Q1FY25 Concall Highlights:

Financial Performance:

- Consolidated Revenue: INR 105.28 Crores, up 82% YoY

- EBITDA: INR 49.62 Crores, blended margins of 45%.

- Profit After Tax: INR 15.77 Crores. More than 5X as compared to Q1FY24

- Rental Segment Revenue: INR 66.79 Crores (63.44% of total revenue)

- Design & Build Turnkey Contracting Segment Revenue: INR 35.30 Crores (36.56% of total revenue)

Operational Performance:

Managed Office Business:

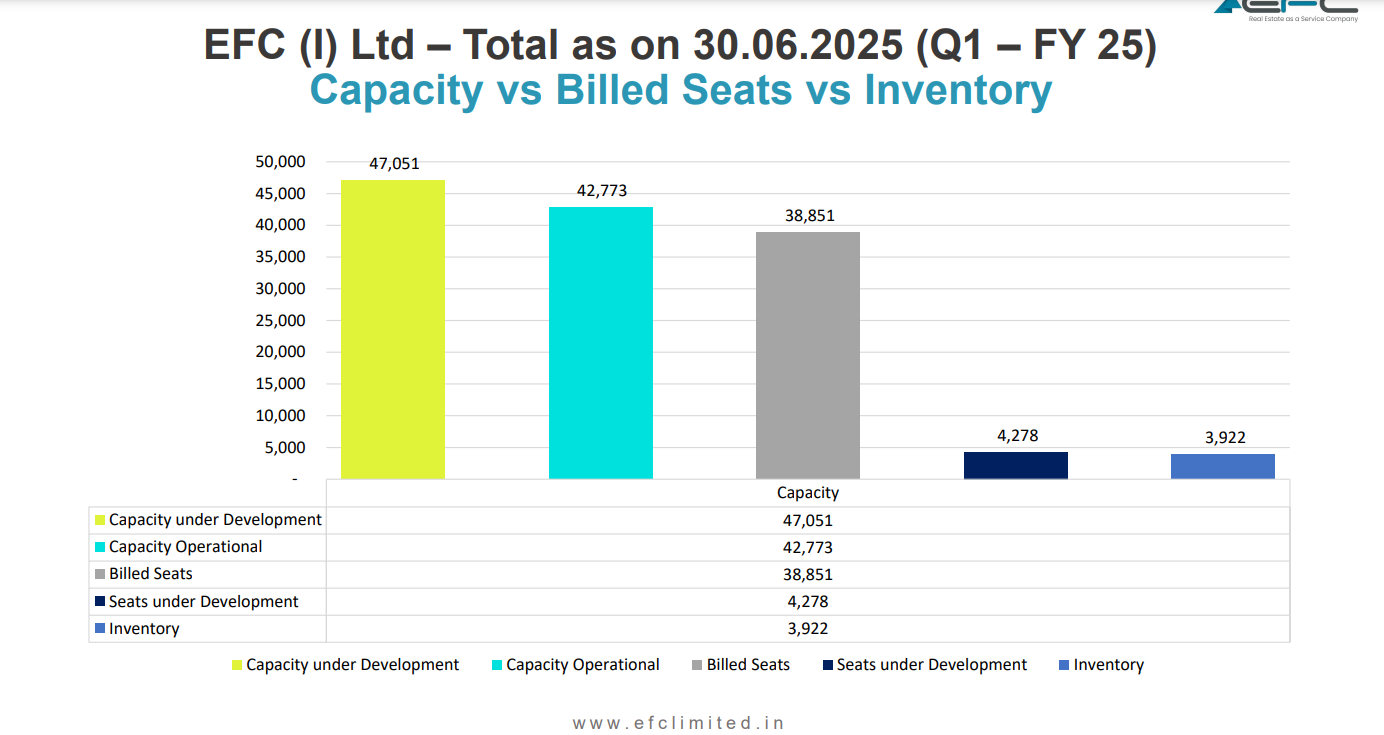

- Increased leasehold area by 300,000 sq ft across 7 centers in 4 existing cities.

- Added 7,000+ seats, bringing total seating capacity to over 47,000. By the end of this year, company will easily be around 65,000-70,000 seats.

- Acquired 80,000+ sq ft property in Pune for development and leasing.

Design & Build Division:

- Secured contracts exceeding INR 75 Crores across various sectors.

- Completed a 100,000 sq ft project for Coforge in 62 days.

- Currently negotiating contracts valued at over INR 100 Crores.

Furniture Manufacturing Segment:

- Secured regulatory approvals for a new manufacturing facility in Pune.

- Workforce of 200+ people.

- Production trials to commence in August 2024, with commercial production starting in September 2024.

- As per management, one simply cannot just bring capital and starts manufacturing of furniture, thorough understanding is required along with right blend of team.

Future Outlook:

- Target to double topline by FY25, with blended EBITDA Margins of 30%.

- Management sounds confident and ready for the next 3 years.

- Managed Office Business: Aiming to add 30,000-40,000 seats annually for the next three years.

- Design & Build Division: Confident in achieving year-on-year doubling of revenue.

- Furniture Manufacturing Segment: Projected to achieve INR 250-300 Crore topline by FY26. Commercial production is set to be launched by September 2024.

- This year, company is expecting INR 50-75 Crores contribution in topline from the furniture segment.

Other Important Points:

- REIT: Incorporated a real estate investment trust (REIT) with a corpus of Rs. 499 Crores. By the end of this month or beginning of September, EFC should get approval for the registration of their REIT.

- Inorganic Growth: Focusing on strategic acquisitions like Big Box.

- Competitive Landscape: Acknowledged increasing competition but believes in their integrated business model and pan-India presence.

- Acquired a 51% stake in Big Box Venture Private Limited. Big Box was already doing INR 2 Crores topline per month, with about 2800-2900 seats and since acquisition BB has added 2000 more seats.

- Bigbox Venture, has an impressive portfolio of over 3000 seats in Pune, is aggressively expanding into NCR region, Ahmedabad and Kolkata, significantly enhancing EFC overall market presence.

- The Pune acquired property will be used for managed office space only.

- As of now, focusing on nine prominent cities only ( NCR region, Bangalore, Hyderabad, Chennai, Gujarat, Ahmedabad, Bombay, Pune and Kolkata ), but going ahead EFC is also looking to expand in other cities as well, where certain developments are happening like Indore, Coimbatore and Chandigarh.

- One Instance shared by management:

- Management admitted that inorganic growth is necessary for any company in this space.

- Management on Acquisition Strategy:

- Management admitted that this space has no entry barrier, but to get to that efficiency level at which everybody like EFC is operating, that’s not going to be very easy for every new entrant and also to become a significant player.

- All the seats which are getting developed might not get occupied immediately, because there is a lag between the development and the occupation.

Concerns:

- Management was hesitant to answer some questions regarding TCC Concept RPT with EFC.

- The competitive intensity is increasing in this sector, which needs to be watched out.

| Subscribe To Our Free Newsletter |