Axiscades is a Bengaluru headquartered company involved in the six business segments – Aerospace, Defence, Automotive, Energy, Product Engineering (Semiconductors) and Heavy Engineering. The company looks interesting to me due to following few top-level things –

- Company had large high-cost debt due to Mistral acquisition. Company raised 220cr from QIP done in Jan 2024 and this high-cost debt will be retired – which would result in lower interest cost (56cr in FY24 to 30cr in FY25) and improve EBITDA to PAT translation.

- Mistral Defence business has two segments – prototyping which is -ve single digit EBITDA margins business and defence production business is 25-40% EBITDA margin business. The defence production business delivered 112cr in revenue in FY24. The company has guided for 170cr revenue for FY25 and 225-250cr revenue for FY26 in defence production.

- Tejas and Sukhoi are large opportunities for the company where company can supply products worth ~8cr. The commercial production of LCA Tejas (around 16-24 per year) and Su30 upgrades (around 50 per year) would gain traction starting FY27. Our projection is that defence production revenue can cross 500cr when this starts.

- Heavy engineering is a legacy business of the company where Caterpillar is major customer. This business is a staffing business, and it was -ve EBITDA (-3%) margin for the company. The company is looking to achieve mid-single digit EBITDA margins in FY25 and can achieve low double digits in FY26.

- Aerospace business is a large business for the company and it is growing at high rate and it is expected to continue. Airbus is the largest customer of the company with dedicated ODC. Airbus is looking to ramp up production to 700 planes in next 1-2 years and looking to go to 1000 planes per year over medium term as it has order book of 3000 planes to be delivered. The issues faced by Boeing 737 Max are helping Airbus to grow at fast pace.

Now let us get on to segment by segment details.

MISTRAL ACQUISITION

Let us first go into history of Mistral acquisition. The owners of the company realized that Defence space is about to explode in India and was looking for some acquisition in India.

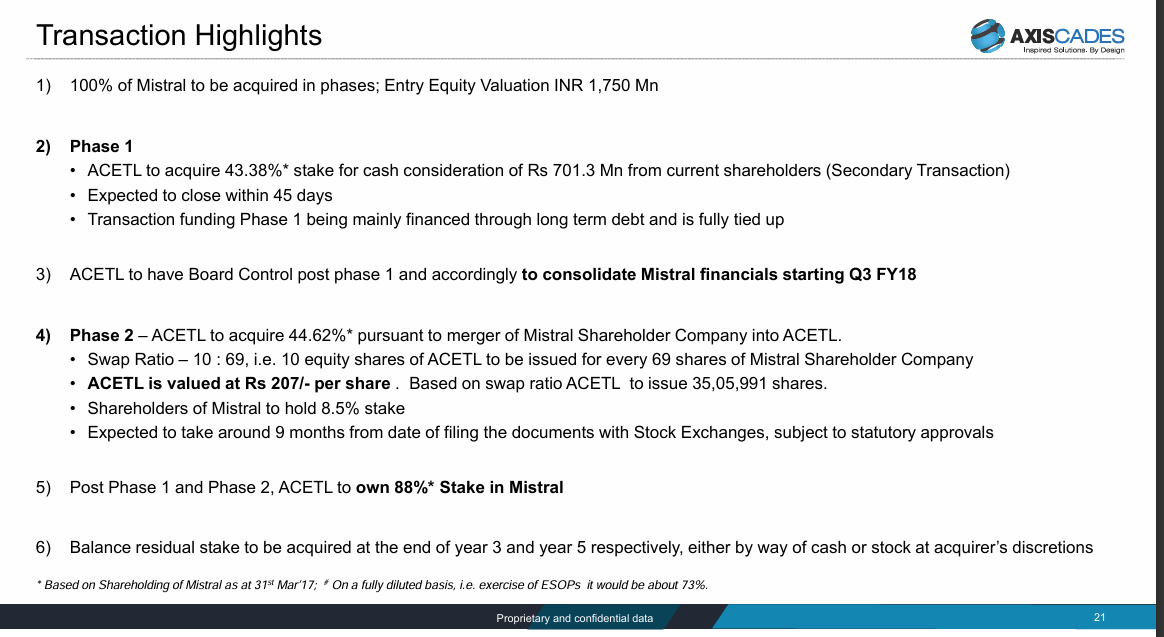

The company zeroed in on Mistral Solutions Limited – a company working in defence space for 20+ years at that time. Axiscades was a small company at the time (~500cr m-cap, 500cr revenue and 30-40cr normalized EBITDA). The Mistral acquisition was going to cost 200-300cr and they did not have balance sheet to support it. So the company decided to do the acquisition in 4 phases over time using debt and equity swap.

