I have been meaning to do detailed write-ups on Ceinsys and Genesys but haven’t found the motivation to do so. I think I have done numerous posts in the bull therapy thread over the past year though on both and don’t want to repeat the same mundane details from concalls, presentations and ARs. Anyone with a bit of motivation can find those details themselves.

Of late though I noticed a slew of orders won by Ceinsys (Order book had stood at 750 Cr before these)

- 29 Cr CIDCO order for GIS implementation with drone survey and basemap creation (3 yrs)

- 331 Cr SWSM/WSSD, MH Gov order for IoT deployment including design, implementation and maintenance for Jal Jeevan mission in MH phase 2. They had done a similar order in ’22 in phase 1 (2 years impl. + 5 yrs maintenance)

- 28 Cr MHADA order for Land Management System, GIS mobile app, (2 years + Maintenance for 3 yrs)

with these, of course order book has crossed 1000 Cr and not adjusting for runoff during the quarter, should be around 1150 Cr. All these new orders are firmly in the Geospatial space which again affirms the strong tailwind we are going to see in this space in the coming years. I believe we may have just started here.

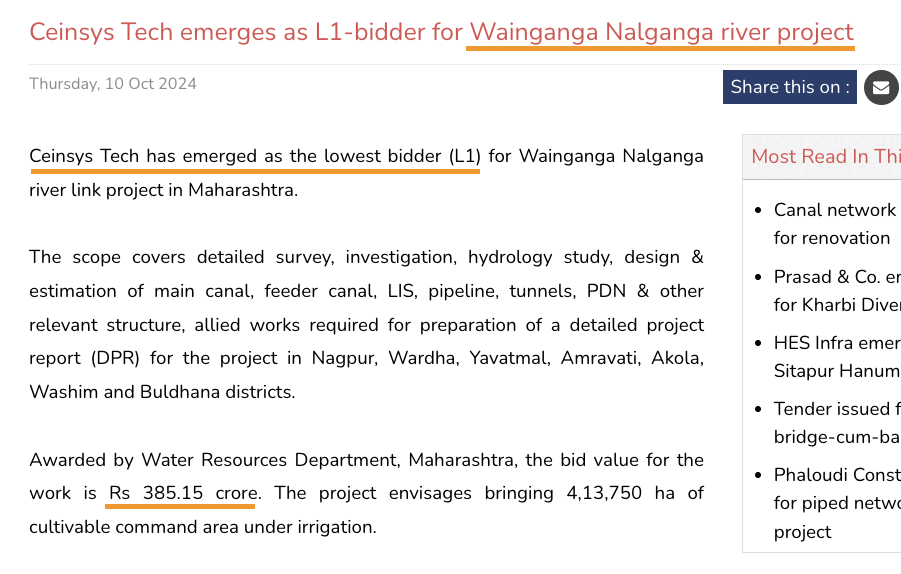

Now onto the interesting part. While looking up these tenders and scope of work etc. I stumbled upon this article.

Initially I was confused and thought this must be same as the 331 Cr order recently reported but realised upon double-checking that the disclosed order win for was SWSM while this one is for WRD (Water Resources Department). The scope of work as well is completely different with one being for IoT deployment for Jal Jeevan mission (drinking water) while the other is for Wainganga-Nalganga river linking for irrigation of 4.14 lakh hectares of land in the Marathwada/Vidarbha regions. The bid amount as well is 331 Cr vs 385 Cr and timeline 2 years vs 6 months (which I realised after I double checked the tender online)

