It’s strange that this thread was inactive from past 4-5 months, don’t know the reason but I am assuming ” No earning surprise” in the last 8-10 quarters, was maybe the reason.

Q1FY25 brings some hope in terms of growth, where all other QSR players are facing demand headwinds, the Jubilant Foodworks has shown some sign of growth, in this challenging environment. The 45%YoY and 23% QoQ growth in revenue along with stable 20% margins and LFL growth came of 3.0% driven by Delivery LFL growth of 12.1%, shows some sign of revival in the business operation.

Key Takeaway from the Q1FY25 Concall:

Financial Performance

- Consolidated Revenue came in at INR 1933 Crores, up by 44.8% YoY

- EBITDA margins stood at 19.8%, INR 380 Crores against INR 277 Crores in Q1FY24.

- PAT stood at INR 61 Crores, upward QoQ: +56.9% YoY: +110.3%.

- Gross Margin of 73% at consolidated level.

India Segment

- In India, the revenue at INR 14.4 billion was up by 9.9% YoY. EBITDA margins at 19.3%

- Domino’s growth came in at 8.5% led by record high orders, registering 16% growth YoY.

- Domino’s India LFL growth came in at 3.0% driven by Delivery LFL growth of 12.1%

- Domino’s Mature Store ADS for 1,644 stores at ~INR 80,000 was also the highest in last five quarters.

- Launched ‘best value’ that a QSR chain offers a Lunch Thalia four-course meal at INR 99.

- Launched the globally acclaimed Domino’s Cheese Volcano pizza range meant for cheese lovers.

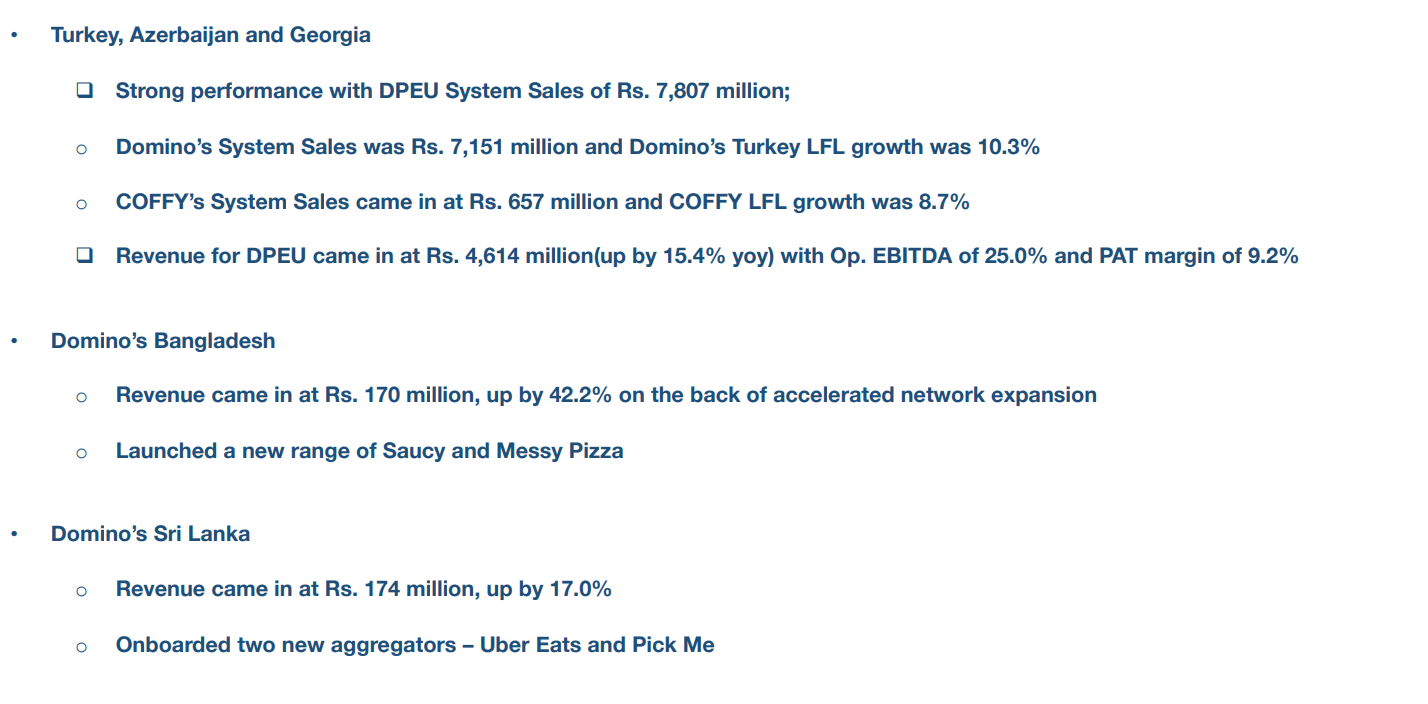

Turkey Segment

- Domino’s Turkey system sales came in at INR 7 billion and LFL was 10.3%. COFFY system sales came in at INR 656 million and LFL was 8.7%.

DP Eurasia

- The Revenue from DPEU came in at INR 4.6 billion, higher by 15.4% YoY at current currency rate. EBITDA margin came in at 25%

- PAT margin was strong and accretive to Indian business, at 9.2%.