Post phase 1 or phase 2, Data Pattern listed at something like 4500cr m-cap at 70-80 PE. Post this, valuation concerns emerged, and disputes erupted between the parties.

The case went to NCLT and went on for 2-3 years. Finally, Axiscades was allowed to buy out Mistral but they had to pay a lumpsump for phase3/phase 4 and plus interest at 12%. This is when the company has to take large debt at high cost in short time.

The Mistral acquisition is now complete, and it is a wholly owned subsidiary of Axiscades now. The company raised ~220cr in Jan 2024 at the price of approx ~660. This is being used to retire the high-cost debt taken. At the end of Q1 FY25, the net debt in the balance sheet is 50cr.

MISTRAL DEFENCE

Before going into Mistral defence, some basics first –

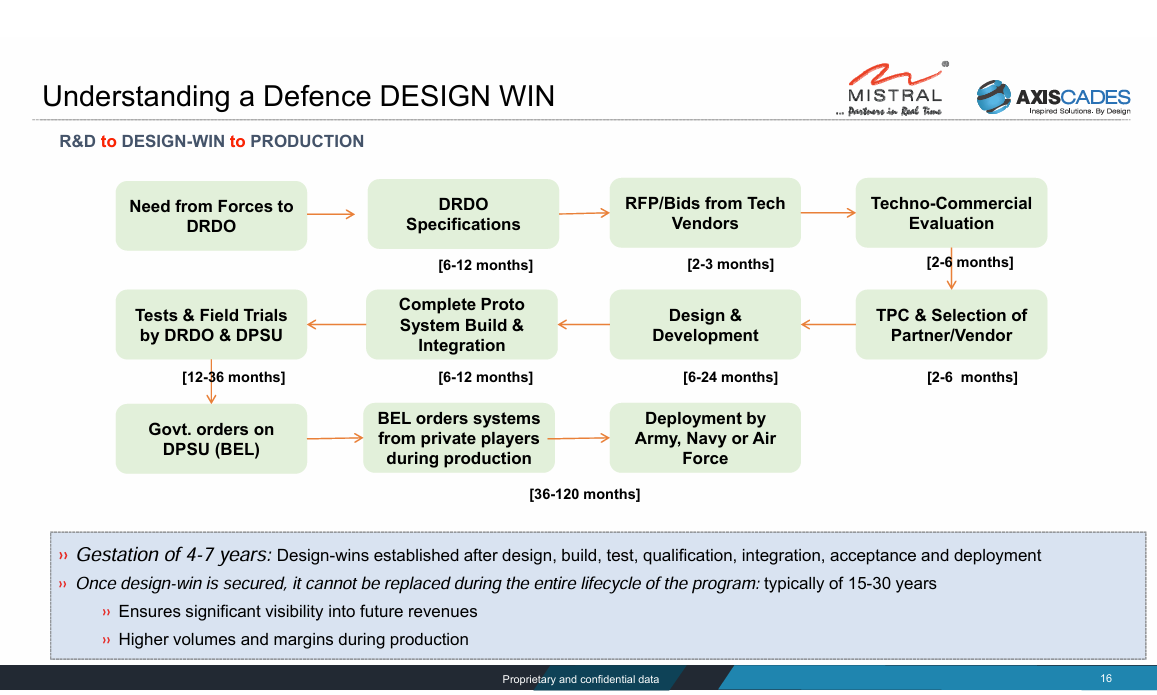

Defence involves two distinct phases – prototyping and production.

As can be seen from above, prototyping is a long process where it can take 4-7 years. Prototyping is a competitive space as if you are not into prototyping, you cannot win production orders. Prototyping margins range from -ve EBITDA margins to 10-15% EBITDA margin – varying between project to project.

But when these prototypes go into production – the vendor cannot be replaced, and you will continue to get orders for 15-30 years. Production is 25-40% EBITDA margin business.

We want to invest in a defence business at the inflection point where defence production business is going to become larger and larger for them. This is what happened to Data Patterns starting FY20 onwards – where margins went to 28% in FY20, 41% in FY21 and so on. Prior to that margins were in 16-18% type range.

This is exactly the inflection point where Mistral Defence is as you will see later.

