Few thoughts about financial reporting and possibilities of ML models:

- Research has shown that companies that introduce a lot of changes to their reports between quarters are more likely to have negative stock price performance during the following period, see Cohen, 2020 and Adosoglou, 2021

- The downward price effect is usually not happening right at disclosure time, rather some time after it, when other news emerge, such as publishing of negative outlook etc.

- In other words, the information about risks etc. might have been provided in quarterly reporting, but in a more subtle way than a straight headline, for example. Therefore, it might have not been registered by investors, and is ignored in their decision making i.e. the stock price

- Implication from this is that an investor should be aware of sudden changes in the content of a company’s reporting, if the stock is intended for a long holding period. It is especially the case when a change has happened, but it hasn’t affected the pricing immediately.

- ML models can be used to quickly determine if semantically meaningful content change has happened.

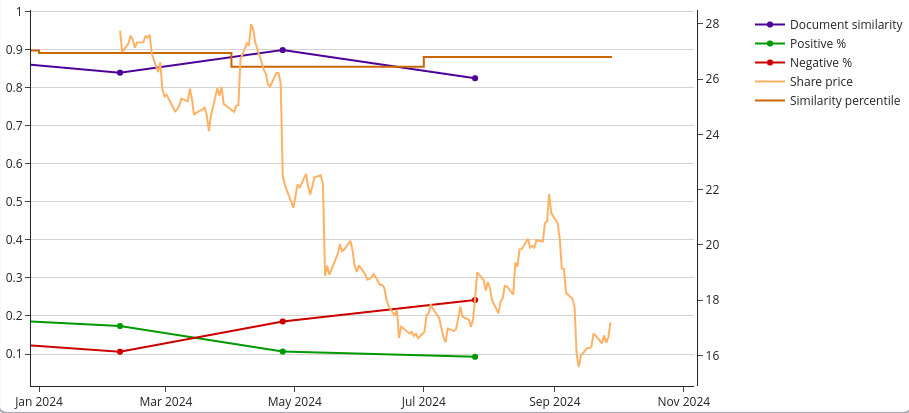

Here is one case example, from a Finnish large cap Neste, using the tool at finsim:

In the graph there are some developments of Neste’s year 2024.

- Dots represent quarterly reports, from Q4/23 to Q2/24. The brown reference line shows a similarity-score that 50% of companies don’t surpass during the quarter.

- It can be seen, that in Q1 the share price has plummeted after the release, most likely due to subpar numbers. Note also the rise of negative tone.

- However, a bigger slide in price happened some time after the release, when a lowering of outlook for the year was released. This could have been conveyed in Q4/23 report, which had little bit lower similarity-score than usual (84% similarity compared to Q3/23)

- In Q2, a more prominent effect was seen. At first, the markets responded with optimism, and the share price had an upward trend after the first days. Then, about month later another lowering of guidance happened.

- Here the similarity-score is around 82%, lower than usual, along with growing proportion of negative tone. Again, the Q2-report might have had some different wordings about risks etc, which were realized later during Q3.

At least in hindsight, the possibility of additional risks related to the company could have been picked out by using the similarity metric, and then delving into the details of the disclosure. In the Cohen study there is a similar type of example, they highlight the changes line by line, and show another turn of events. Here is also an interview, in which the study is discussed in more detail:

Lazy Prices with Dr. Lauren Cohen, professor at HBS

| Subscribe To Our Free Newsletter |