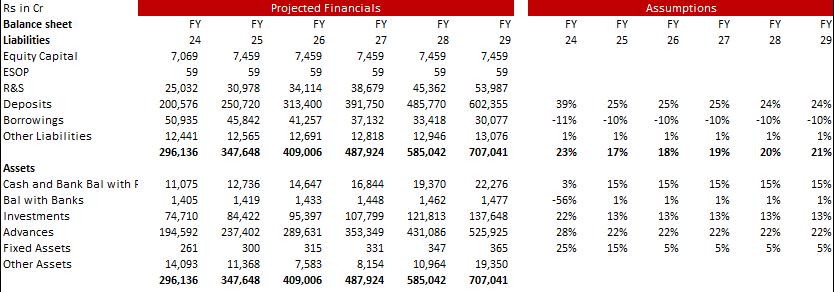

Here is my Projected Financials of IDFC First till FY 29 based on management guidance of few metrics in their Guidance 2.0 metrics and few of my own hypothesis

- Loans to grow annually at ~ 22% till FY 29

- Deposit to grow by 25% till FY 27 and 24% thereafter

- Borrowings to be keep reducing by 10% YOY

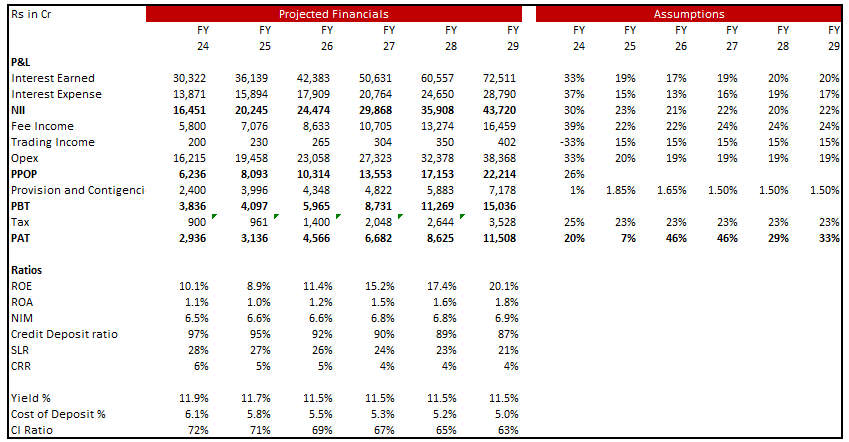

- NII to grow at CAGR of ~ 24% annually till FY 27 and then slow to ~ 20% ( have assumed drop in yield to be 40 bps in 5 years due to estimated repo rate drop ( almost 40% the book is not repo rate rate driven ) and assumed Cost of deposit to drop by almost 100 bps over next 5 years due to pay off of legacy bonds , reduction in repo rate )

- Fee Income to grow by 22-24% annually till FY 29 ( Assumed growth here to tapper from 35% -40% historically as many fees are waived off )

- Opex increase assumed to be 20% in FY 25 and 19% thereafter ; Cost to Income ratio to come down by 67% till FY 27 and 63% by FY 29

- Credit Cost to be 1.85% in FY 25 , 1.65% in FY 26 and 1.50% from FY 27 onwards

- ROA is coming to be 1.5% in FY 27 and 1.8% in FY 29

- PAT for FY 29 is coming at ~ 11500 Cr ;

- Have assumed no further equity dilution

Kindly critically examine these numbers and assumptions as to far these looks reasonable

Management has guided for 12-13k Cr of PAT in FY 29 with 1.8-2.0 ROA and 17-18% ROE and 7 lacs cr of Balance sheet size

Disc : Invested

| Subscribe To Our Free Newsletter |