Now let us talk about the most exciting vertical in the whole piece – Mistral Defence. When Axiscades acquired Mistral, they came out with a detailed presentation on Mistral in Nov 2018. This presentation is a must read to understand Mistral. Another good presentation is Nov 17 PPT –

179f51f7-9e39-4ce5-b56f-de8801fb11ad.pdf (bseindia.com)

Some of the slides from the presentation are captured here.

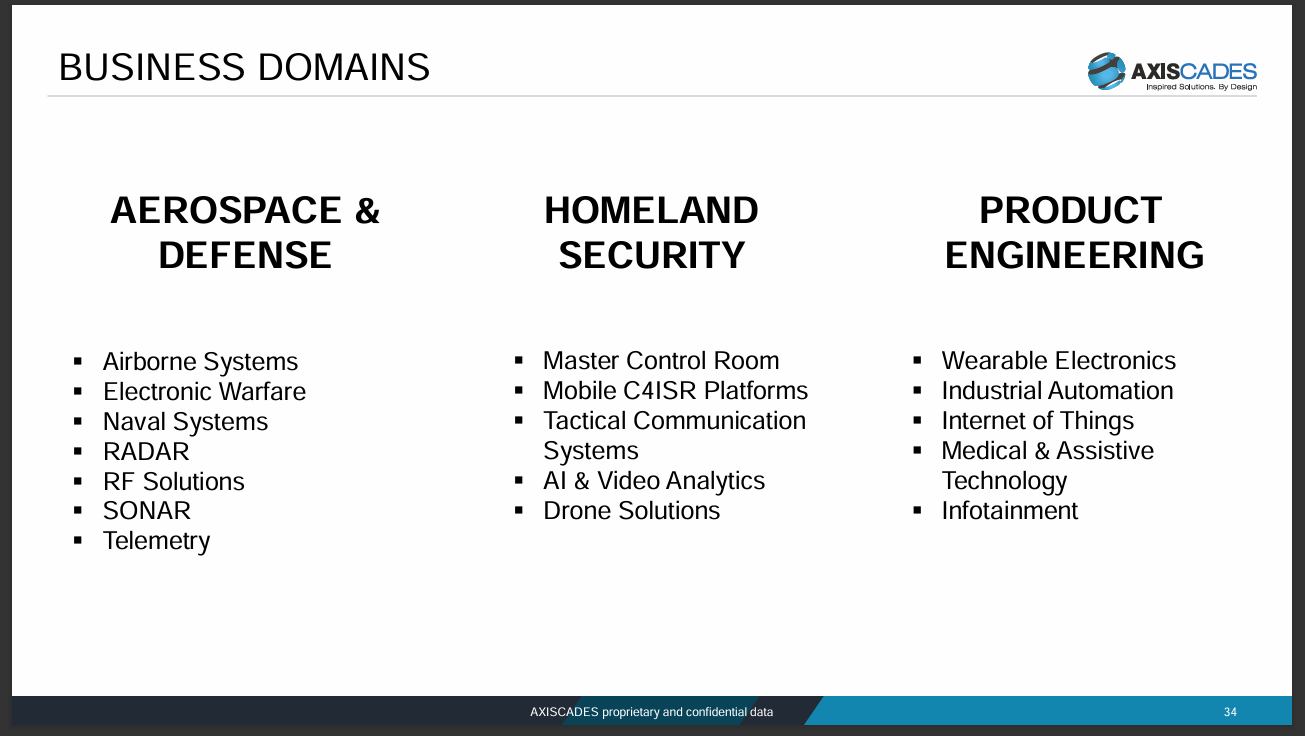

Mistral works in 3 segments – Defence, Homeland Security and Product Engineering.

