In my understanding, PI takes a portfolio approach to managing molecule concentration, with different molecules dominating revenues at various times. While competition for pyroxasulfone is imminent, PI has successfully navigated similar challenges in the past. Looking beyond pyro and agrochemicals, PI is now expanding into electronic chemicals and pharmaceuticals, which offer significantly larger addressable markets. I am more excited for PI’s journey now as they replicate their successful strategy in industries with far greater prospects than agrochemicals.

I am not good at understanding these macro shifts, I am more detail oriented and am generally looking for bets where I have better medium term visibility.

I bought Eureka because they are leaders in water purifier market which offers very higher gross margins. For e.g., most consumer durable cos make 30-35% GMs whereas water purifier cos make 50-60% GMs. This implies a possibility of higher operating and PAT margins at optimum utilization. Also, Eureka has been reporting double digit volume growth in last few quarters, when most consumer durable cos are struggling to grow. I feel new management is doing a decent job and there is a lot of value that they can create. Some data excerpts below on Kent’s financials (Eureka’s main peer) to show that potential PAT margins can exceed 15% in good times (super rare in consumer durable space).

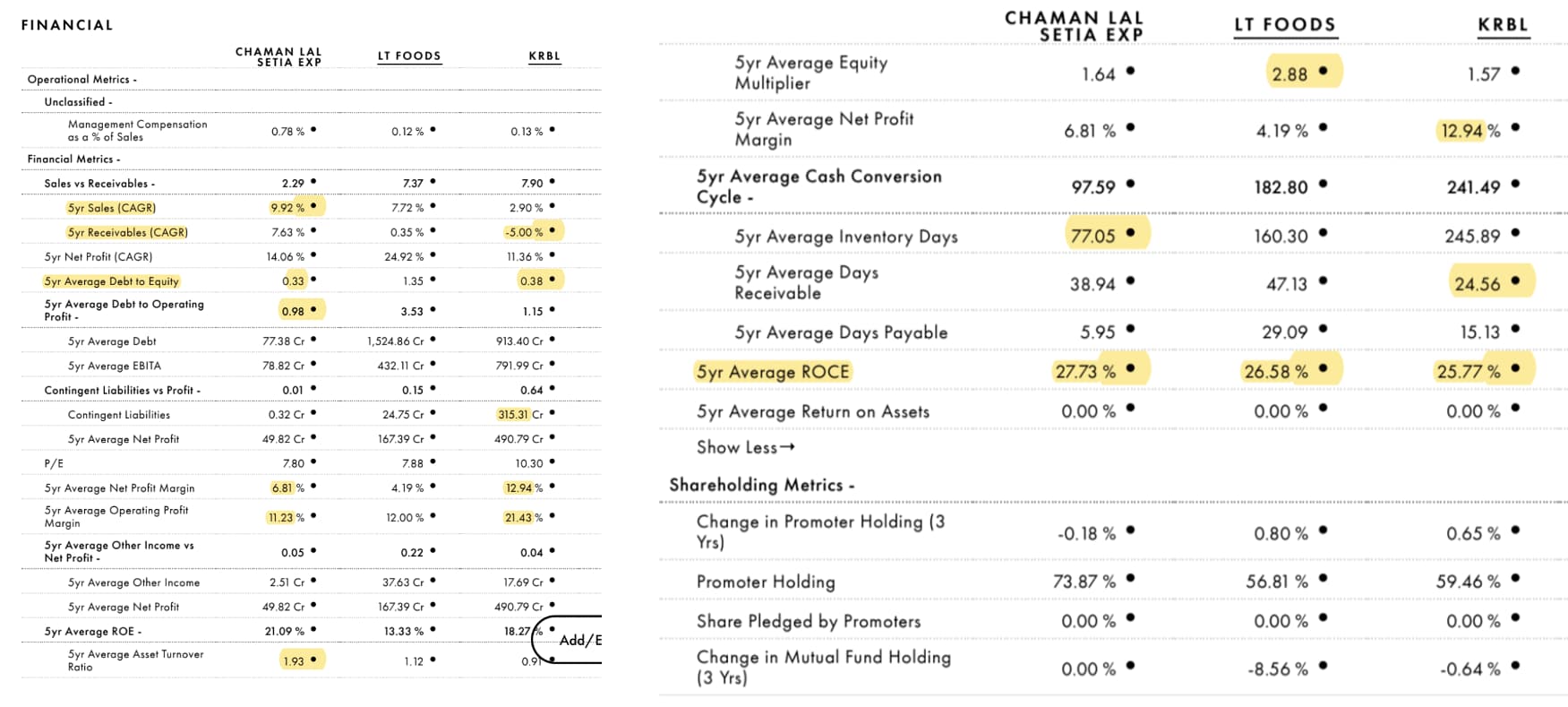

Yes, I still hold it and am excited by how management has opened up to investors and improved capital allocation (increased dividend payout to 10-15% + buyback). I feel with scale, more investors will see how well Chamanlal is managed. They make the highest ROICs, despite operating at lower margins than KRBL/LT foods. Managing inventories is the key in this business and they have done that very well.

Unfortunately, I have not been able to create much cash as I have found opportunities to deploy capital regularly. I have been selling a number of stocks which have done well (e.g. Godfrey, Nesco, HDFC AMC, Kaveri, Time techno, Ajanta, Amara, etc.) and reinvested in some new bets (e.g. Ambika cotton, Venky’s, AGI Infra, Gokul agro, Bharat rasayan, etc.). As a result, I have been unable to generate cash. I am also worried that in the next downturn, portfolio might see sharp drawdowns given how rewarding this upcycle has been. Lets see what future holds.

I cannot guarantee when I will be able to write the theses for some new bets, but I try and contribute to the respective thread (wherever possible).

| Subscribe To Our Free Newsletter |