Apeejay Surrendra Park Hotels Limited (ASPHL)

Apeejay Surrendra Park Hotels Limited (ASPHL) is a prominent player in India’s hospitality sector, with over five decades of experience in luxury boutique and midscale hotels. Known for its flagship brand, The Park Hotels, ASPHL has established itself as a leader in creating unique, design-driven properties in key urban locations across the country. The company’s portfolio includes 33 operational hotels, spanning luxury, upper midscale, and economy segments. Additionally, ASPHL’s iconic F&B brand, Flurys, contributes significantly to its diverse business model. The company’s commitment to innovation and service excellence ensures its strong position in India’s growing hospitality market.

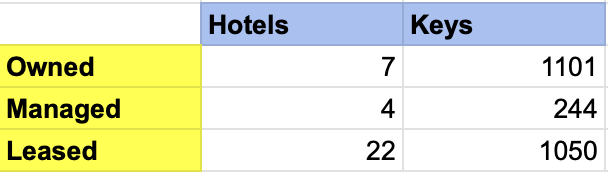

Hotels Bifurcation-

Operates 4 segments of Hotels-

- The Park Hotel– Luxury Hotels in metros

- The Park Collection– Luxury Resorts/Hotels in select tourist destinations (have less rooms)

- Zone & Zone Connect- Upper Midscale segment

- Stop by Zone– Motels (economy)

Hotels in place-

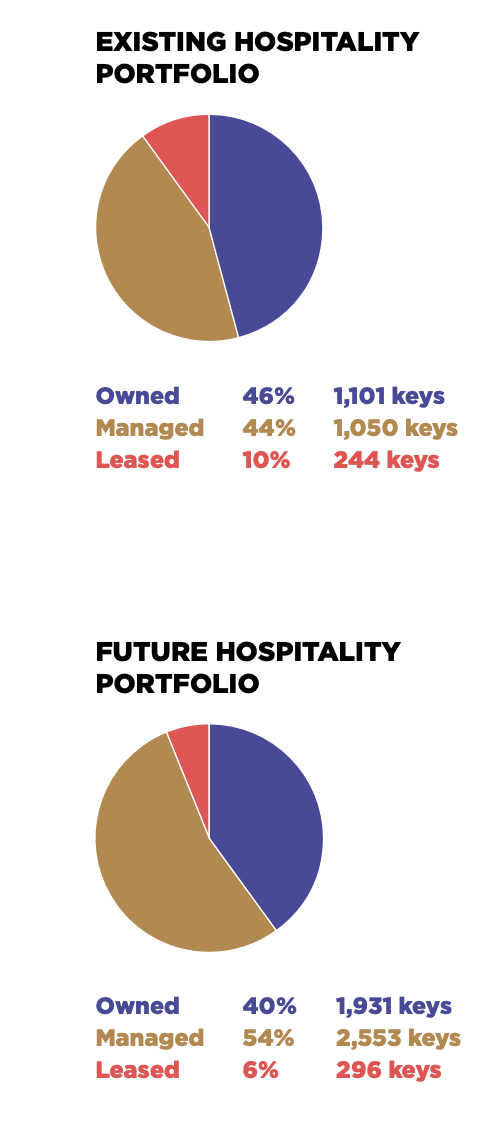

Total Keys- 2395 over 33 Hotels

Key Differentiation-

Operating at- 92% occupancy (100% in kolkata hotel, 93% in Mumbai and Chennai Hotel)

ARR- 6699

RevPAR- 6170

*They have the highest occupancy rates in the industry. Even during the covid maintained 62% occupancy rates.

Guidance-

Occupancy will be maintained at 92%, moreover can increase it to 93-94%.

Revenue Bifurcation-

Room rent- 58%

F&B- 32%

Flurys Coffee Shop- 10%

(ASPHL) boasts a vibrant portfolio of 88 restaurants, nightclubs, and bars, renowned for their exceptional ambiance and energetic nightlife. The nightlife at The Park Hotels has earned a stellar reputation, with its bars and nightclubs being popular destinations among patrons for offering dynamic, immersive environments. Additionally, strong presence in nightclubs and bars compensates for the downturn if ever happens in the industry,

FLURYS- The Coffee Shop / Tea Room

The bakery is quite famous and well known and is one of the most iconic confectionary brand in the country.

