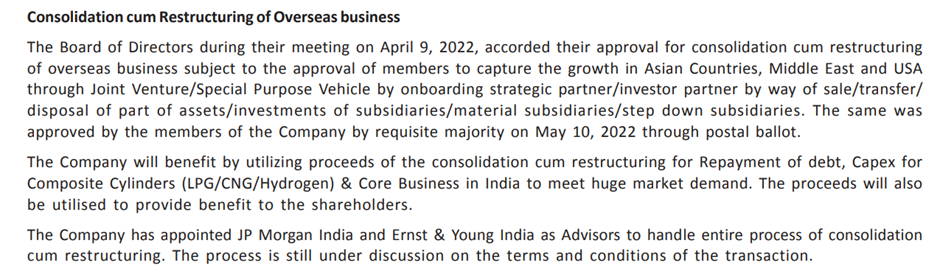

The Annual Report confirms what I suspected (see this) – no consolidation / restructuring of overseas businesses is going to happen. All such plans have been given a quiet burial. The Annual Reports of FY22 and FY23 had contained the following paragraphs:

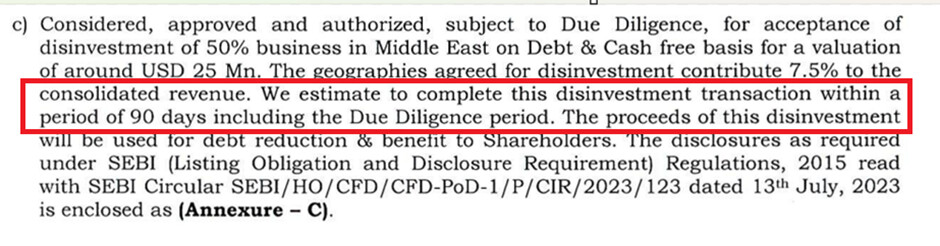

However, the latest Annual Report for FY24 only mentions 50 % divestment of the Middle East business announced earlier. Everything else has been removed:

This is a far cry from the understanding that was conveyed when the restructuring was first announced more than two years ago. The resolution to approve restructuring of the business was put to vote and passed in April / May 2022. At that time, the intent was to invite strategic partners / investors to participate in JV / SPVs while continuing to hold only minority stakes in foreign entities. This would release large resources which could be ploughed back into India, to repay debt, reward shareholders and invest in the domestic businesses. A step-down subsidiary called “Abhi Investment Holdings” was incorporated to hold TTL’s stake in these JVs / SPVs. Ernst & Young was appointed to advise and oversee the process and later, JP Morgan was added to the list. But the restructuring kept getting postponed from one quarter to the next, and then more.

Abhi has disappeared without a trace. It is not mentioned even in Form AOC-1 of Annual Reports for FY23 or FY24, so looks like it was never registered or has been liquidated. JP Morgan / E & Y have gone home, we don’t know what they advised. No JV / SPV has so far been formed, no strategic partner has joined hands with the company. Instead of holding minority stakes as promised, the company announced it is retaining 50 % in the Middle East business and has gone silent on the rest. Even the Middle East transaction, announced on 12th February 2024 is not yet closed. It was expected to be completed in 90 days, and we are in September already.

So even this deal should be considered closed only when they actually show the money.

Essentially, the whole restructuring story is coming to naught. Investors can only expect sale of Rs.100-odd crore worth of non-core assets I think, nothing more. Of course, operational improvements have happened over the last two years and will likely continue, but it is a far cry from what was implied two years ago.

May be the company has legitimate reasons for going back on the restructuring. May be the overseas businesses are doing well, and JPM / E&Y might have advised against selling. But whatever it is, it has not been communicated transparently, we have to read between the lines.

(Disc.: No positions)

| Subscribe To Our Free Newsletter |