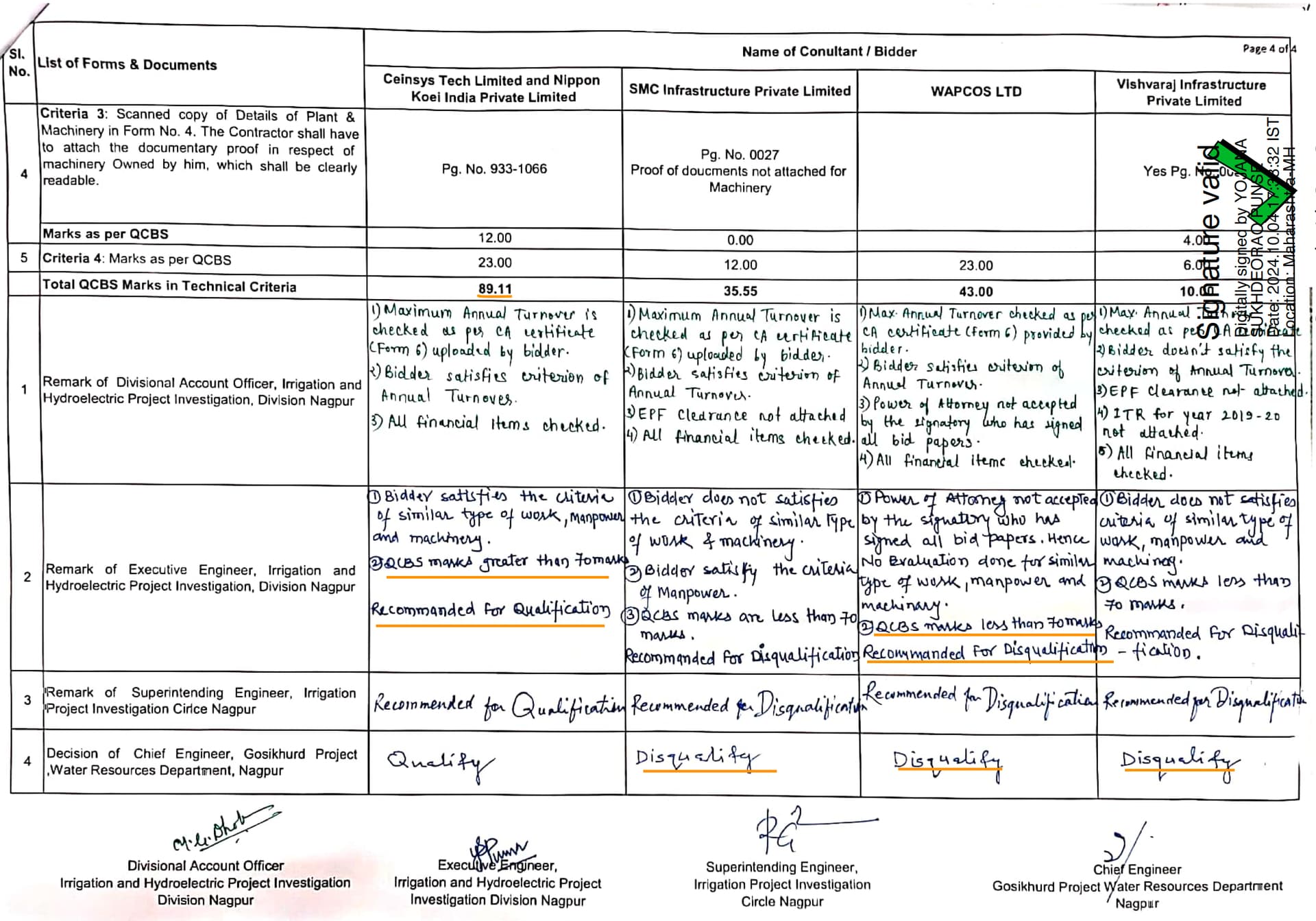

In the tender technical details doc, I found some very interesting stuff – like how exactly was the tender awarded to Ceinsys. (You can get these docs from any of the tender assistance sites for a small fee)

There were a total of 4 bidders for this tender and the other three were disqualified in QCBS (quality and cost based selection) as they did not score above 70. Others scored 35,43 and 10 while ceinsys scored 89.

Now to understand what gave ceinsys the edge, I re-read the tender doc and also the result detail doc and this is what I found

-

Similar type of work with value > 115 Cr done in the past – ceinsys scored 16.30 here while rest scored 0. Ceinsys was the only one with prior experience in this sort of project.

