Interesting Hospital to lookout for given ~40-50% valuation discount to Industry.

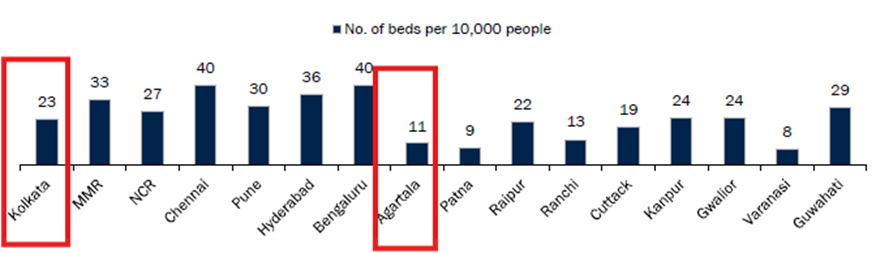

Kolkata is amongst key Tier –1 cities and Agartala is amongst the Tier –2 cities have one of the lowest concentrations of beds per 10,000 individuals

GPT positions itself as a cost-effective healthcare provider, prioritizing personalized patient care. The company’s strategy focuses on establishing smaller hospitals with 100-200 beds, unlike its listed peers who typically operate larger hospitals with 300-400 beds.

Operating as a mid-sized setup, GPT requires significantly lower capital expenditure compared to other multi-specialty hospitals in India. GPT’s average capex per bed stands at Rs5.17m, covering hospitals in tier-1, tier-2, and tier-3 cities. This is substantially lower than the industry average, which ranges from Rs12-14m per bed in tier-1 cities and Rs7-8m per bed in tier-2 cities.

Due to its strategic focus on mid-sized hospitals in high-density areas, GPT’s hospitals reach EBITDA breakeven in a relatively short time. Its Dum Dum and Howrah hospitals, which began operations in March 2013 and September 2019, achieved breakeven within 10 months and 8 months, respectively.

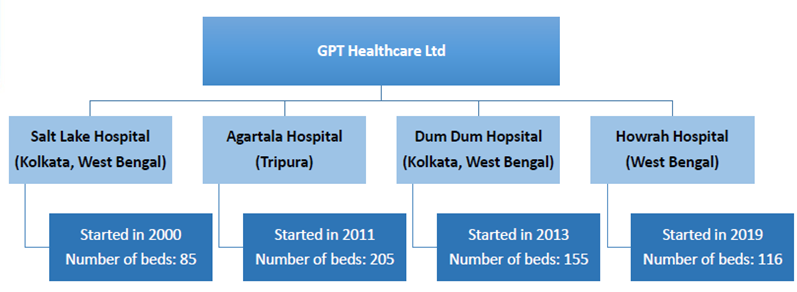

GPT currently operates four hospitals with a total capacity of 561 beds and an overall occupancy rate of around 59%, leaving ample room for growth from existing assets.

Of the four hospitals, Salt Lake (85 beds) and Dum Dum (155 beds) perform optimally, with occupancy rates of approximately 65% and 70%, respectively. In contrast, Agartala (205 beds) and Howrah (116 beds) are operating below optimal levels, with occupancy rates of 53% and 45%, respectively. Three of the four hospitals consistently generate EBITDA margins exceeding 20%, while Howrah, being a new facility, is currently operating at ~11% EBITDA margin.

As per AR and Concalls, GPT has outlined plans to increase occupancy at the Agartala and Howrah facilities, targeting 70% occupancy over the next two years while maintaining optimal levels at Salt Lake and Dum Dum.

At Agartala, GPT launched a new Cancer Care Department (Radiation Oncology) in Q1FY25 and plans to open a state-of-the-art diabetic clinic to further expand its medical services.

The Howrah hospital, which was established in 2019, was repurposed as a COVID center during FY20-23. As it returned to multi-specialty operations in FY24, the company is now aggressively scaling up the facility. Successful scale up of the Howrah facility will help it reach to >20% EBITDA Margin mark, thus contributing to scale up of company level EBITDA margins.

The company has also focused on reducing Average Length of Stay (ALOS) across all its hospitals, enabling higher patient inflows without the need for additional capacity, thus enhancing operational efficiency. The company has an ALOS of ~3.9 days in FY24 which has reduced from ~5.6 days in FY21.

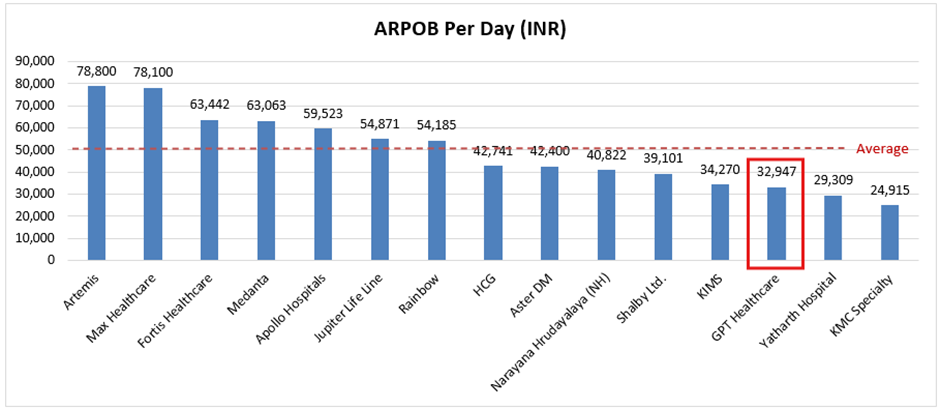

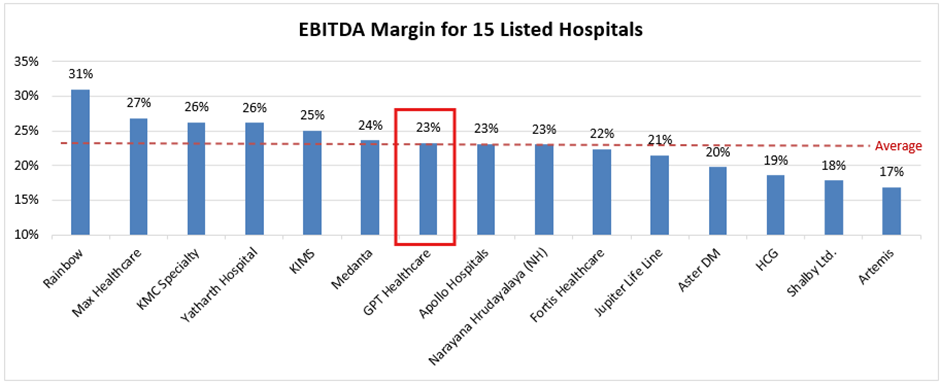

Despite pricing its services about 35% lower than its listed peers (ARPOB), GPT consistently generates EBITDA margins in line with the industry average, showcasing the company’s operational efficiency and strong financial performance.

With a 90% CFO to EBITDA conversion rate, short gestation period coupled with low-cost capex model, the company has been successfully generating 20%+ ROE/ROCE over the last 3 years.

Company has set an ambitious goal of becoming a 1,000-bed hospital chain within the next three years with opportunities in Raipur, Ranchi, and other Tier-2 cities of Eastern India.

At TTM financials, the company trades at ~16.5x EBITDA and ~2.6x EV/Bed. Whereas, the current Industry average of ~36x EBITDA and ~8.6x EV/Bed.

Disclosure: Educational purposes only, Not a buy recommendation, I am not SEBI registered analyst or advisor and I am invested in it hence my views may be biased.

| Subscribe To Our Free Newsletter |