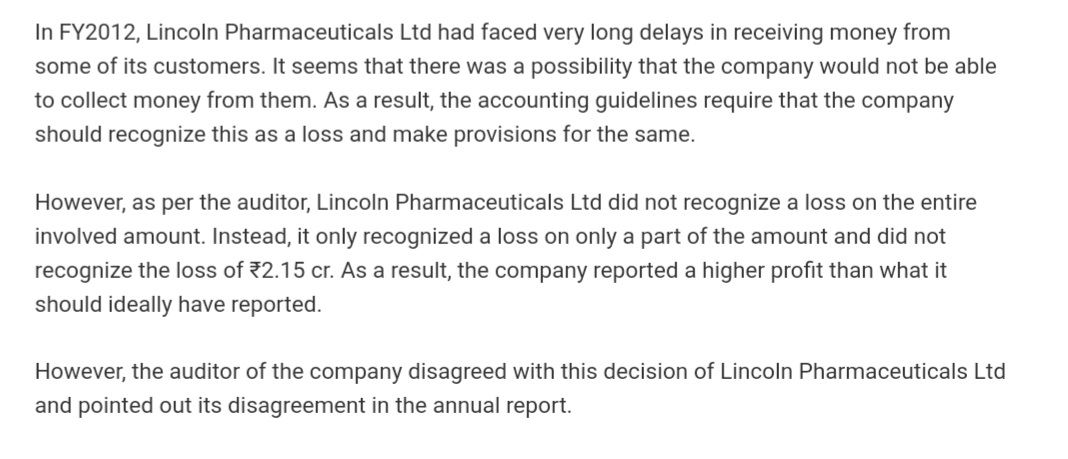

Lincoln Pharma has a history of inflating its profits, In FY 2012, the company reported a lower provision for bad debt, categorizing it under trade receivables.

With other income sources including 22 crores from share valuations related to investments or trading.