It currently operates 82 Flurys bakeries, with plans to expand aggressively by adding 30-40 new outlets annually. The brand has received a strong response from customers, particularly in Mumbai, where its recent introduction has been met with overwhelming success. The outlet near the Gateway of India has consistently exceeded expectations, and a new location in Colaba is set to open soon. Additionally, two kiosks have been launched at Mumbai Airport. Management remains highly confident in Flurys’ growth potential and believes it will continue to surpass expectations.

The bakery is on 3 formats-

- Kiosk- 150 sq ft (capex- 20 Lakh)

- Cafe- 400-600 sq ft (capex- 40-60 Lakh)

- Restaurant- 1000 sq ft (capex- 1cr)

Also, Cafe business is little seasonal-

H1- 40% sales

H2- 60% sales

Flury is earning 13% EBITDA margin. Will increase to the north of 20% in coming quarters and will be maintained there.

Hotel biz EBITDA margin- 36%

Won’t Flurys be a drag on consolidated EBITDA margins?

No, opening of luxury property- The palace hotels will earn significantly higher EBITDA margins and will compensate for the same.

35% EBITDA margin is stable on a consolidated basis. Has 2-3% headroom to grow if operating leverage kicks further.

Future Plans-

Many projects are under development for future expansion-

23 Hotels & 2385 keys- planning to be opened. This is almost a 100% increase from the present keys in place.

Q2 FY25-

Opening of 2 flagship Palace Hotels-

- The Chettinad Palace (15 rooms)

- The Ran Baas Palace, Patiala (37 rooms)

ARR for these 2 properties will be 13000. Occupancy will increase substantially. Getting a good response for these 2 hotels. Room bookings are already taking place.

Future Openings-

- FY27: 200 rooms in Pune- at capital outlay of 200 crs

- FY28: 100 rooms in Vizag- at capital outlay of 100 crs

- Fy 29- 200 rooms in EM Bypass + 100 apartments (JV with Ambuja Nautica)

At a capital outlay of 900 crs. The proceeds from the sale of apartments will be used for the construction of the hotels.

- FY 29- 80 rooms in Navi Mumbai

Plus the opening of 30-40 outlets of Flurys coffee house every year.

Total Capital Outlay will be around 1000 crores by FY29, fully funded by internal accruals. Can take a little debt to speed up the construction process. 1000 crores is net after accounting for the sale of apartments,

Future expansions are being driven by an asset-light model. The company’s owned hotels are situated on proprietary land banks, and further owned hotel developments will be constructed on these owned land assets.

