Overall, fair set of topline growth in Q2 FY25, driven by the HPP and CDMO segments. While consolidated profit after tax slightly declined, (lower other income, higher depreciation, tax) the company maintains a positive outlook, backed by a strong order book, ongoing capacity expansion projects, and a strategic focus on key growth drivers.

Posting the summary note from the investor presentation here.

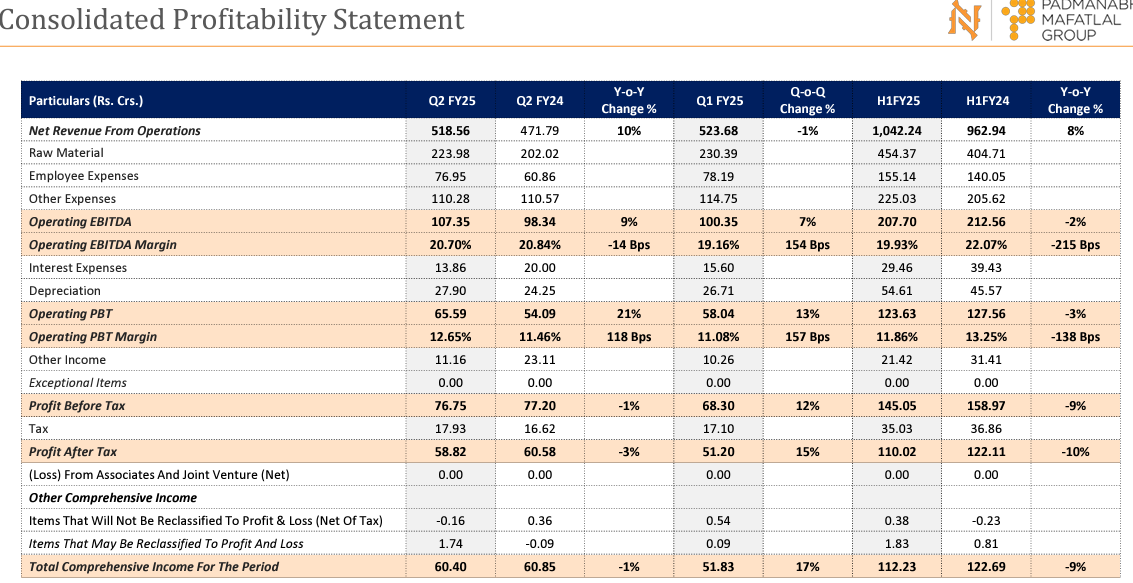

Navin Fluorine International Limited Q2 FY25 Performance Summary

Topline:

- Consolidated revenue from operations for Q2 FY25 was Rs. 518.56 crores, a 10% increase year-over-year (Y-o-Y).

- The Specialty CDMO segment saw a 10% Y-o-Y sales increase, reaching Rs. 518.6 crores.

- The HPP business vertical experienced a 23% Y-o-Y revenue growth, driven by increased R32 sales and better R22 realizations.

- Specialty Chemicals revenue decreased by 15% Y-o-Y due to cautious global demand and competitive pressure.

- The CDMO business vertical saw a 41% Y-o-Y revenue increase, driven by strategic actions including supplying a quantity for process performance qualification for a late-stage study for an EU major customer.5

Bottomline:

- Consolidated profit after tax for Q2 FY25 was Rs. 58.82 crores, representing a 3% decrease Y-o-Y.

- Operating EBITDA for Q2 FY25 was Rs. 107.35 crores, reflecting a 9% increase Y-o-Y.

- Operating EBITDA margin for Q2 FY25 was 20.70%, a decrease of 14 basis points (bps) Y-o-Y.

Other Trends:

- Strong order visibility for the Specialty Chemicals segment is expected for Q3 and Q4 FY25, extending into FY26, supported by the Surat and Dahej assets.

- The CDMO segment holds a strong order book position for H2 FY25.

- Navin Fluorine is making significant investments in capacity expansion projects

- AHF capex for Rs. 450 crore is on track for commissioning by the end of FY25 or early FY26.

- Additional R32 capacity with a capex of Rs. 84 crore is progressing as planned and should be operational by February 2025.

- cGMP4 capex of Rs. 288 crore is underway, with Phase 1 (Rs. 160 crore) expected to be commissioned by the end of Q3 FY26.

- The company maintains a consistent dividend performance history, with a focus on ESG targets.

- Navin Fluorine’s core business strategy emphasizes a high-demand product basket, strong customer partnerships, and being a dependable fluorochemical company.

- The company is focused on driving operational excellence, financial robustness, disciplined execution, revenue stream diversification, partnership strengthening, and the creation of scalable platforms.

Competitive edge stems from factors such as:

- A strong brand reputation, state-of-the-art facilities, and a focus on building scale.

- Backward integration, deep expertise in fluorine chemistry, and a comprehensive approach as an integrated fluorine provider.

- Credible certifications, a competent team, and a commitment to safety and sustainable practices.

- Proximity to logistical options and a long history of expertise in handling complex fluorine chemistries.

Disclaimer: Invested and Biased. Less than 3% of PF. No transactions in the last 30 days. Post purely for study purposes. Consult your advisor before any transactions.

| Subscribe To Our Free Newsletter |