I’m bullish on waaree energies

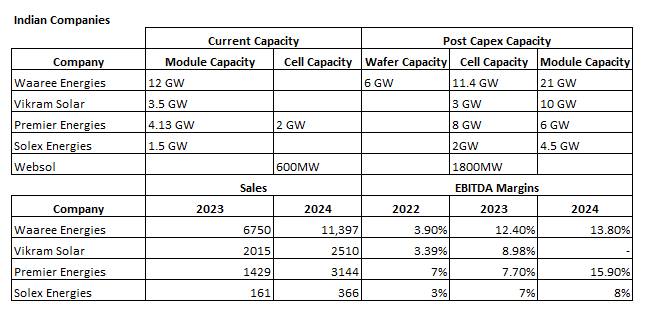

- Waaree Energies is one of the leading players in India’s solar energy industry. They are currently one of India’s largest solar module players with 21 GW capacity and 11.4 GW cell capacity. Its EBITDA margin has also improved

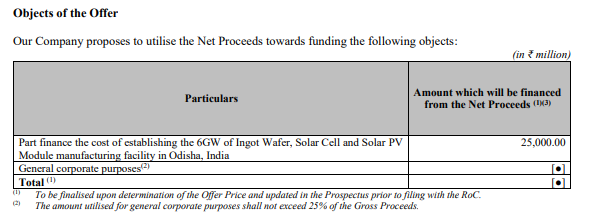

- Waaree Energies is setting up a 6 GW integrated facility for ingot wafers, solar cells, and modules in Odisha. The company is benefiting from Industrial Policy Resolution 2022 in Odisha, which includes capital subsidies, power tariff reimbursements, and tax exemptions

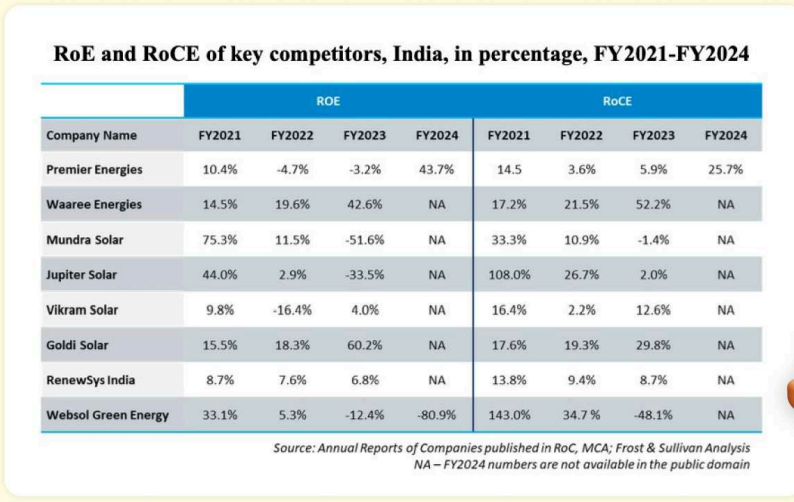

- High ROCE compared to other players

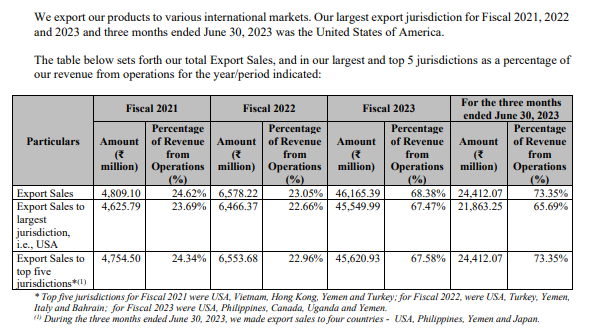

- Waaree may benefit from global shifts in solar module supply chains, particularly due to trade tensions between China and major markets like the US and EU. The demand for Indian solar modules is increasing, especially in the US and Europe. As of 2023, exports accounted for 70% of revenues

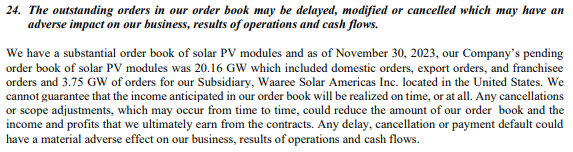

- Huge Order Book

Their order book as of November 30, 2023, was 20.16 GW for Solar PV modules

- The company also plans to venture into the green hydrogen market by setting up a gigawatt-scale electrolyser manufacturing facility, targeting sectors such as refineries, fertilizers, and chemicals

- Waaree has been awarded ₹19,232.40 million under PLI for its 6 GW integrated facility. The Indian government has set a target of achieving 280 GW of solar power by 2030. Waaree Energies can capitalize on the growing domestic demand

Disclosure: Invested. The above information is for educational purposes and should not be considered as a recommendation. Please conduct your own due diligence before making any decisions

| Subscribe To Our Free Newsletter |