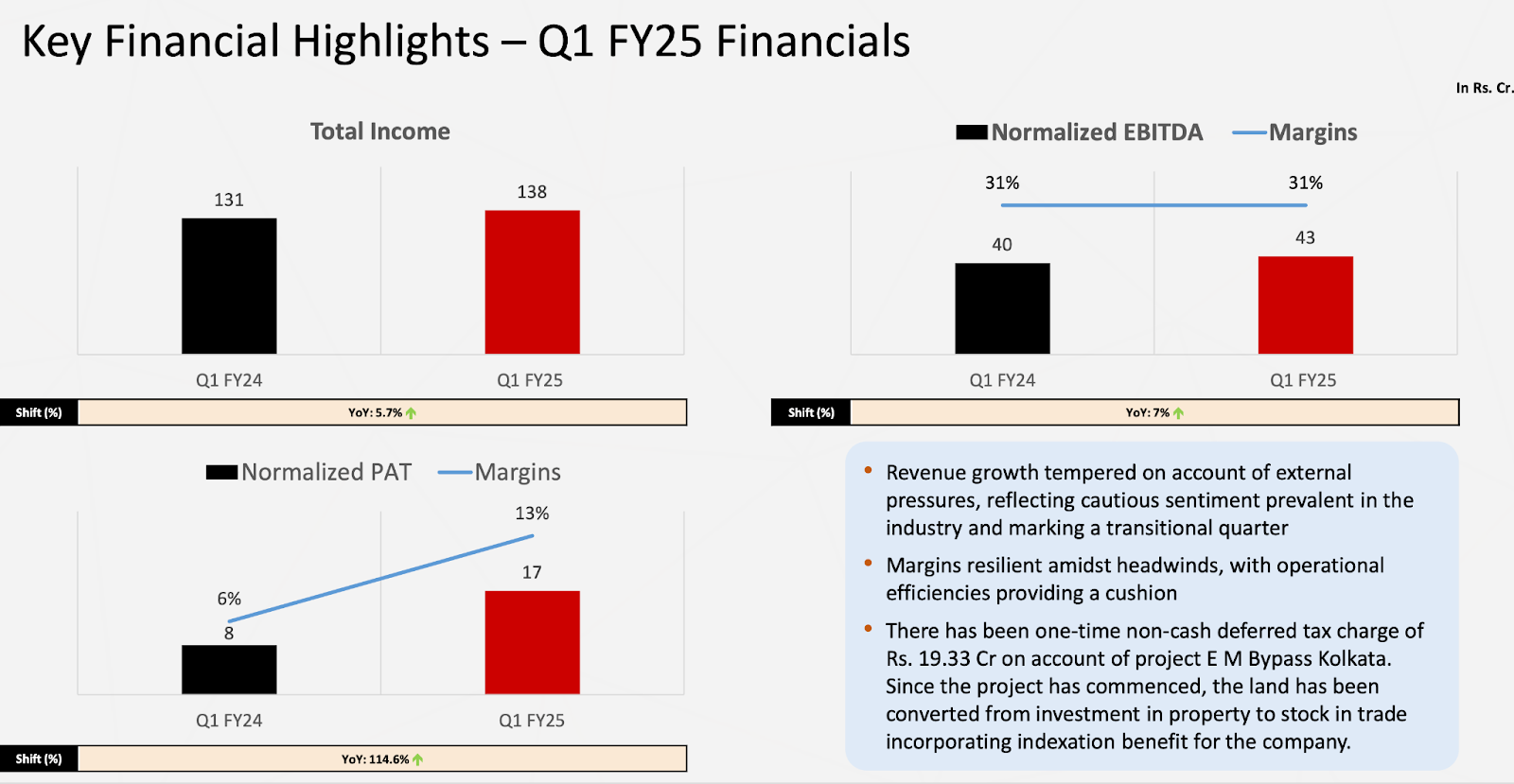

Q1 FY25

Why did PAT increase significantly?

Because from the IPO proceeds, the Company paid off the debt of 550 crores, Huge savings on interest cost happening.

Only 100 crores of debt remains in the balance sheet as of now.

12 Crores of interest payment will be happening p.a. reducing from 66 crores p.a.

Additionally, in this quarter they took 19 crores one off hit. (details mentioned in the slide)

Also, management mentioned Q1 was soft due to elections and heat waves.

And seasonality is there in business: Q4>Q3>Q2>Q1.

The company consistently undertakes renovations to enhance customer experiences, with 10% of its inventory typically under renovation at any given time. Currently, upgrades are underway for several hotel rooms and nightclubs. These ongoing renovations allow the company to maintain and elevate the immersive experience it is known for.

Park Hotels enjoys a high percentage of repeat customers, thanks to the company’s effective use of AI and ML to track user data and maintain ongoing engagement with guests. Additionally, the well-structured loyalty program ensures a strong, loyal customer base, further enhancing customer retention.

The markets they are operating in has seen a robust demand growth of 9.3% outpacing the supply growth of 5%. And this phenomenon will continue further leading to double digit ARR growth.

Flurys saw 17% YoY growth and will continue to surprise further.

Only 100 crores of debt remains in the balance sheet as of now.

12 Crores of interest payment will be happening p.a. reducing from 66 crores p.a.

Management expects 10-15% revenue growth YoY.

