Hello everyone,

I’ve been developing a risk management algorithm that adjusts the stop-loss dynamically based on previous trading performance. This algorithm responds to the trading results, expanding the stop-loss during winning streaks and contracting it after losses, allowing for more calculated risk-taking while aiming to preserve capital.

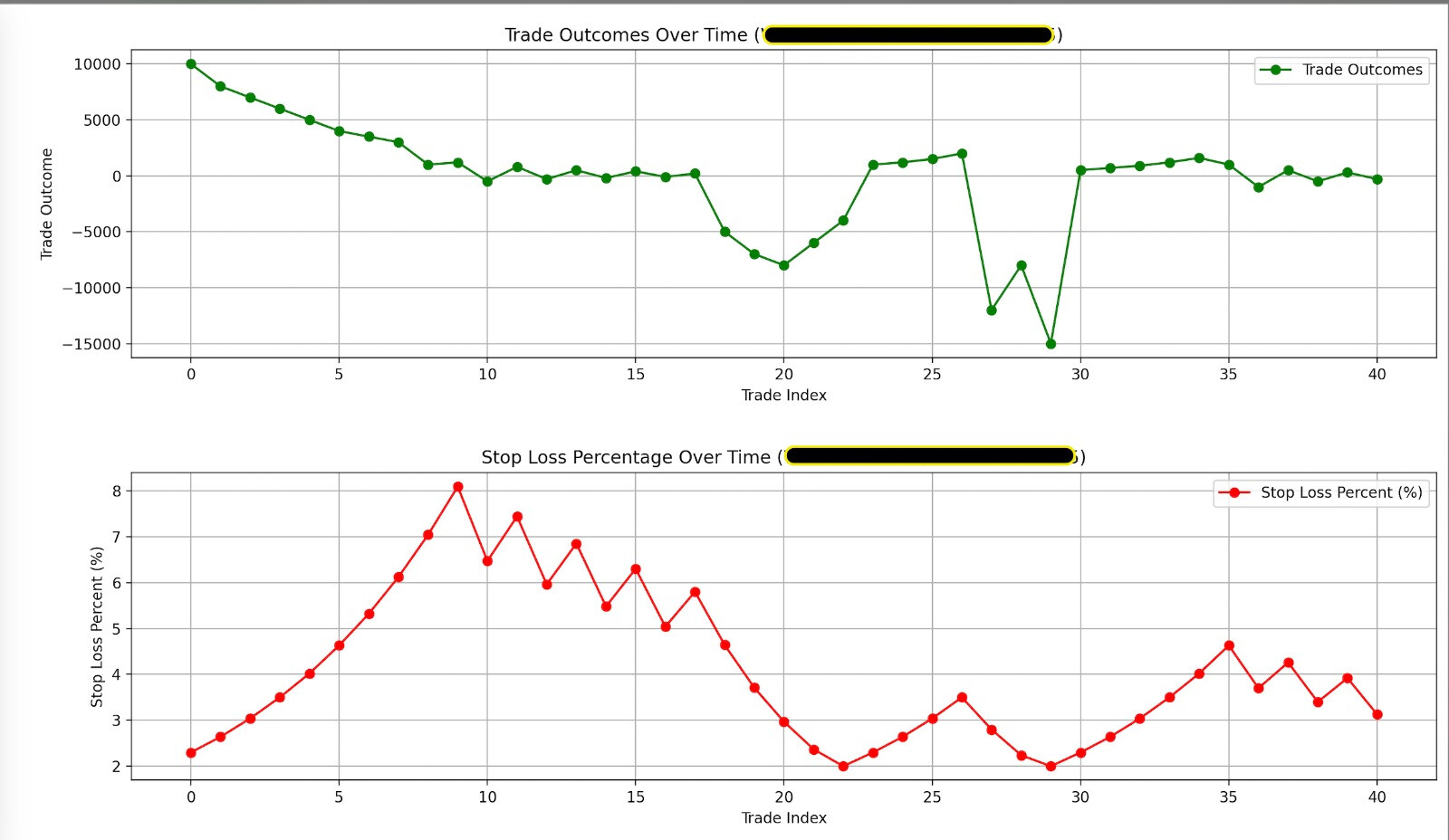

I’ve included two charts below to illustrate how this works:

- Top Chart: Trade outcomes over time, demonstrating a mix of winning and losing streaks.

- Bottom Chart: The stop-loss percentage over time, dynamically adjusting to the results of previous trades.

Additionally, I’ve shared the test data (visible in the screenshot) that reflects various market scenarios such as:

- Strong winning streaks

- Choppy market conditions

- Sharp reversals to losing streaks

- Sudden large losses

- Recoveries after losses

You can correlate the graphs with this test data to better understand how the algorithm responds in different market conditions.

Key features:

- Increases stop-loss after winning trades, allowing for more risk.

- Reduces stop-loss after losses, limiting further risk exposure.

- Minimum stop-loss is capped at 2%, ensuring a base level of risk management.

I’d love to hear your thoughts on this approach. Does this dynamic stop-loss strategy align with your risk tolerance and trading style? Are there any improvements or tweaks you would suggest?

| Subscribe To Our Free Newsletter |