Other Countries

Store Composition

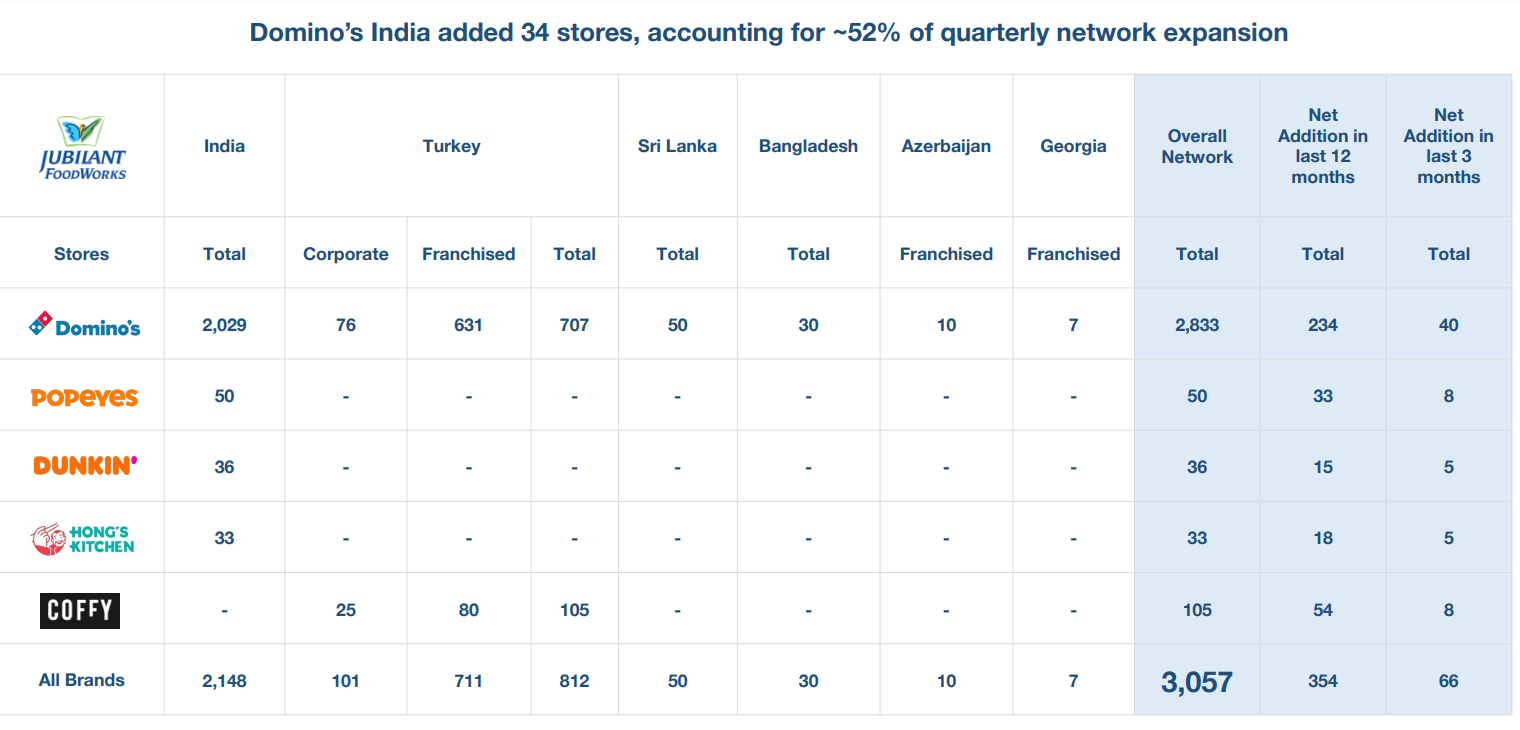

- Reached the milestone of 3000 stores across 5 brands and 6 countries. India’s contribution to Domino’s network at 10%.

- Crossed 100 COFFY stores in Turkey and 50 Popeyes stores in India.

Operational Performance

- The company acquired new customers at highest-ever rate, beating the industry trend.

- No price increase in the straight last 8 quarters also waived off the delivery fees.

- Across the world , delivery as a mix is growing. So there is also a consumer trend that Jubilant is also riding on. Delivery channel now contributes 69% in Q1FY25.

- Delivery channel revenue increased by 15.7% driven by Delivery LFL growth of 12.1% YoY, while Dine-in channel revenue declined by 5.7% YoY.

- Any store refurbish at least would see 10% to 12% growth in dine-in.

- Monthly active users has moved from 10.3 million to 12 million, which is almost 2 million customers we have added.

- Cheesy reward customers are now contributing 50% of business.

- In DP Eurasia (Turkey, Azerbaijan and Georgia), H2 is higher than H1.

- In Popeyes, the management has brought down the store size to fit it into the Indian kitchens.

- Domino’s India volume growth is about 16%, which is mainly on account of reduced threshold fees for delivery which is now only INR 150.

- Majority of the debt in DP Eurasia book is short term in nature.

- Management on any material change in the trend:

“Despite rains, despite heat, whatever the weather conditions we are seeing an uptick in delivery, and that’s what we are banking on.” - Bangladesh business turned profitable at the operating level. On the ongoing political unrest, management assures that staff is safe and company has not incurred any material loss.

- The company is looking to increase the ticket size by offering greater cheese and more indulgence to consumers.

- In Popeyes, the management is focusing on the chicken eating markets, that’s why more stores are in South India.

- In Popeyes, the company has high street locations to do deliveries. delivery share is lower and dine-in is higher at the moment.

- Dunkin is even more on track to kind of achieving high store-level profitability.

| Subscribe To Our Free Newsletter |