It is definitely the reason for low and slow deposit growth.

There’s plenty of money in the system but deposit is not attractive compared to stock market.

“₹12-crore IPO of Resourceful Automobile, an SME company, which attracted bids worth ₹4,800 crore.

The ₹6,560-crore IPO of Bajaj Housing Finance set a new record, with subscriptions exceeding ₹3 lakh crore. The IPO was oversubscribed 63.61 times.”

Post from another thread:

3.2 Lkh crore blocked in bank accounts towards Bajaj finance IPO size of 6600 crore- looks scary !

Source:

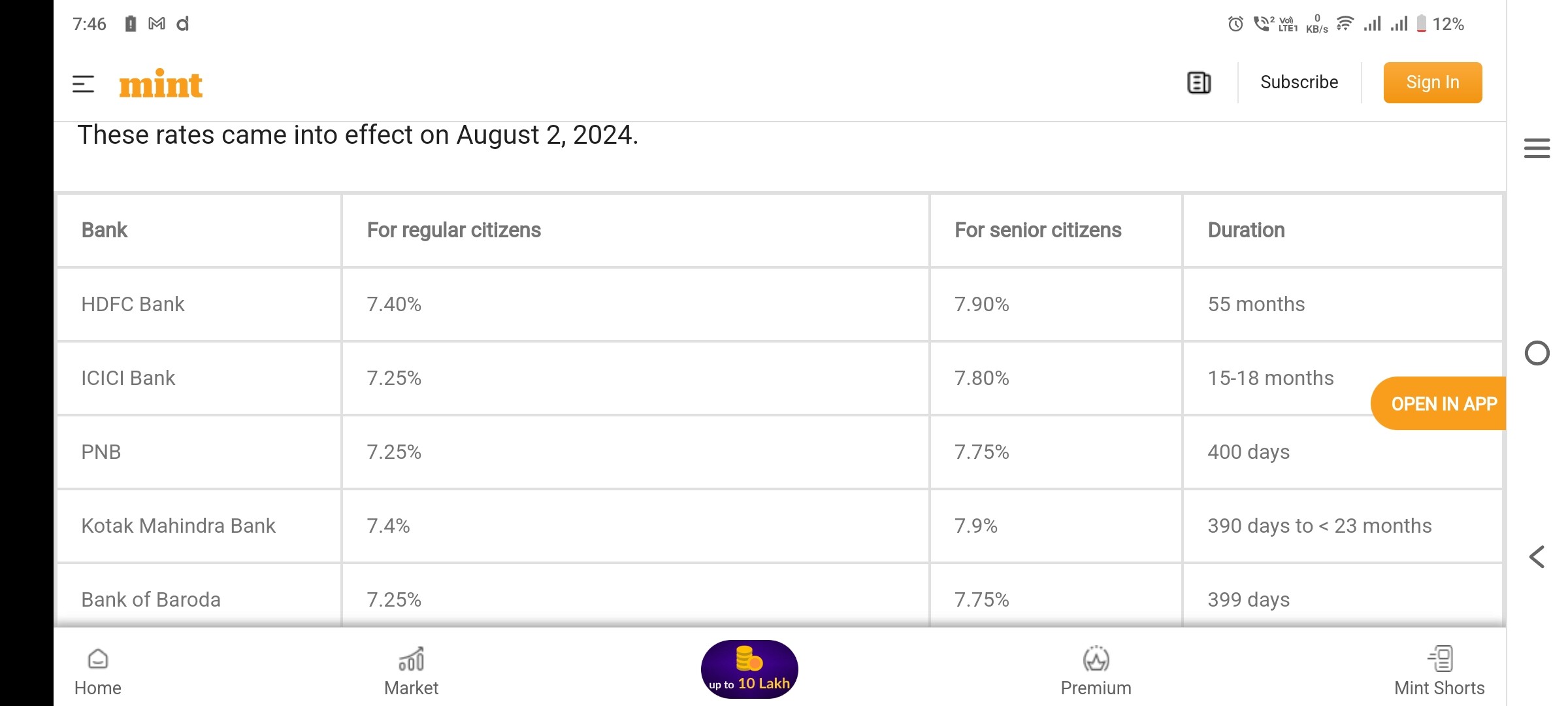

The bank FDs are not even yielding 8% pa interest. Over that, the interest is taxed at peak slab rate. For me it is 35%. So post tax, returns is 5.2% while the real inflation will be North of 7%. And there’s no deposit protection beyond 5 lakhs.

I don’t see any incentive in Bank FDs. Money will be better placed in nifty index fund which will give 12% cagr over long-term.

A patient investor in HDFC Bank and Kotak Mahindra Bank will be better rewarded than an FD holder in those banks. Also, we are at the peak of interest cycle and interest is bound to go down from here which will bring down the FD rates even further.

| Subscribe To Our Free Newsletter |