-

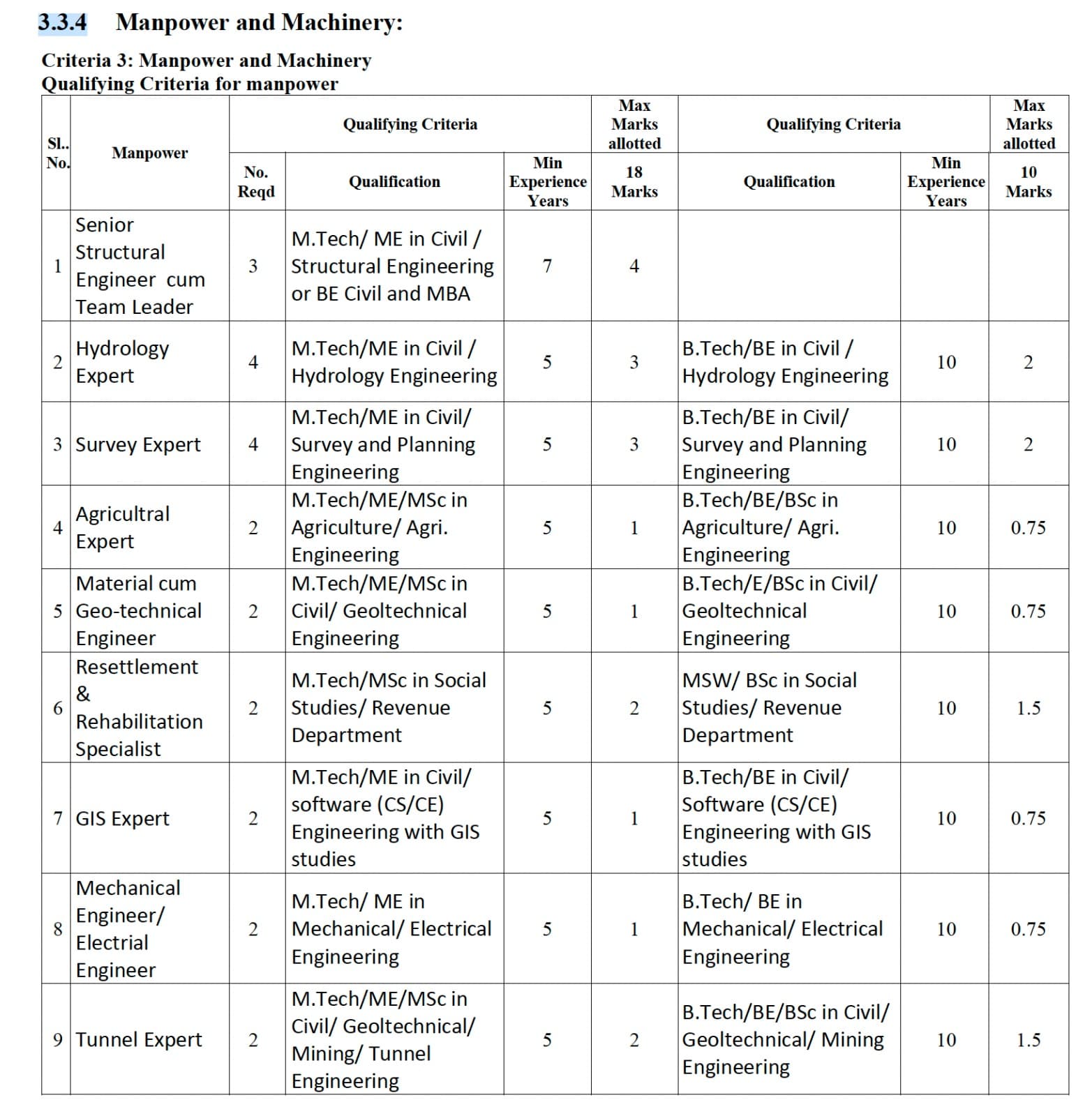

Technical personnel (structural engineer, hydrology expert, agri expert, GIS expert, tunnel expert, resettlement expert, survey expert etc.) ceinsys scored 18 here while closest did 6. I dont know how many other companies would have hydrology, GIS/Survey, Agri, Structural engineer and resettlement and rehab specialist on their payrolls.

