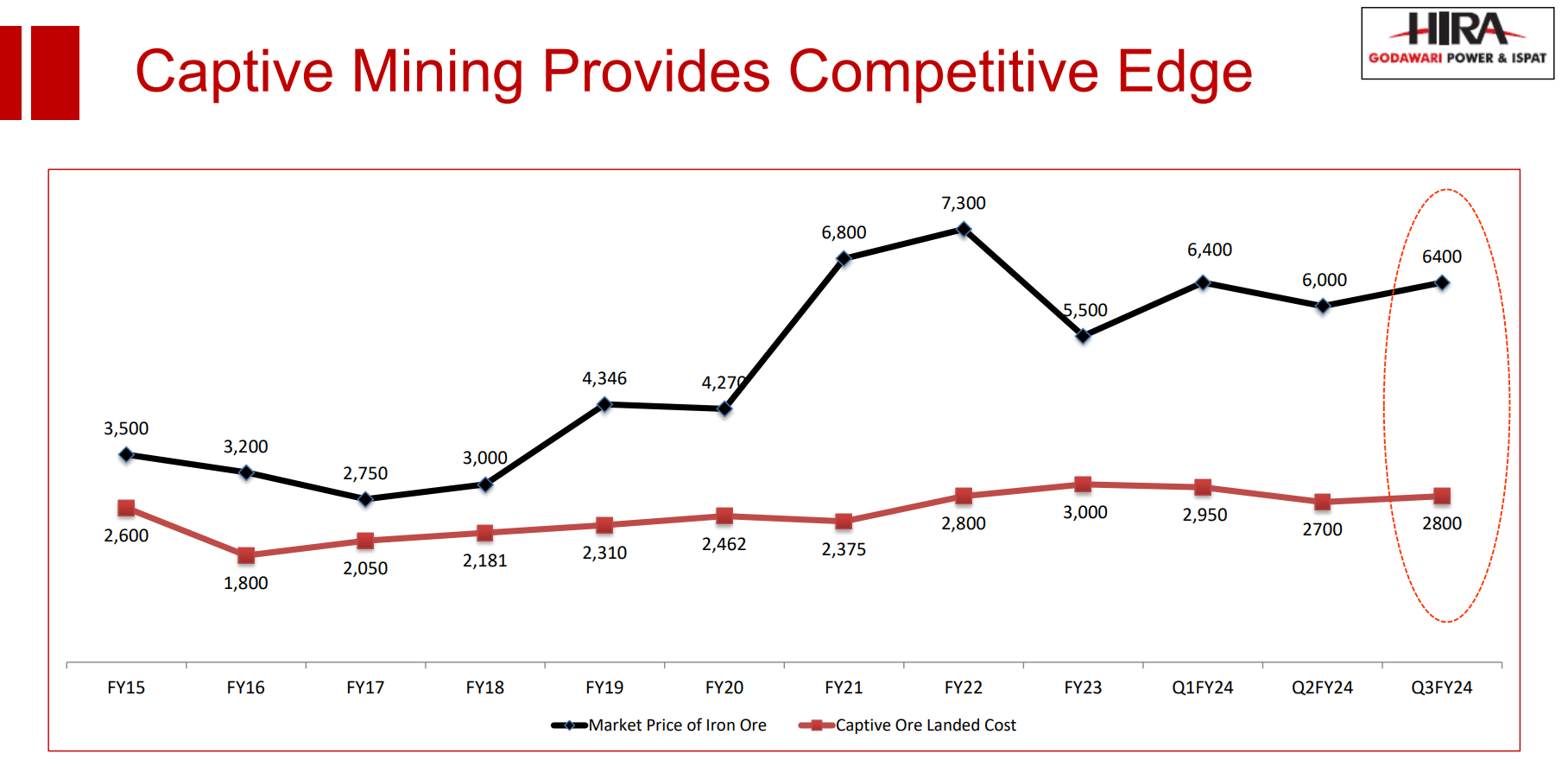

For GPIL the landed cost of captive iron ore is around 2800rs ($40).

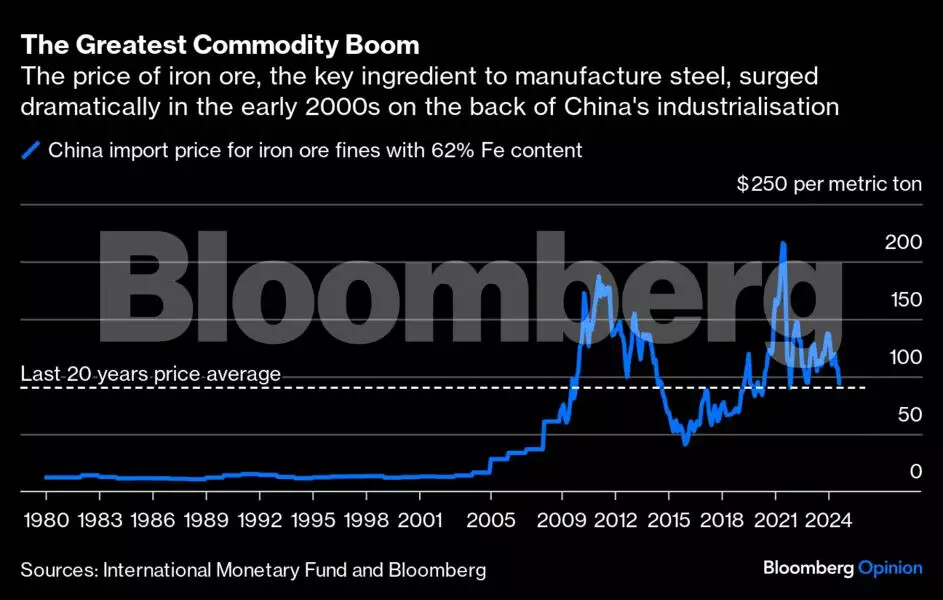

Currently the iron ore price is around $98.

Iron Ore – Price – Chart – Historical Data – News (tradingeconomics.com)

The article also pointed out that;

Over the medium-term, iron ore prices must drop to rebalance the market, pushing out high-cost miners. How low? It would depend a lot on whether the new mines come on stream on time, and whether the Chinese real estate sector recovers a bit.

In 2015-16, the prices dropped to $50 due to oversupply. Rio Tinto Plc., the world’s largest iron ore miner, digs the mineral out of the Pilbara region of Western Australia at a cost of about $21 a ton.

I think there is medium term risk to iron ore prices as pointed out in the article. There is higher probability of capital cycle playing out in this sector going forward.

However, GPIL is one of the low-cost producer having high grade Fe iron ore mines.

Disc: Invested & Biased. Not a mining expert or related to mining industry. Views are personal.

| Subscribe To Our Free Newsletter |