Reminds me of Warren Buffett quote “A full wallet is like a full bladder; you may have the urge to pee it away”

![]()

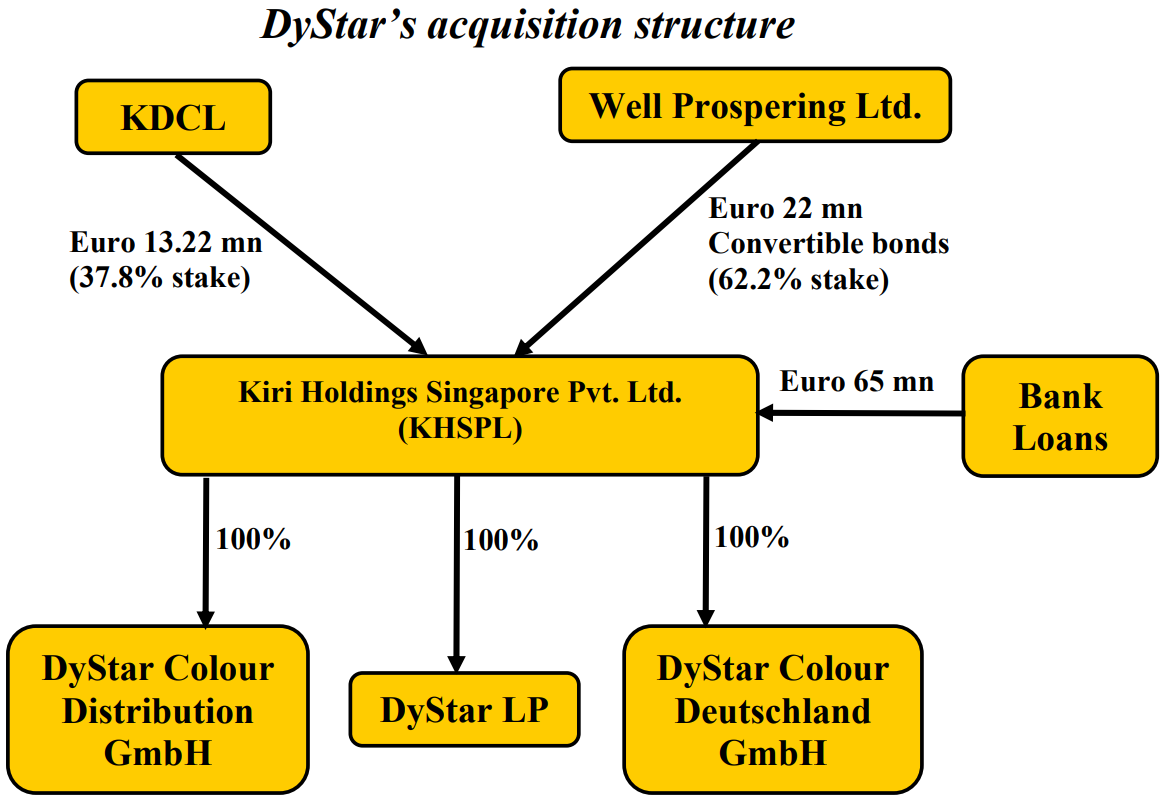

Another fun fact below folks – this is from 2010 showing the Dystar acquisition capital structure – Below structure shows that KDCL (which is Kiri Industries) put Eu 13.22 mn for 37.8% equity stake and allowed Well Prospering Ltd. (which is LongSheng or Senda) to take majority stake 62.2% as Convertible Bonds. This meant that

- Senda had option to convert into equity if things go great (and they did convert into equity and took control and started Minority Oppression on Kiri) and

- if things go south – Kiri takes all downside and Senda with its debt is superior to Kiri’s equity in capital stack. Sends was responsible and covered itself as this acquisition was from bankruptcy proceedings. But Kiri was clearly aggressive. And they still show this aggression in the latest Litigation Financing.

Again it may all work out fine but just highlighting why market is not recognizing the value and that promoter is clearly aggressive so much that in their aggression they take risky steps! The genesis of 10 years of legal case is the wrong structure which Kiri entered into in 2010. So in some way it is their own making.

Market is supreme!!!

Invested small portion of pf.

| Subscribe To Our Free Newsletter |