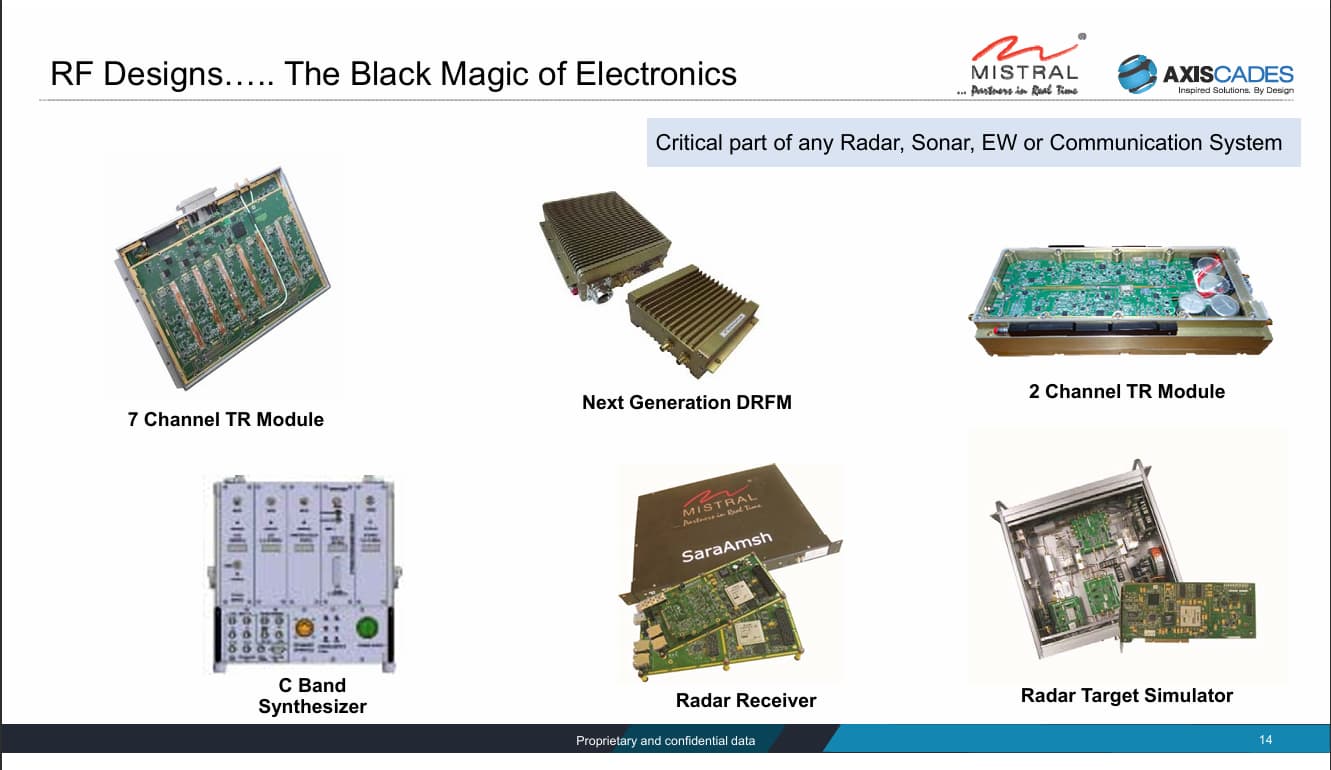

In Defence, company works in radars, sonars, telemetry, electronic warfare (EW) systems, airborne & naval systems.

Above diagram shows some of the products of Mistral, I will list some of them –

- Medium Powered Radar – This is Arudhra radar for which company won a contract worth 90cr for 8 radars recently.

- Low Level Tracking Radar (LLTR) – This is Ashwini LLTR radar. The tender for this is currently open and active bidding is ongoing between BEL/Data Patterns/Astra Micro and Mistral. This is likely to be 50-60cr opportunity for Mistral.

- AEWAC Radar Processing Unit (RPU) – This goes into Netra EW system. Recently Adani was declared L1 for Netra 2 project and Mistral would be supplying this component to Adani Defence.

- Front End Processing for Ship Sonars – these are applicable for ongoing ships and new ships.

- Multi Function Radar – There is an active order from BEL to Cochin Shipyard worth 850cr for Multi-Function Radars ( 0539bf8d-1b29-4088-9ede-7d5093316e60.pdf (bseindia.com) ). We are trying to figure out the value of components that Mistral would be supplying.