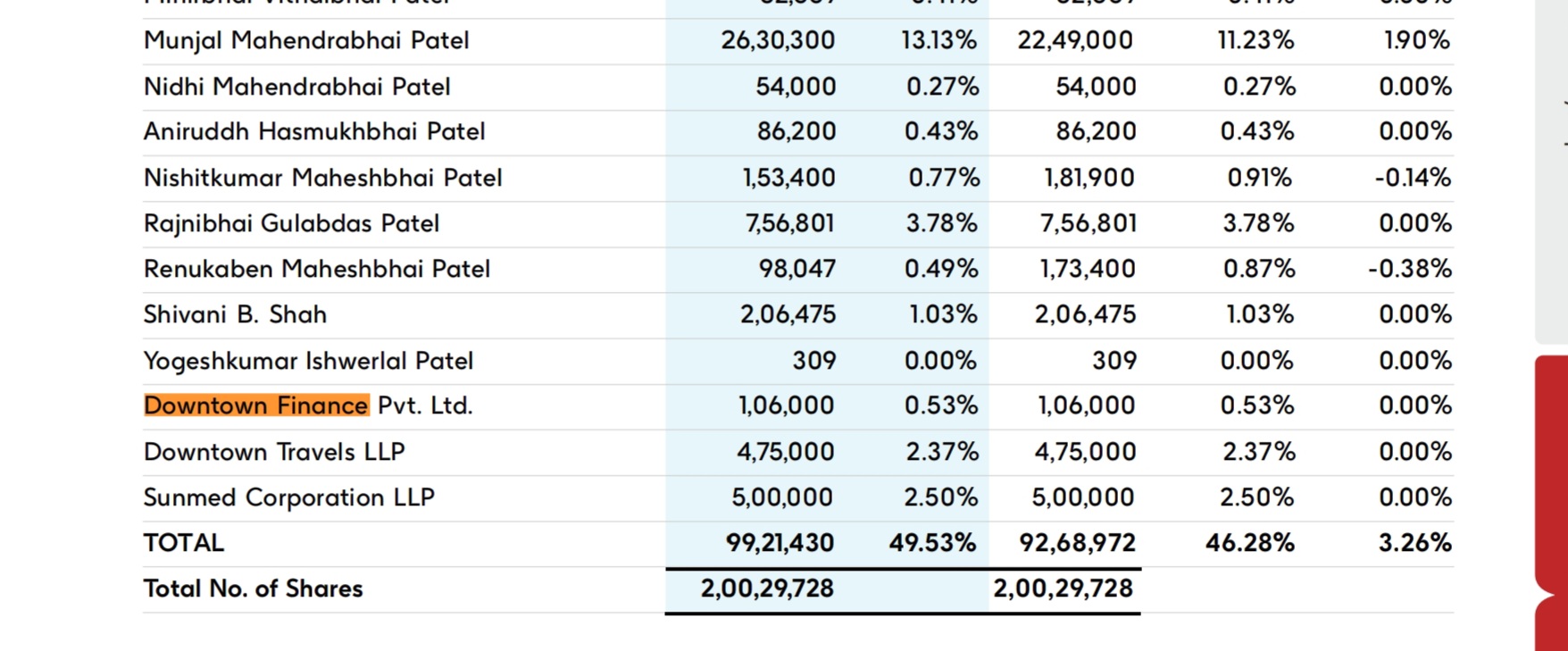

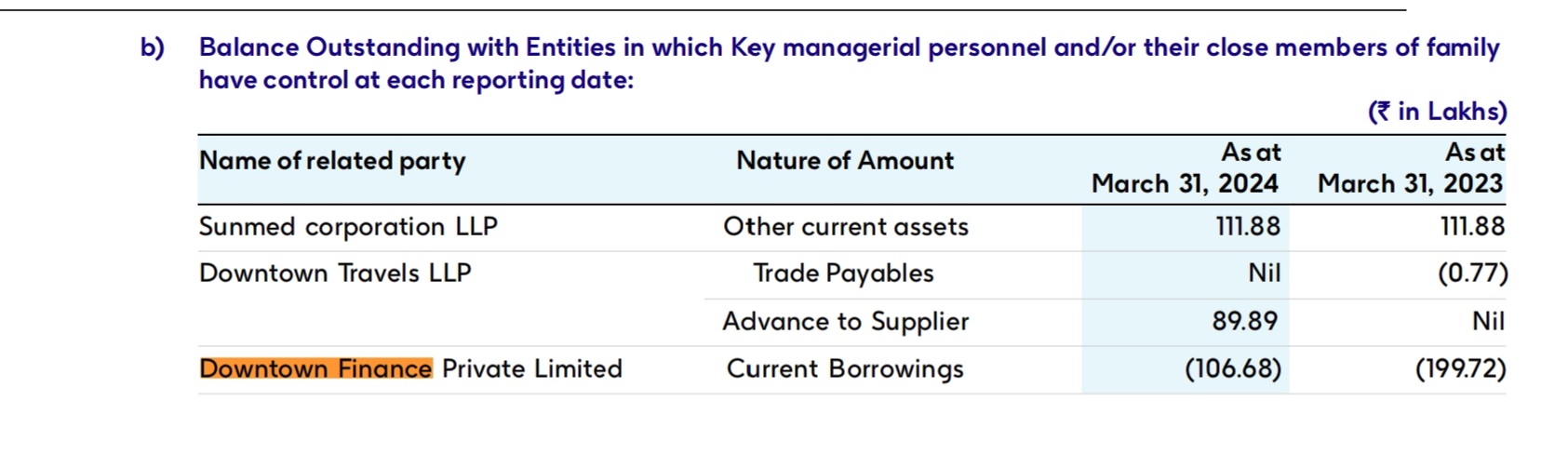

The company also lends money to Downtown Finance, managed by key personnel who invest in Lincoln Pharma shares during significant stock price declines. When asked about this, Munjal Patel stated, “We help them, and they help us,” emphasizing their reciprocal relationship.

Even after excluding fair valuations from stock trading income, the price-to-earnings ratio stands at 20, and low sales growth since 2016 likely contributes to this low P/E ratio.

[My view] Additionally, being a debt-free company, Lincoln Pharma has the flexibility to take risks and generate capital from various sources, including stock trading, which it can ultimately reinvest in its business. If revenue increases in the near future, the price-to-earnings ratio could rerate to 35 or higher, potentially pushing market capitalization beyond 5,000 crores and positioning it as a potential multibagger.

Moreover, cephalosporin developments are in the final stages and are expected to be monetized soon. According to management, this could boost revenue by 250 crores, serving as a significant growth trigger for the company.

Disc: Invested

| Subscribe To Our Free Newsletter |