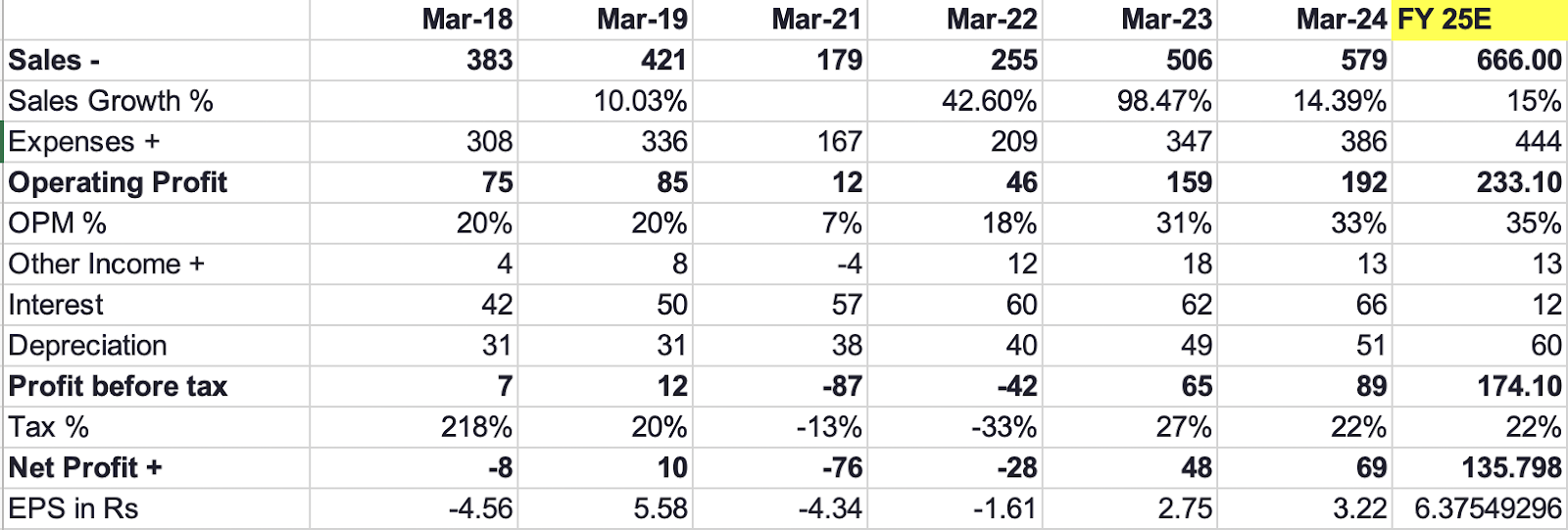

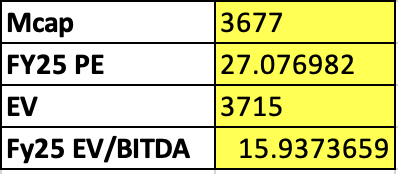

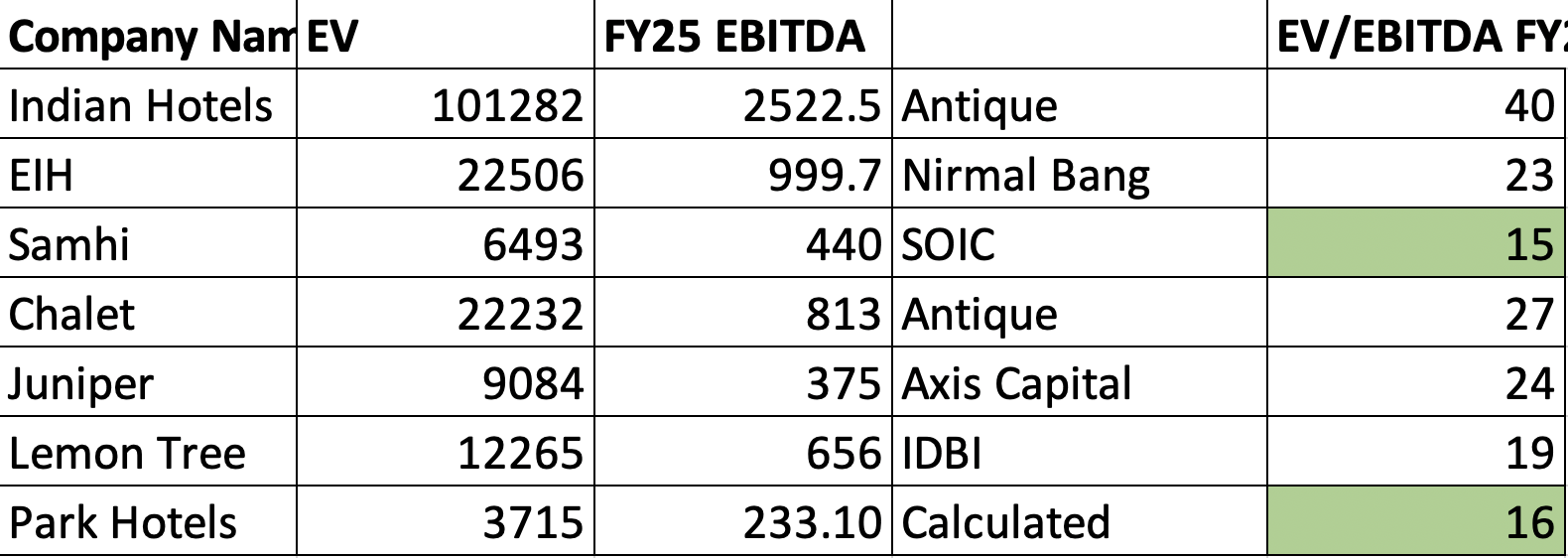

FY25 estimates:

P2P comparison:

Technically in a downtrend.

| Subscribe To Our Free Newsletter |