122% return in 15 months – this eye-catching data is of Mankind Pharma’s IPO.

Source: New Listed IPOs at Ticker

- If you are exploring pharma stocks for your portfolio or

- you missed out on the Mankind Pharma IPO or

- you didn’t get an allotment

Mankind Pharma is worth having a close look at.

First-generation promoter Ramesh Juneja founded the company. Mankind’s journey from a family business to a healthcare giant is nothing short of inspiring.

After leaving a secure job at a leading pharmaceutical company, Juneja ventured out to address the overlooked medical needs of small towns and villages across India. This mission has remained at the core of the company’s strategy for the past three decades.

Below is Mankind’s FY23-24 revenue breakdown:

- 92% from the domestic sales

- with 47% of that coming from Tier II-IV cities and rural markets

This breakdown represents the company’s focus on affordability, extensive reach in underserved areas, and strong brand presence. All these, already highlighted in their key differentiators, set Mankind apart in the pharma industry.

First-generation promoters often excel at nurturing and expanding their family businesses.

- Companies like Bharti Airtel, Page Industries, and Infosys are some examples.

- Mankind Pharma follows this trend, blending a deep commitment to quality with aggressive growth strategies.

This combination makes it a compelling stock option for your investment portfolio.

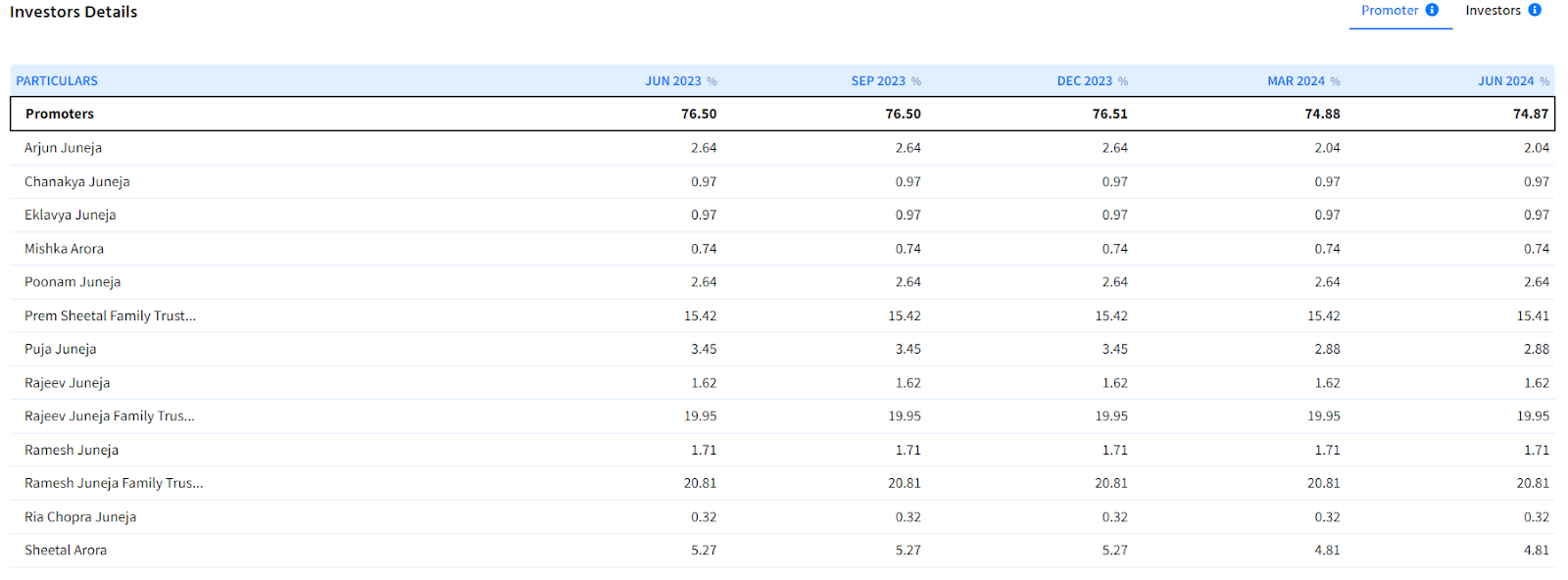

Junejas’ family holdings

(Source: Mankind Pharma Company Page in Ticker)

The influence of the Juneja family on Mankind Pharma’s growth is undeniable. Their strategic input has driven significant operational efficiency and market expansion.

Due to their keen focus on optimising operations:

- Net Operating Working Capital Days reduced from 45 days to 42 days in FY 2023-24

Despite industry headwinds, this achieved improvement reflects their commitment to operational excellence. The family’s leadership has also been pivotal in achieving strong domestic primary growth of 13% in FY 2023-24.

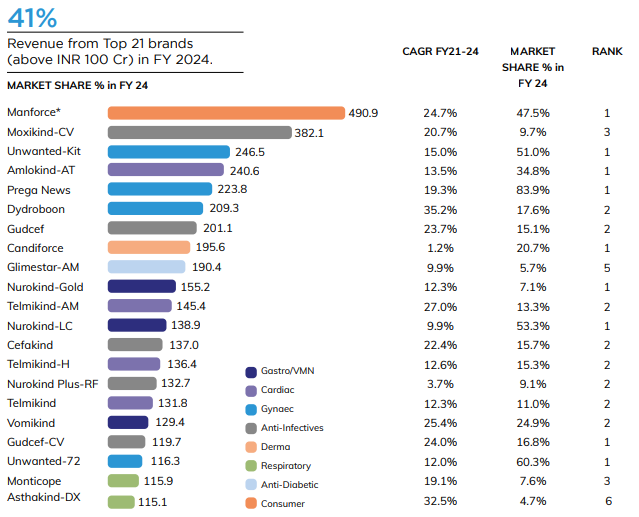

Growth has been particularly strong in the chronic, anti-infective, and gastro segments, fueled by gains in modern trade and hospital sales. Junejas’ investment in manufacturing capabilities further demonstrates their strategic foresight.

Mankind Pharma is well-positioned to dominate the market with:

- 30 facilities across India and

- a total installed capacity of 43.5 billion units per annum

The commissioning of India’s first fully integrated manufacturing facility for Dydrogesterone and hormone-related products in Udaipur, Rajasthan, is a testament to their innovative approach. Additionally, they started moving towards backward integration. Manufacturing APIs and key starting materials for flagship brands like Telmikind and Dydroboon have slashed operating costs and boosted product quality.

These strategic moves showcase the Juneja family’s ability to steer Mankind Pharma towards sustained growth and a competitive edge in the market.

Acquisition Insights: Bharat Serums And Vaccines Limited (BSV)

-

BSV Acquisition: Expected to significantly enhance Mankind’s gynaecology portfolio and contribute to becoming the leader in the segment

-

Fertility Portfolio: Positioned for growth, with potential for better revenues through cross-selling in fertility clinics and institutions

-

In-House Manufacturing: Potential to manufacture BSV’s prescription portfolio in-house, reducing costs and improving profit margins

-

R&D Capabilities: Leverages BSV’s strong R&D platform in recombinant technology, niche biologics, novel delivery systems, and immunoglobulins.

-

-

Synergies: Expected synergy benefits ranging from ₹50 to ₹100 crores over 12 to 24 months

Future Guidance

-

EBITDA Margin: Retaining 25% to 26% guidance for FY25

-

Growth Focus: Aiming for sustained growth in domestic and international markets, focusing on high-margin chronic therapies

| Subscribe To Our Free Newsletter |