Results – Q2 FY’25

Some fabulous numbers posted by Par!

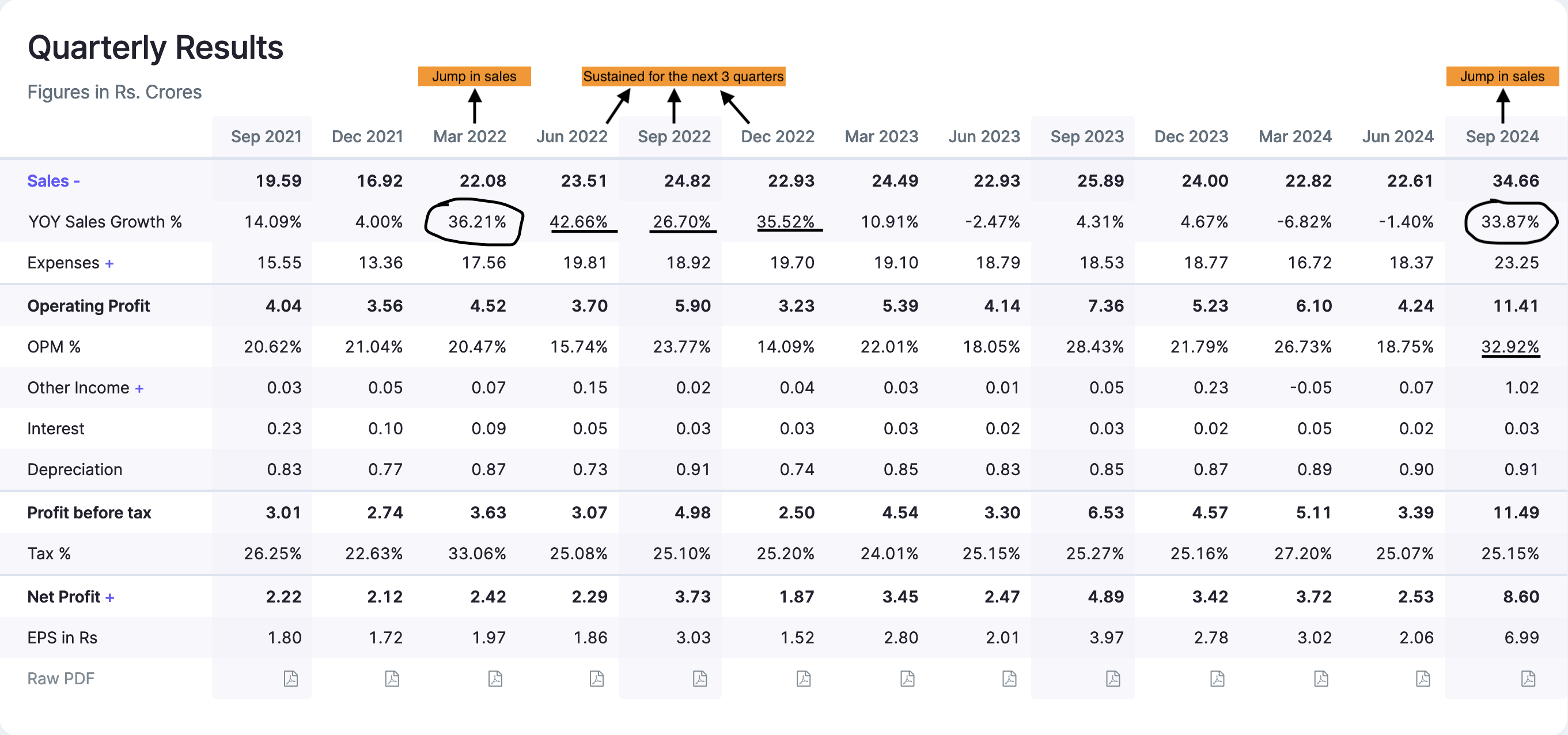

If we take a closer look at the quarterly numbers, we can point at:

- Highest ever OPM at 33%

- Other income of 1Cr

- Is this one-off growth? Well, the last time Par saw a jump in revenue of a similar scale (marked in the diagram below), the revenue was sustained for the next quarters too. Can we assume a few good quarters ahead?

Margins

Highest ever margins, and that is a testament of Par’s focus on constantly improving their product quality and efficiency. In their annual report, they mentioned introducing high-value products that might have helped boost their margins.

Over the past year, we have continued to expand our product portfolio, targeting new application segments and introducing high-value products that resonate with diverse market needs.

Another reason could be that magnesium prices are at a 3 year low!

Par’s API portfolio primarily consists of magnesium salts, and their margins are directly linked to fluctuation in magnesium price. The price of magnesium can be correlated to their margins in the past as well. This was also mentioned by the company in their annual report (you may check my previous post on this thread).

Valuation

Currently on Screener, in Pharmaceuticals – Indian – Bulk Drugs companies, there are only 3 profitable companies (out of 34) with a lower PE than Par (PE-15), and none of them are as financially sound.

Under the radar currently, with markets looking relatively week. Could we see a possible re-rating after these results?

| Subscribe To Our Free Newsletter |