Hello Community,

I’d like to share some quantitative insights from my analysis, which complement the qualitative highlights that @Chandragupta Sir has thoughtfully provided. His review gives a thorough understanding of the business, and now let’s dive into the numbers since listed:

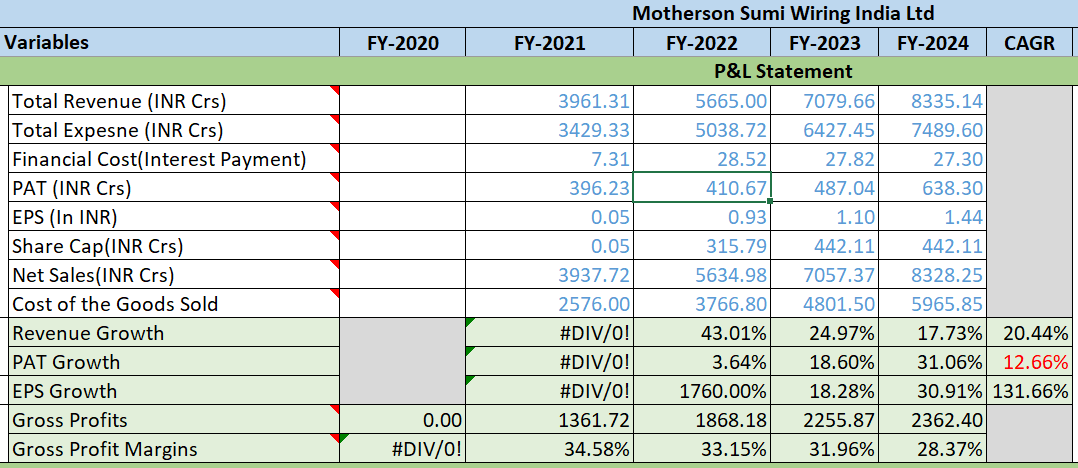

Profit & Loss Statement:

- Revenue CAGR: 20%

- PAT CAGR: 12%, with consistent year-over-year improvement

- EPS CAGR: 131%, also improving year over year

- Gross Profit Margins: Steadily hitting 30% YoY

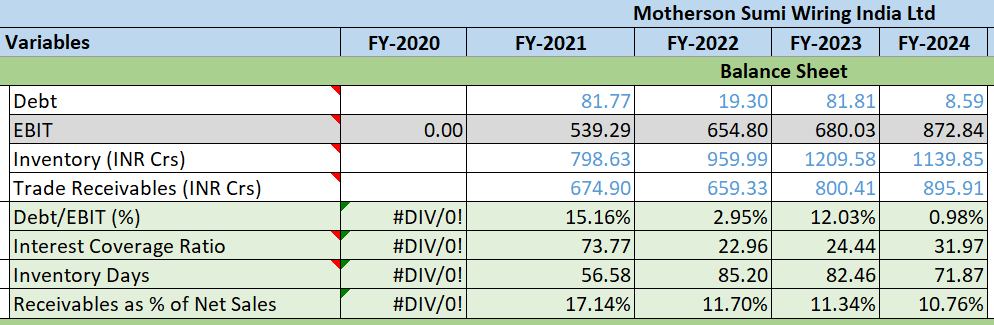

Balance Sheet:

- Debt to EBIT Ratio: Reduced over the past 5 years

- Interest Coverage Ratio: Consistently improved over the last 3 years, reflecting sound financial management

- Inventory Days: Declining, while PAT is increasing from last 3 years, signaling positive growth

- Receivables as % of Net Sales: Showing a downward trend, which is encouraging

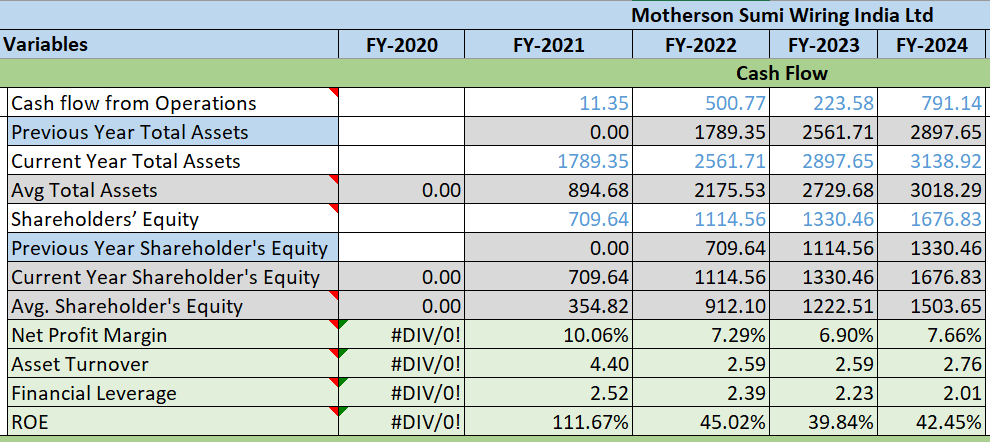

Cash Flow Statement:

- Net Profit Margin: Consistently around 7%; further improvement would be beneficial

- Asset Turnover Ratio: Stable at about 2.5x

- Financial Leverage: Decreasing

- ROE: Exceeding 40%, which is phenomenal

ROCE & Business Focus:

- The company’s ROCE is driven more by higher sales relative to capital employed rather than margin improvement, suggesting a supplier-side moat. This aligns with the management’s commentary, indicating a strategic focus on ROCE over margins. Maintaining and enhancing this supplier-side moat will be crucial for future performance.

Conclusion:

This is a simple business with a strong supplier-side moat, benefiting from positive industry tailwinds and robust parentage from SAMIL and Sumitomo Wiring Systems, Ltd. (SWS). If they expand their supply reach into other industries like healthcare, aerospace, and logistic solutions, etc., it could lead to margin expansion, improved ROCE, enhanced profitability, and ultimately, higher earnings.

Disclaimer: I am invested, so I may be biased.

| Subscribe To Our Free Newsletter |