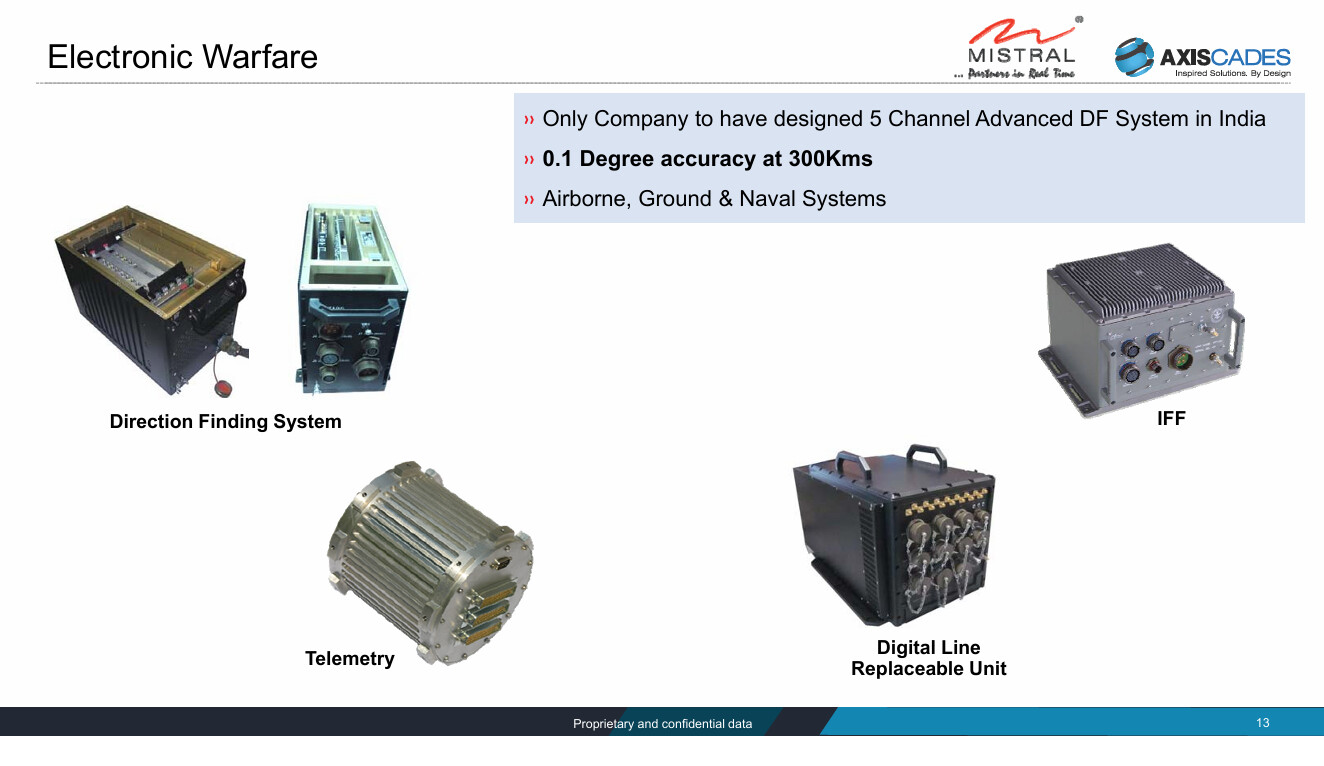

Above image shows the products used in Electronic Warfare (EW) systems –

- Direction Finding (DF) systems – these are used in EW and Mistral has good expertise in this area.

- Identification of Friend of Foe (IFF)

- Telemetry systems

The company is also involved in various sub-components of Radar, some of them are listed above –

- TR Module – is transmitter receiver module

- GaN based transmitter receiver modules which are mostly used in AESA Uttam Radar.

The company also supplies secondary board computer (SBCs) for various aircrafts.

These are some of the highlights of products and there are many more. This just demonstrates the wide range of products that they have developed. @YachnaBhatia and I have done some work to figure out various details of several of these products.

