Mgmt. keeps saying that they are into 3 diff. lines of business. Yet most discussions keep gravitating towards the segment (metal trading) which they claim will only give them 1/3rd of their goals.

Even in metal trading, is the infra.market , for instance, really a competitor ?

Infra.market claims to be a house of brand. But it has (taken from it’s corporate video on it’s site)

- 10 Milion cubic meters of RMC mfg. capacity – worth 4k-6k cr.

- 2.5 Million AAC Block capacity – Again 1k cr. worth of

- MDF and laminate plants.

- Has it’s own brand of plastic pipes and fittings.

- Operates the shalimar paints brand and owns 24% of it.

- has a electrical and appliance vertical and manufactures them.

- Tiles Mfg… unit

- Modular kitchen mfg. unit etc etc…

Even with all this, it had a ~12k cr. topline and ~150 cr. PAT in FY23. Take a look at their corporate video. Do you still feel SGMart is competing with them ?

Should we compare this with SGMart just because there is online connection ?

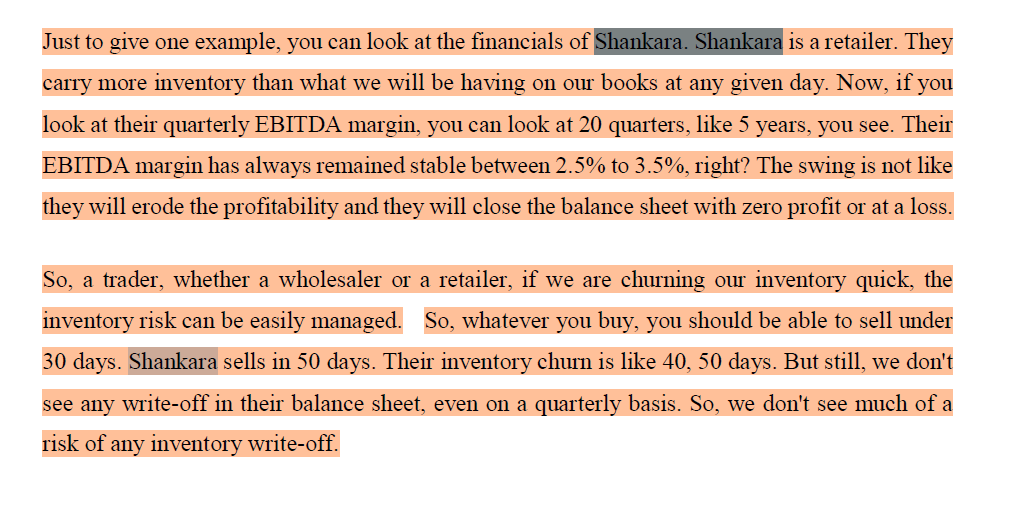

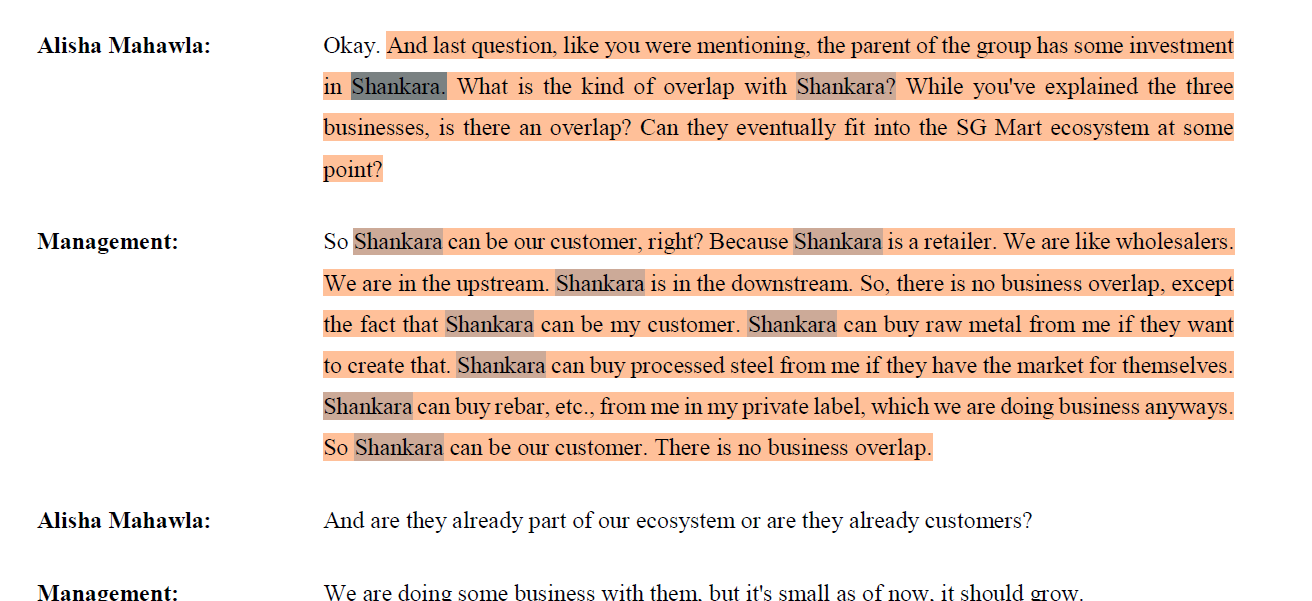

Comparison with Shankara is already addressed by Mgmt. in the call

mgmt. has given their logic of how they are playing to their strength by entering the specified segments.

OfBusiness operates in a market which offers 7.5% EBITDA margins. I doubt steel trading can give this kind of margins.

Also can we try and find some competitor in the rest 66% segment which SG is targeting ?

Can you help to give more clarity on this point. Do the Japanese trading company(like Marubeni) operate in India ? In the sense that they buy from Indian manufacturers and sell them to Indian distributors, like what SG is aiming to do ? If not then how is relevant to SGM ? They are not competing with Marubeni’s of the world in the world market, right ?

| Subscribe To Our Free Newsletter |