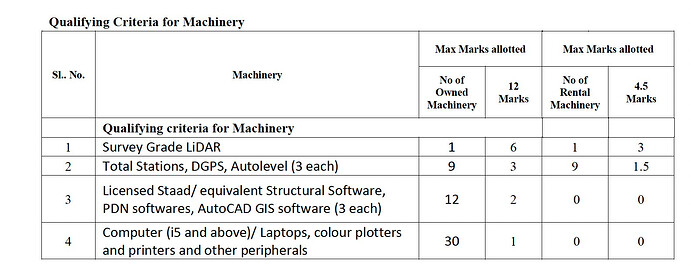

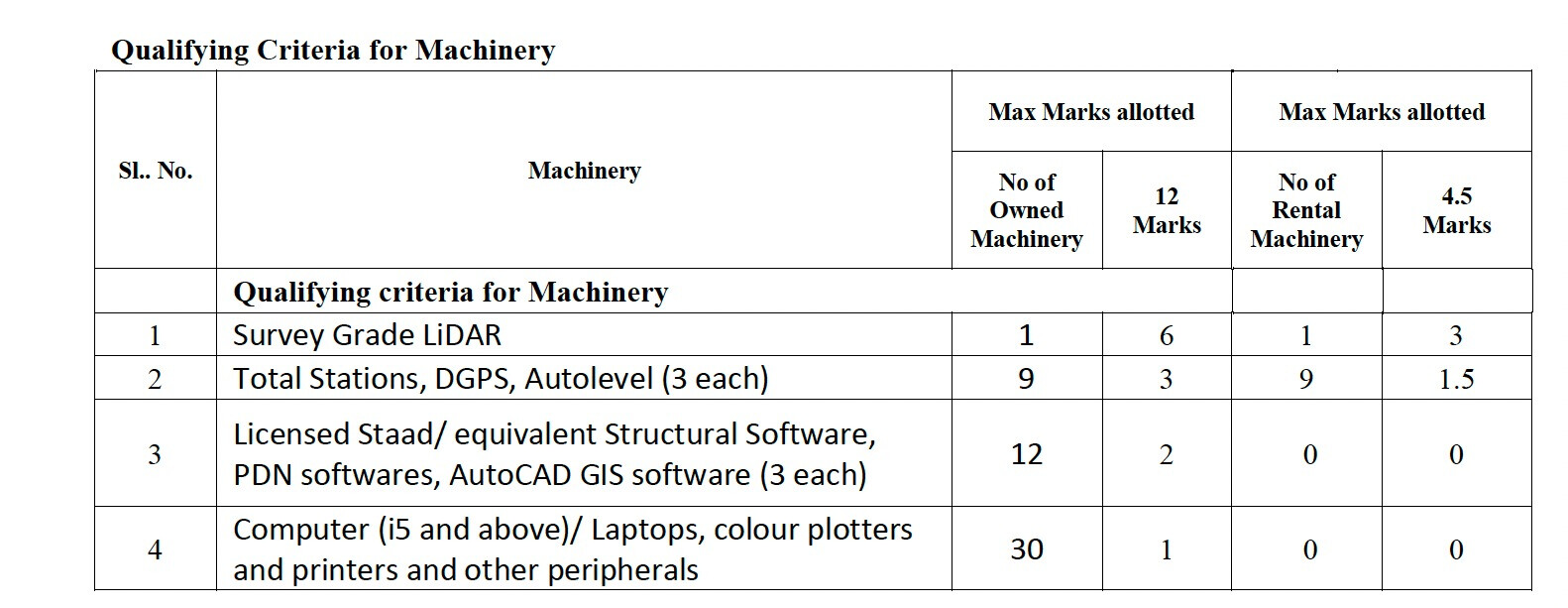

- Plant and machinery for LiDAR and other things. ceinsys scored 12 while rest did 0

It makes better sense now why ceinsys say they win 90% of what they bid but they are very selective on what they bid. Its perhaps the confluence of skillsets, equipment, experience and capital. Its possible and you can argue that the tender criteria itself is skewed to support Ceinsys but to me it looks like a fair evaluation of prior experience, capability and ensuring the people and equipment are present and the other bidders weren’t even close on this basic evaluation.

This is just a L1 bid award as of now. Not sure how long this becomes a LoA and I would assume Ceinsys would notify the exchanges only post that (hopefully there’s no slip from now to then). If you are interested in understanding this project, then check this and this. The whole project outlay seems to be a whopping 87k Cr and seems to have been approved in August (probably a big poll plank in the drought hit Vidarbha/Marathwada regions). I feel a bit more confident that though there is political risk, the company’s capabilities can’t be denied. The funds have been raised from promoter and FPI as well, so an acquisition abroad can’t be far away and along with the allygrow/allygram and data center business, the govt. dependency should reduce which will make this quite a robust business.

Disc: I am invested in Ceinsys since Oct ’23. No recent transactions. I am not SEBI registered and these are just my opinions and please don’t act based on this without further research.

| Subscribe To Our Free Newsletter |