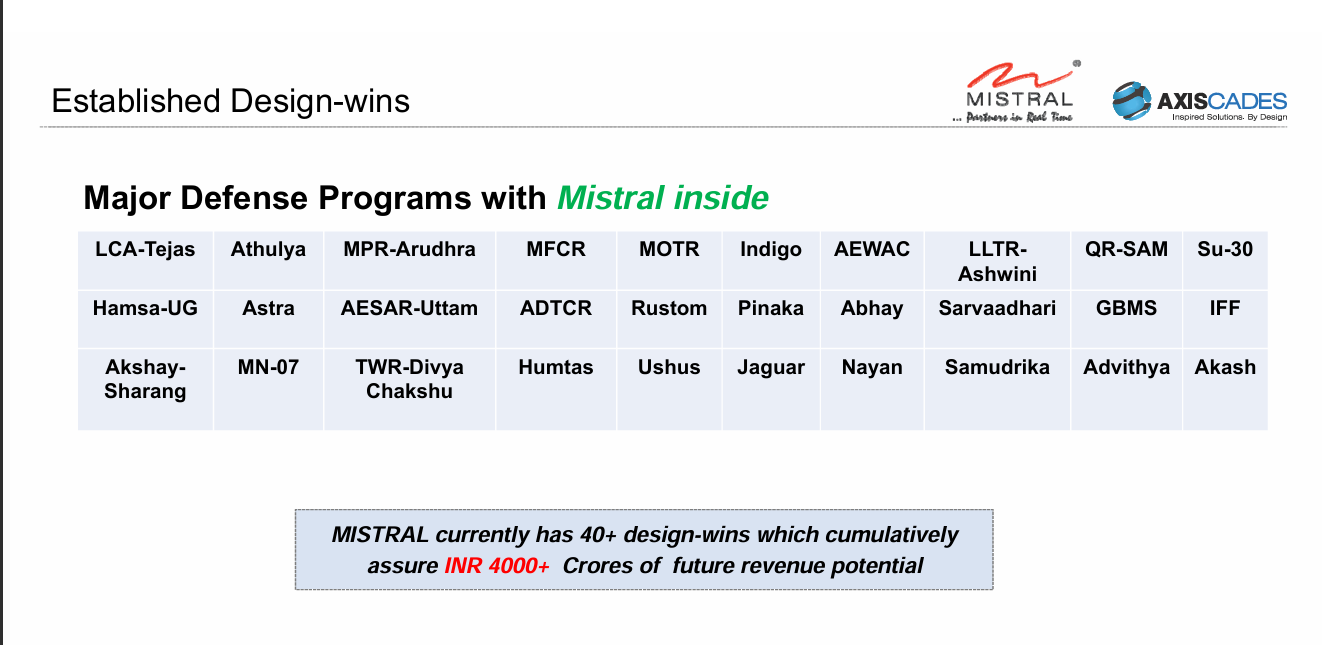

But all of this can be abstracted and summarized in two slides –

The company has 40+ design wins across above programs and there is potential to get 4000-5000cr worth of revenue over next 10 years.

The breakdown of of 4000cr orderbook can be done as follows –

- Light Combat Aircraft (LCA) Tejas – Mk1 & Mk2 – roughly 1200cr opportunity

The company supplies parts of avionics like SBC or video/graphics components. The company would also be supplying some component of Uttam Radar that will be used in Tejas – like exciter receiver and RPU. First few Tejas (between 20-40) would be using Israeli radar and then later versions would be using Uttam AESA radar. Indian Air Force (IAF) is looking to procure ~200 Tejas over next 8 years. Per Tejas contribution would be about 8-9cr. So this is roughly 1200cr opportunity (150 * 8) over 8 years. Currently HAL has production capacity to produce 16 Tejas per year, they are looking to take it to 24 soon. Tejas is facing delays as GE is unable to deliver engines. There are news articles that supply of engines from GE will start from Nov 24. Tejas opportunity will become meaningful for Mistral starting FY27. - Su-30 mid-life upgrades – 2000cr opportunity

GoI is looking to upgrade around 230-250 Sukhoi aircrafts with radar, avionics etc. Mistral is involved in multiple sub-systems in SU-30 and per aircraft opportunity is ~8cr. This program is currently in development phase and commercialization is expected to start after 2.5-3 years i.e. H2FY27 or FY28. - Airborne Electronic Warfare & Combat Systems (AEW&CS)

There is ongoing production/supply of Netra 1 EW systems. Adani Defence was recently declared L1 for Netra 2. Then there is Samudrika program which is basically a Naval EW program. Samudrika has 7 EW programs inside it – Ship Borne Systems (Shakti, Nayan, Tushar) and Air Borne Systems (Sarang, Sarakshi, Sarvadhari, NIkash). It is WIP to figure out exact timelines and opportunity size but ~300cr opportunity is a fair estimate. - Ashwini Radar – 50-60cr opportunity

Ashwini radar would be 50-60cr opportunity for Mistral and tender is under active bidding. - Others – 2000cr opportunity

There are other programs on which clarity needs to be built. Some of them are –

- Naval Radars/Sonars

- Rustom UAV program

- Dornier-228 Upgrades

- QRSAM – Battery Multi-Function Radar (BMFR), BSR – Battery Surveillance Radar

- Long Range Radar etc.

- Naval Programs – P75i, P76, Indigo etc.

I think all of the above combined would be 1500-2000cr type of opportunity over next multiple year.

The management has guided for defence production revenue of 170cr in FY25 and 225-250cr revenue for FY26. And as we can project that when both Tejas and Sukhoi programs go into production (24 Tejas per year and 50 Su-30 upgrades per year) – both of these programs itself represent 600cr kind of opportunity. So one can see that FY27/FY28 would be major step jump years for Mistral.

