-

Net addition of stores peaked out in Q2FY23 when 348 stores were added during a quarter. Average store openings over the last three quarters have been below 150. Q1FY25 was an aberration because of general elections. The management continues to guide for 600 store openings on an annual basis

-

Consequently stores open for 2 plus years have seen a bump up which has improved the margins as well. Management maintains stores open for 24 months plus contributes higher to EBITDA

-

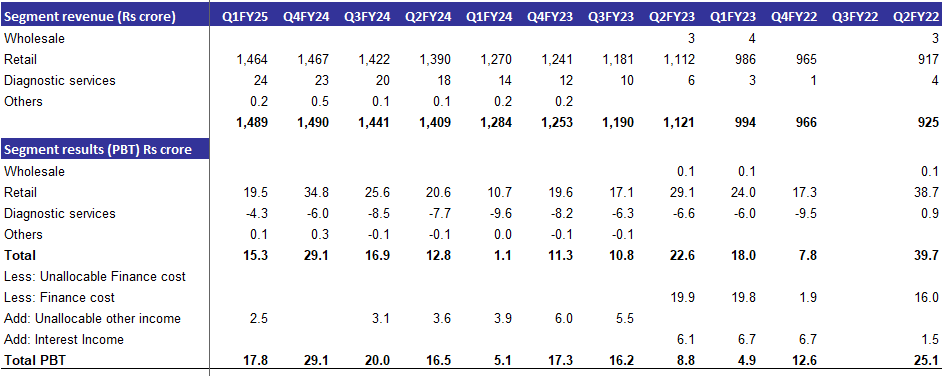

The diagnostics business has seen its annual run rate increase every year since its opening going up from Rs 30 crore annualised to Rs 100 crore annualised in FY25. Consequently PBT losses in this business in Q1FY25 were at their lowest. Hopefully this business too starts contributing to the bottomline by FY26. The margins in diagnostic business are much better than traditional pharmacy retail. This for now remains a one city operation confined to Hyderabad only

-

Private label contribution at 15.8% of overall revenues in Q1FY25 is highest for the last few years. As per management guidance this will improve overall margins for the business

Disclosure: I own shares in the company

| Subscribe To Our Free Newsletter |