Putting down some of the things that I came across from management commentary and AR:

- In Q1FY25 concall, management claimed to have 300Cr of Cash on book, which seems questionable

Net Debt Q4FY24 = 1824 Cr

Net Debt Q1FY25 = 1862 Cr (increased by 38Cr)

Cash on books as on Q4FY24 = 262 Cr

Free Cash generated in Q1FY25 = 34 Cr (per concall)

Did company take additional debt of ~72-75Cr in Q1FY25 to achieve 300Cr cash with increased net debt of 1862Cr?

In reality, net-debt increased by 38Cr inspite of generating 34Cr cash. This means cash outflow of 62Cr (capex).

-

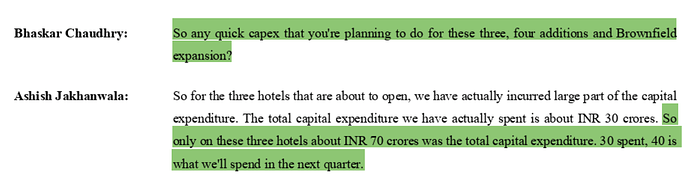

Inconsistent commentary on Capex numbers for planned renovation+new rooms+ACIC integration.

– In Q4FY24 concall, management claimed that company will spend 65Cr in FY25 for capex that includes all above activities

(1) 40Cr for renovation & new rooms

(2) 25Cr for ACIC integration

– In Q1FY25 concall, management claim to spend 138Cr for capex including same all above activities.

Mismatch (increase) of ~73Cr in near-term capex number commentary between Q4 and Q1. Though total 168Cr (138 + 30 incurred in FY24) capex seems reasonable(?) for: 111 rooms (Kolkata new hotel) + 137 rooms (rebranding Noida) + 54 rooms (new rooms Bangalore) + 22 rooms (new rooms Pune) + ACIC integration

-

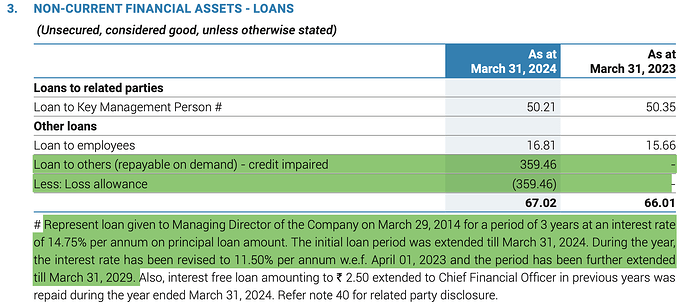

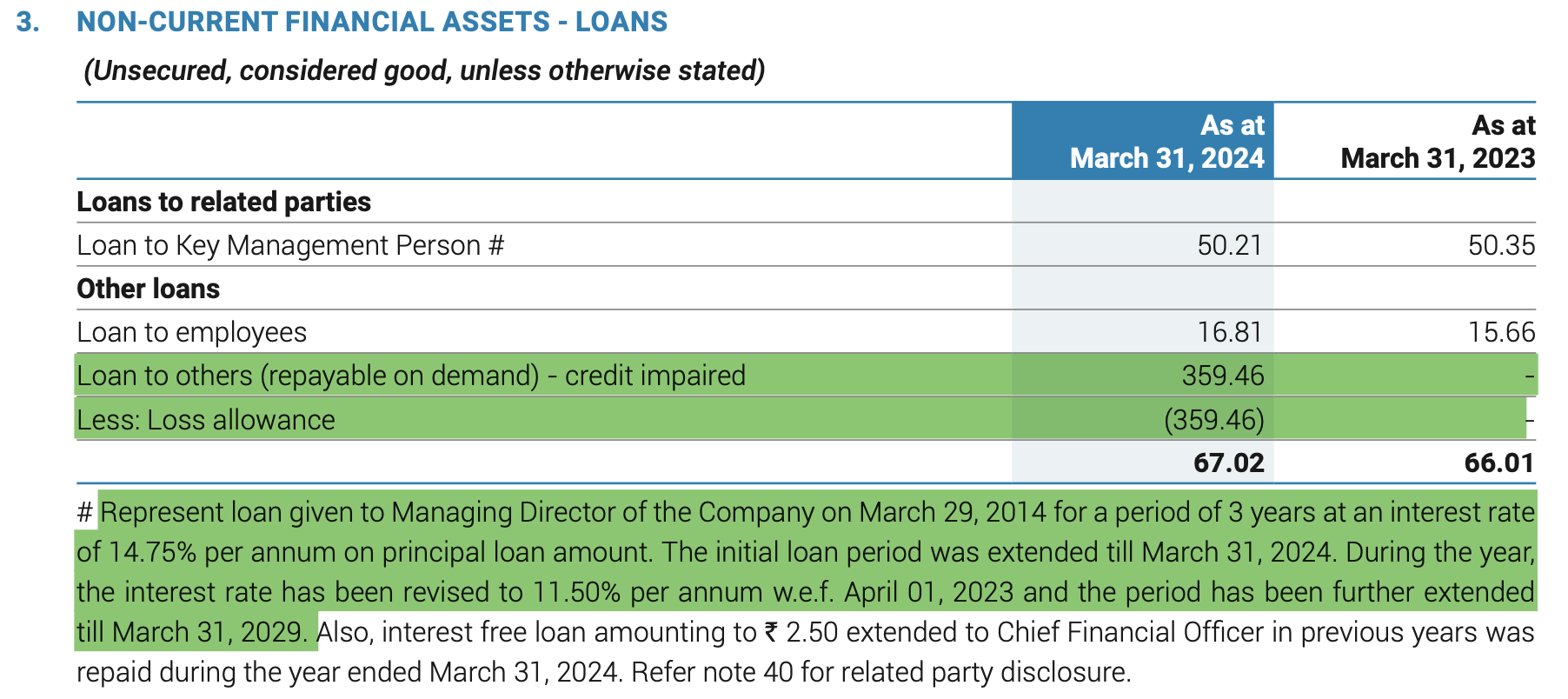

Some minor not-so-good things with loan given to others and MD.

Credit impairment of 35Cr for loans (to others) which was given in the same year.

Disc: Invested

| Subscribe To Our Free Newsletter |