I can write more details about Mistral Defence but above is comprehensive summary of things.

AEROSPACE

Axiscades has strong presence in Aerospace vertical where it did the revenue of 280cr in FY24 and 80cr in Q1 FY25.

Airbus is the largest customer for Axiscades. Due to issues with Boeing and specifically Boeing 737 MAX, Airbus has order book which is overflowing. Airbus is looking to produce 700 planes in this year and looking to ramp up to 1000 planes per year as they look to fulfill order book of 3000 planes.

Axiscades works across four areas –

- Product Design

Design of certain parts of the new products, new aircrafts. e.g. whenever new models come like A350, A380 etc. - Concession Management

This is linked to volume of the aircraft. As one can see, production of aircrafts is slated to grow over next 3-4 years. - Repair Work

Engineering assessments of the defects. This is also linked with volume of aircraft in the operations. - Manufacturing Engineering

This is basically plant engineering – designing of new plants, increasing throughput existing plants

In Q3 FY23, Airbus renewed the contract with Axiscades. The contract value is 75mn$ over 3 years.

In Q4 FY24, company won a contract of 18mn$ with an Aerospace OEM – in the areas of repairs and manufacturing support.

In AGM24, the company said that they are currently engaged majorly with OEMs. The company is also looking to engage with MROs (given major MRO centers are going to come up in India), Engine Manufacturers, Avionics and Landing gear manufacturers.

My expectation is that this business will continue to grow 15-20% for next few years at a minimum. One of the risks to growth is issue with Pratt & Whitney engines that Airbus is facing.

HEAVY ENGINEERING

This is a legacy business for Axiscades where Caterpillar is the largest customer. Historically, this was developed as staffing business with low margins. Actually, company had -ve EBITDA margins in this space in FY24 on the revenue of 152cr.

The company has small +ve EBITDA margin in Q1 FY25 and it looking to deliver 5-6% margins in FY25.

My expectation is that this business will reach double digit EBITDA margins in FY26 with 10-15% growth.

PRODUCT ENGINEERING (SEMICONDUCTOR CONSULTING)

This business has two parts – consulting and production.

This division did revenue of 125cr in FY24, consulting – 67cr, production – 58cr.

In consulting space, company works to bring up, develop firmware, applications etc. on customers’ hardware. Texas Instruments (TI) is anchor customer in this space and end product segment is automotive as per my understanding. Basically, TI develops the HW chips, Mistral develops a platform and drivers/firmware around this chip – so that end auto customer can begin his application development.

The other two customers in this space are Qualcomm & Nvidia.

Once these development boards are developed, because the Volume is low – TI etc. have asked Mistral to get them manufactured through EMS partners and supply to various customers. This piece has faced inventory build up issue and has been facing degrowth since last 3 quarters. The management has guided for improvement from H2 FY25.

My understanding is that semiconductor consulting business is 30%+ margin business and production business is 10-15% margin business.

The company reported 22% margins in entire product engineering t in FY24.

The expectation of growth rate in this business is around 10-15%.

AUTOMOTIVE

This was a new segment started by Axiscades few years ago.

Then the company acquired a German company by the name of add solution, Gmbh. Volkswagen is the largest customer of add solutions and they work in the fields of HMI testing and wiring harness areas. This business delivered revenue of 103cr in Fy24 with 10-11% margins.

Automotive is a long-term growth driver as auto contributes 20-25% of ER&D industry. But this business is facing headwinds due to – Invasion of Chinese EVs into Europe. Volkswagen is going to close couple of plants in Wolfsberg after several years.

The company has also acquired JLR as a client due to connects of MD.

The expectation is that this business will be flat in FY25 and might have modest growth in FY26.

ENERGY

This is another new segment for the company. Recently company acquired a Hyderabad based company by the name of Epcogen. This company is focused on both the energy segments – oil & gas/renewables.

One of the company’s client – Highview Power – recently secured grant of 300mn pounds for the liquid air energy storage plant (LAES) in UK with capacity of 300 MWh (50MW, 6 hours). My understanding is that consulting cost is 1-2% of total project cost in such deals. Highview Power has plans to go 2 GWh over a period of time in UK.

The company is looking to hire 50 engineers in its Hyderabad office as per my search.

The company is also opening office in Dubai – to focus on Tier 1 vendors of large oil & gas majors.

