Key points from the Q1 FY25 earnings call:

Key Financial Performance

- Record Quarterly Sales: V2 Retail achieved its highest-ever quarterly sales in Q1 FY25, with revenue from operations reaching INR 415 crores, up 57% year-on-year.

- Profitability: Gross margin stood at 29%, and EBITDA grew by 56% to INR 55.5 crores. The net profit (PAT) increased by 162% to INR 16.3 crores.

- Same-Store Sales Growth (SSG): The company reported robust SSG of 37% and volume growth of 55%, driven by a high proportion of full-price sales (93%).

Operational Highlights

- Store Expansion: V2 Retail added 10 new stores in Q1, bringing its total count to 127 stores. The company plans to add 40-50 new stores this year, primarily in Tier I and II cities, and underserved markets.

- Private Label Growth: The contribution from private labels rose to 80%, with a target to reach 100% in the next 1-2 years. This strategy is expected to enhance brand identity and customer loyalty.

- Inventory Management: Inventory aging improved, with the share of stock over a year old dropping to 7% from 23% two years ago. The goal is to reduce aging inventory further.

Strategic Focus

- EBITDA and Margin Goals: Targeting a pre-IndAS EBITDA margin of 8-9% and a PAT margin of 4.5-5.5% for FY25.

- Expansion Strategy: Planning to invest INR 110 crores in store expansion, inventory, and working capital, funded through internal accruals.

- Targeted ROE: The company aims to achieve an ROE of 20-22% through increased sales and improved operational efficiency.

Competitive Landscape

- Positioning Against Competitors: V2 Retail faces competition from brands like Zudio, Reliance’s Youthstar, and others. However, it differentiates itself with lower average selling prices and a focus on family shopping, especially in kids’ wear.

- Pricing and Margin Strategy: Emphasis on cost-effectiveness allows V2 Retail to pass savings to customers without reducing gross margins.

Key Challenges

- Store Profitability: The company has worked to ensure each store contributes positively to EBITDA, with no EBITDA-negative stores this year.

- Cost Management: Rising employee costs due to new store openings impacted margins, but the company aims to maintain cost efficiency through better technology and supply chain improvements.

Future Outlook

- Growth Projections: The company expects revenue and EBITDA to grow by 30-40% annually, supported by continuous demand and a favorable market.

- E-commerce Entry: V2 Retail is evaluating an omnichannel approach, using store inventories to fulfill online orders within city limits, potentially reducing logistics costs.

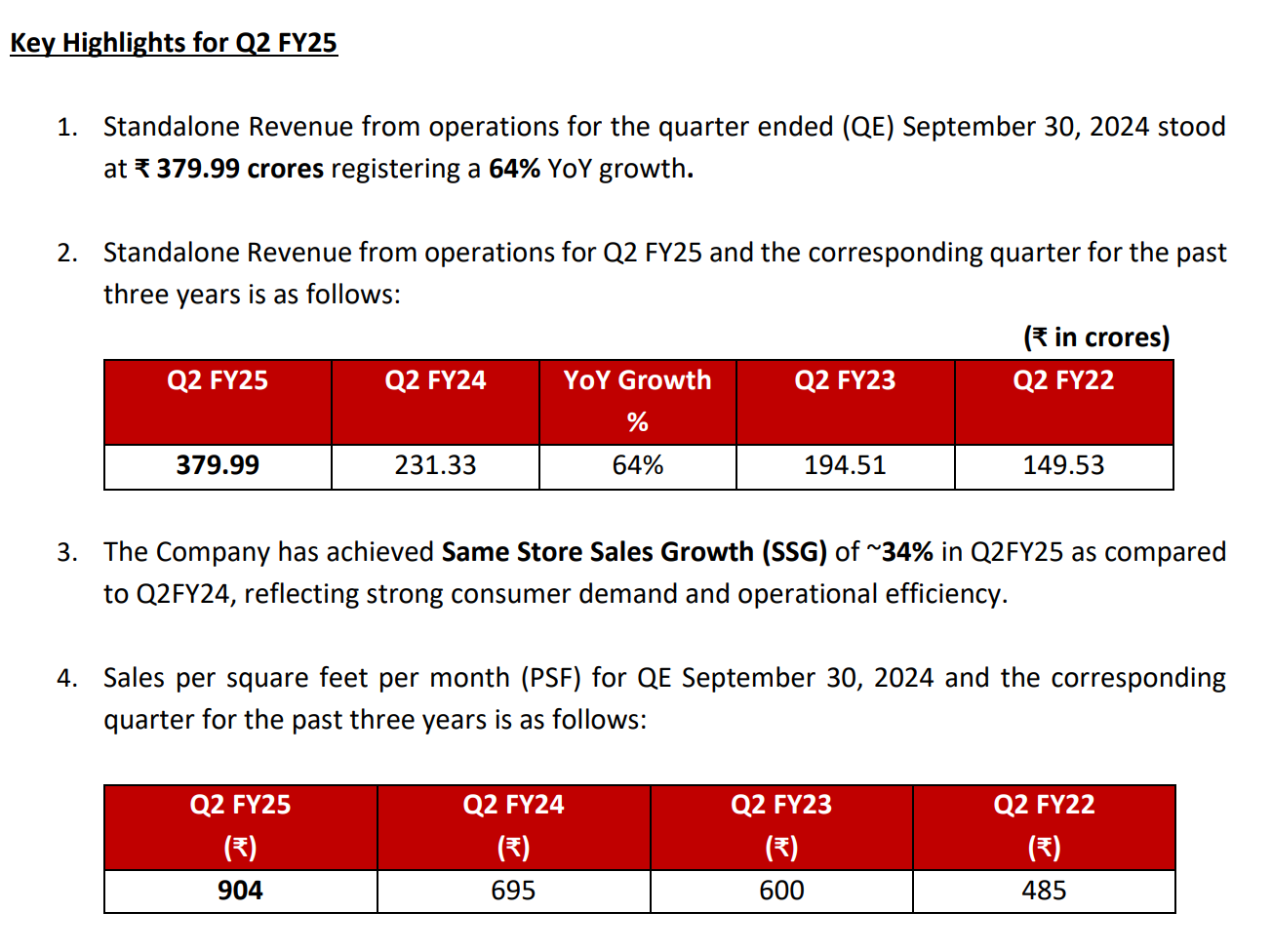

Latest Q2FY25 Update –

Disclosure – Invested

| Subscribe To Our Free Newsletter |