Quantitative analysis of the company:

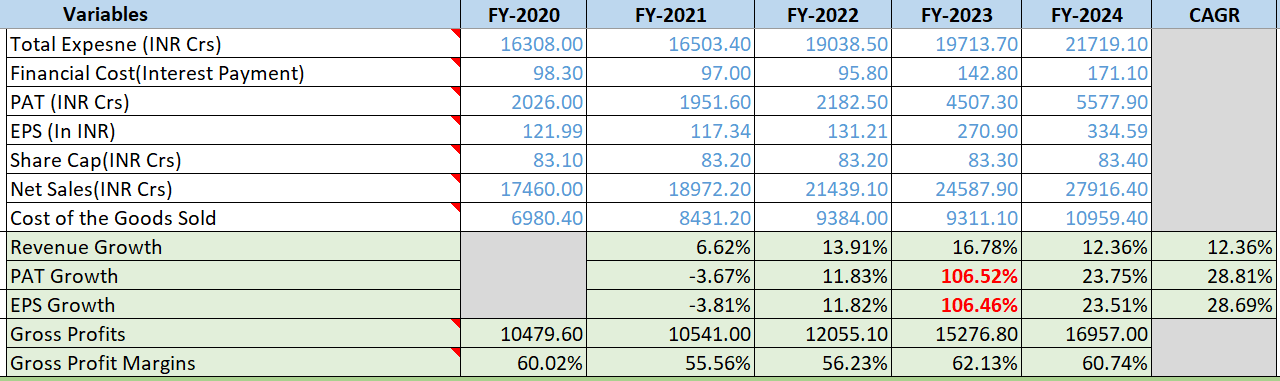

Profit & Loss Statement:

- Revenue CAGR: 12%

- PAT CAGR: 28%, with consistent year-over-year improvement

- EPS CAGR: 28%, also improving year over year

- Gross Profit Margins: Steadily hitting 55+% YoY

There is a spike in PAT & Earning growth in 2023 due to a combination of an increase in Other income, Foreign exchange gain and a reduction in tax

Other Income contributions were Rs.1055.5cr in 2023 vs Rs.484.4cr in 2022.

Details: During the year ended 31 March 2023, the Company entered into a Settlement Agreement with Indivior Inc., Indivior UK Limited and Aquestive Therapeutics, Inc Pursuant to the agreement, the Company will receive payments totaling U.S.$ 72 by 31 March 2024. The said agreement resolves all claims between the parties relating to the Company’s generic buprenorphine and naloxone sublingual film including Indivior’s and Aquestive’s patent infringement allegations and the Company’s antitrust counterclaims.The Company recognised the present value of the amount receivable at `5,638 (U.S.$ 71.39 discounted to present value) on the date of the settlement as other income.The aforesaid transaction pertain to Company’s Global Generics segment.

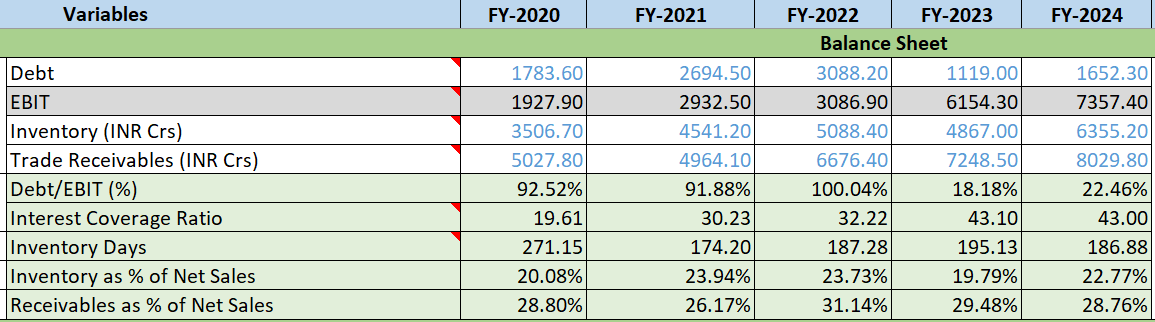

Balance Sheet:

- Debt to EBIT Ratio: Debt/EBIT % is fluctuating but reduced

- Interest Coverage Ratio: Consistently improved YoY, reflecting sound financial management

- Inventory Days: Inventory Days were increasing but only reduced this year and PAT is increasing indicating growth start.

- Receivables as % of Net Sales: Receivables as % of Net Sales is shown downtrend from 3 years, which is encouraging.

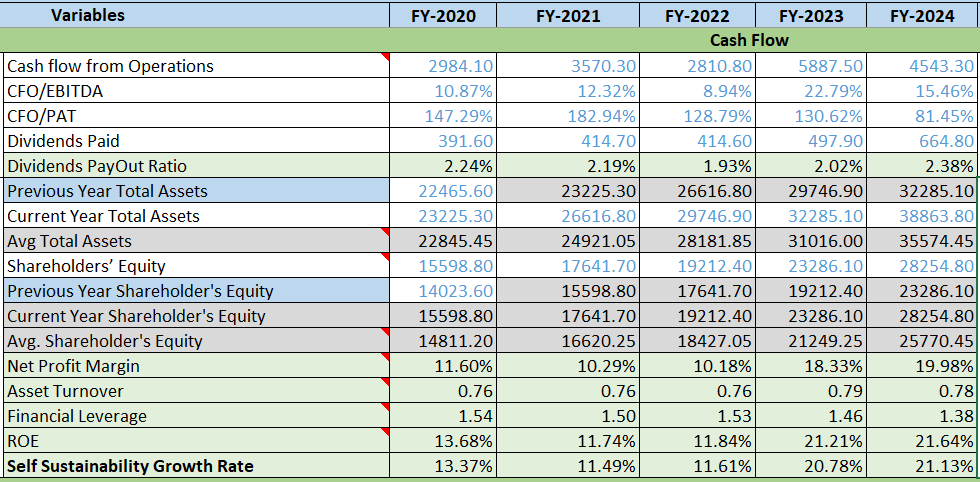

Cash Flow Statement:

- Net Profit Margin: Increasing Trend from past 3 years

- Asset Turnover Ratio: Consistent around 0.76-0.78 would be good if it starts increasing.

- Financial Leverage: Decreasing, a good sign. would be good if its less than 1.

- ROE: Increasing and hitting above 20% from 2 years

Free Cash Flow:

Positive and increasing FCF and FCF as % of Sales is greater than 5%

Valuations:

DCF Method considering avg 10% growth for 10 years, 3.5% Terminal Growth Rate, and 8% discount rate.

Conclusion:

Overall, while Dr. Reddy’s Laboratories faces some regulatory challenges, the company remains proactive in expanding its global presence, especially in consumer healthcare and biosimilars. Its diversified portfolio and strategic collaborations indicate a long-term vision for sustained growth. Currently, the stock appears to be fairly valued, if not slightly undervalued. If management delivers on their plans, the revenue from these collaborations, joint ventures, and partnerships is expected to materialize from 2027 onward. In my opinion, DRL represents a solid mid-to-long-term investment strategy with relatively low downside risk, barring any major regulatory issues.

Disclaimer : I am invested, so I may be biased.

| Subscribe To Our Free Newsletter |