This business did revenue of 33cr in FY24. This business is expected to grow at fast pace and has margins of 20%.

THE X-FACTORS

Outside of this, there are few interesting areas where company is present, and they can become large opportunities if things work out –

- Axiscades Aerospace Technologies Limited (ACAT), subsidiary of the company, had received the order for around 100 counter drone systems. The deliveries are slated to happen over FY25. Some of these counter drones are installed in Manipur. The company claims that this segment has opportunity size of 3000cr. In AGM24, the company said that they are discussing two follow on orders in this space. This is a competitive space with players like Zen Technologies, Adani Defence. We need to see the progress of the company in this space.

- Mistral has spent significant effort in developing products in the space of Homeland Security. Recently they announced deliveries to GJ government of Mobile Command & Control Vehicle. We need to track and see if this can become 100cr kind of segment for the company.

- Mistral is also working on developing drones for defence applications. One can check details of their models – XHERPA, FALCON RAAD, HOUND, STEALTH. Currently, Army spends around 600cr to maintain mules etc. which deliver supplies to Army outposts in remote areas in mountains. Idea is to replace these with drones. Recently, there were trials of drone manufacturers in Ladakh and Mistral participated in that. We need to see if some commercial orders come through in this space.

- The company has technical strengths in the area of mmWave radars. mmWave radars work at high frequency bands and they have short range but better accuracy. These radars find their applications in ADAS systems as well. In AGM24, the company said that they are engaging with some ADAS players for mmWave radars.

VALUATION

The company has given guidance of 1600cr sales and 160-180cr PAT in FY26. This assumes some inorganic growth as well.

Given some developments in Automotive, Pratt & Whitney engines issue and B2G risk in defence orders, my expectation is 1400cr sales and 140cr PAT for FY26.

The company is trading at 16x FY26 PAT as of now. One can see valuations of ER&D companies and Defence companies and determine whether the company is undervalued or not.

RISKS

- B2G Risk

A lot of Mistral Defence growth would be from MoD, Indian Navy, HAL, BEL, Cohin Shipyard etc. This segment is plagues by the delays and timelines – more often than not – tend to move to right. e.g. GE was supposed to deliver engines for LCA Tejas several months ago, but it is plagued by delays. - Key Man Risk

Axiscades was poorly managed with a lot of instability in top management till current MD – Arun Krishnamurthy and CFO – Shashidhar joined. They have stabilized the operations and are now setting growth targets and working towards achieving those. Muju (Mistral CEO) and Mistral senior team has deep engagements with Indian Defence industry. If Arun/Muju decides to leave the company, that would be a key negative. Arun & Shashi have stock options which will be 5-6% of total equity of the company. Hopefully, that gives them incentive to stay focused and put. - Multiple Segments

Since company works across 6 segments, at any given point of time – it is possible that one or two segments would do poorly and bring down the performance of the company. e.g. Automotive is going through a bad phase right now – but it is a small segment for the company. If Pratt & Whitney engine issue exacerbates – Aerospace segment growth might slow down. - Small size of products

One concerns that is being raised is that product size per program is very small, so several programs have to go right for the company to grow well. This is much harder than one or two programs scaling up to 500-1000cr.

This is a valid concern/risk. My only counterpoint is that this is an industry phenomenon and not Mistral specific. E.g. When Arudhra radar contract was signed, the order was split as follows – Astra Microwave (380cr), Data Patterns (180cr), Mistral Solutions (90cr).

Astra Microwave and Data Pattern are more capable companies and address larger opportunity size. But Mistral also has a place in Defence value chain and my understanding is that Mistral will get 15-20% market share in most of the radar orders. - Late Cycle Defence Investment Idea

The defence theme has already played out with enormous wealth being created over last 4-5 years. Most of the Defence stocks are down 30-40% from their recent peaks. Rerating journey for Axiscades Mistral might prove to be frustrating one.

This is not a concern from operating side of the business but more investor specific. This is a valid concern.

My only counterpoint is that – With NDA 3.0 government, one can reasonably hope that capex outlay for defence production and push for Indigenization would continue for next 5 years. The defence production outlay was ~1.7L cr in FY25 budget, with outlay for Indigenous production of about 1.05L cr. One can hope that these numbers would grow at the CAGR of 8-10% by the time we reach 2029. So operationally the business would continue to grow.

Whether to invest and whether valuations make sense is a decision that each investor has to take.

| Subscribe To Our Free Newsletter |