As per managment, they can use practically capacity at level of 85% given the number of batches would reduce the operating time for change in new production order. Hence, at 75% they can increase sales by 10/75, i.e. 13% from the current capacity. However, there might be some new products as well which may need new machinery. Hence, in my view, new capacity expansion is much needed for the company for future growth. One shall not wait for 13% growth, which can happen in 3-6 months time and end up with siuation that there is demand but no capacity to fulfil that demand. While optimum utilisation and just in time improve productivity and margin, at time, particularly given the current geopolitical situation, some buffer for supply shocks are good in my opinion.

Secondly, on margin, your observation that margin at 10%, is not true business margin.

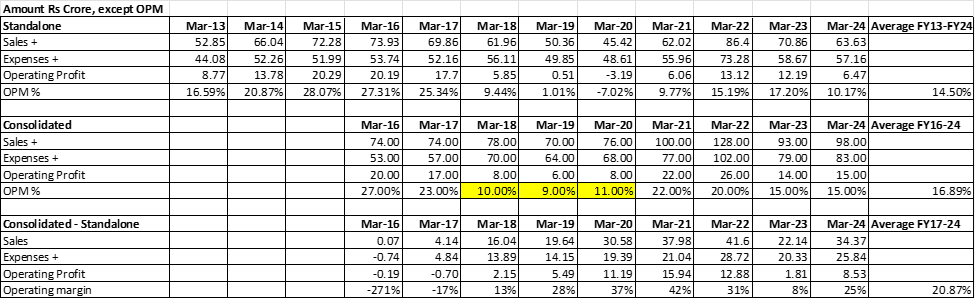

Find enclsoed sales, operating profit and operating margin of Premco Standalone and Consolidated financial over past 10 years sourced from screener.

Your obersvation is correct that during FY18-FY20 period, Consolidated operating margin was 9-11%. However, that was period when Vietnam operation was about to stabilise. If one look at FY26-FY24 period, than consolidated maring are around ~17% which is very good in my understanding.

Further, in my understanding, while the company has not grown signficantly during last few years, they have also not compromised on margin to enhance sales. I find that trait being long term value accretive. Again, this is my subjective evaluation which may biased and wrong.

Disclosure: Same as last post.

| Subscribe To Our Free Newsletter |