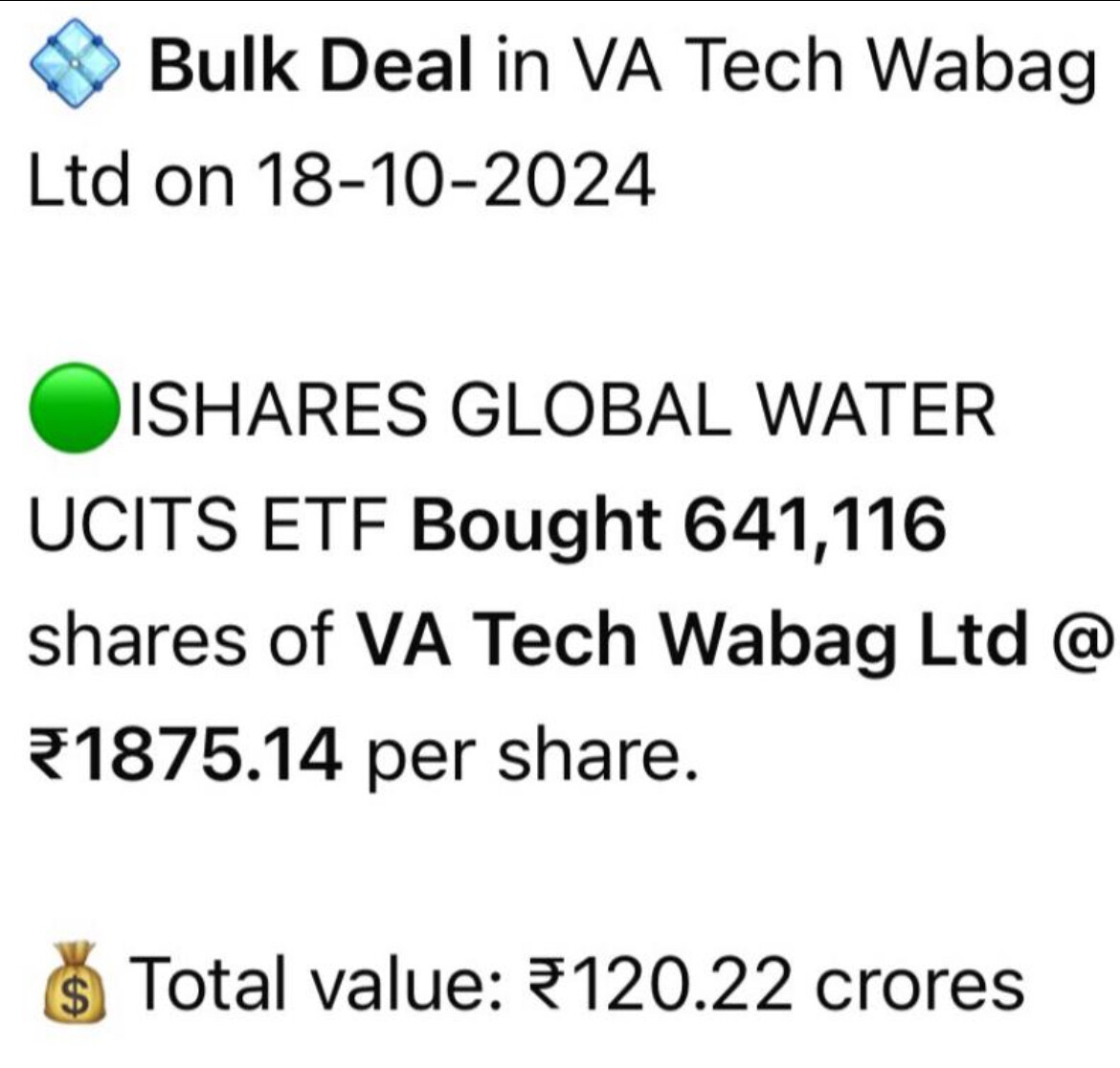

I feel if we take forward earnings of 2026, expecting a PAT of around 300 cr. That values it at 35 times fy26 earnings. I also feel the 15% growth will get re rated to a higher number on actuals. The management is very conservative in my view and may surprise on the positive side. Markets are factoring it now and the move last week was due to fund buying

| Subscribe To Our Free Newsletter |