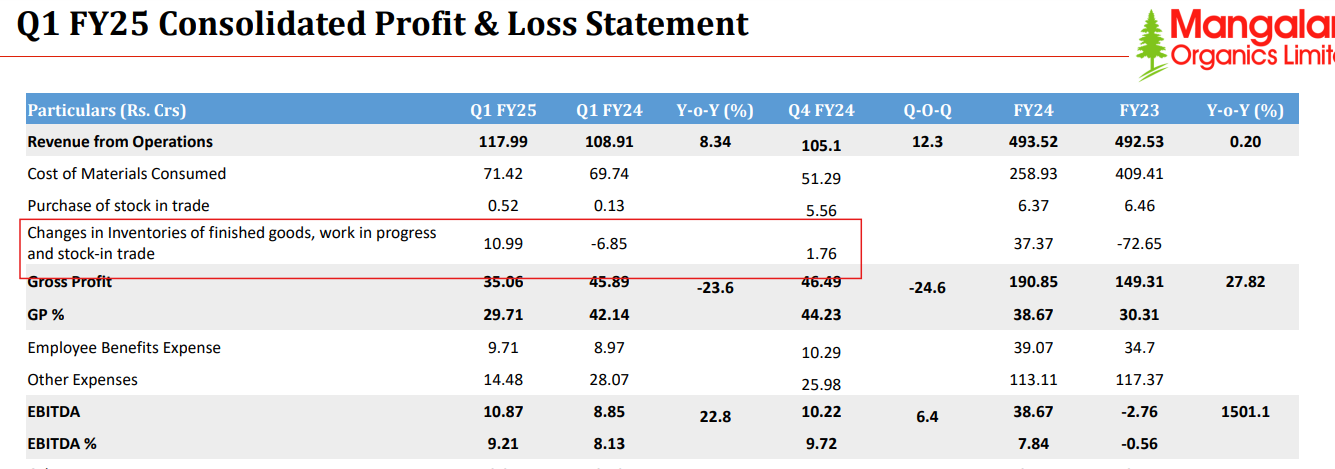

Mangalam Organics has become increasingly difficult to track as it doesn’t do con-call and is highly illiquid (made worse by SEBI ASM frameworks) as well. If i recall, it had done large capex few quarters ago. There may be lag between commodity price increase and company earning due to multiple factors e.g. low priced finished goods inventory still in the channel esp. for B2C players, existing price contracts for B2B sales wherein price hike may take few qtrs to come into effect, presence of high cost RM inventory hence subdued margins, loss of market share etc. Most of these reasons may be theoretical as lack of con-calls means these would be our best guesses. Some buying by promoters and impact of capex done in 2022, may indicate positive outlook for the company esp. if camphor prices remain firm. Q1FY25 results too indicate some increase in inventory so their liquidation at increased prices too can give EPS a leg up.

| Subscribe To Our Free Newsletter |