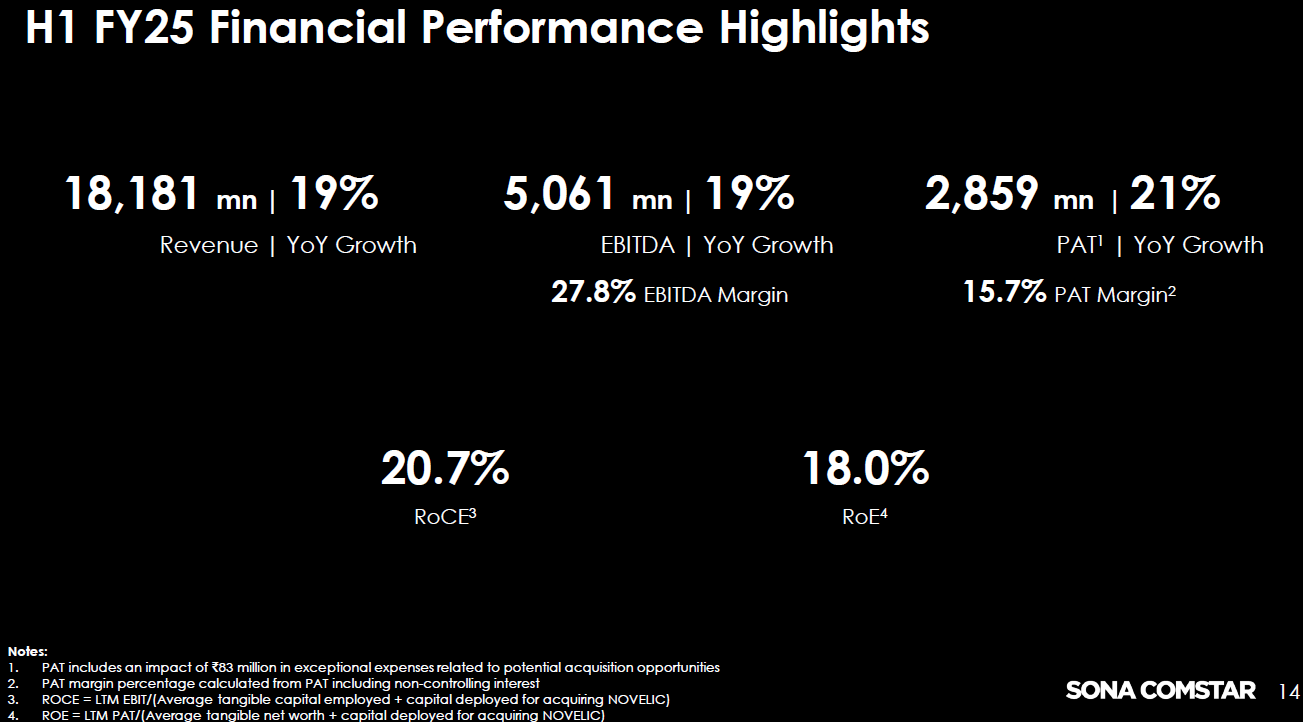

SonaCom posted fair set of numbers in Q2 FY25. Key takeaways from the numbers.

- Total revenue for Q2 FY25 was INR 9,251 million, a 17% increase compared to Q2 FY24

- The light vehicle sales trend in Sonacom’s key markets (North America, India, and Europe) decreased by 2% in the same period.

- BEV revenue in Q2 FY25 was INR 3,172 million, a 53% increase compared to Q2 FY24

- The BEV segment contributes 36% to Sonacom’s total revenue

- Adjusted EBITDA margin for Q2 FY25 was 28.5%, compared to 28.3% in Q2 FY24

- Adjusted PAT margin for Q2 FY25 was 17.1%, compared to 16.3% in Q2 FY24.

- Secured 1 new program in Europe, 1 in Asia, and 14 in India during Q2 FY25

Other highlights/extracts from Inv. Presentation.

Revenue Growth: Total revenue for Q2 FY25 reached INR 9,251 million, reflecting a significant 17% year-on-year increase. This growth outpaced the overall light vehicle sales trend in Sonacom’s key markets (North America, India, and Europe), which experienced a 2% decline. This suggests that Sonacom is effectively capturing market share and expanding its presence.

BEV Revenue Surge: Notably, Sonacom’s Battery Electric Vehicle (BEV) segment witnessed remarkable growth. BEV revenue in Q2 FY25 reached INR 3,172 million, a substantial 53% increase compared to the same period last year. This highlights Sonacom’s successful strategic focus on the rapidly expanding EV market. The BEV segment now contributes a significant 36% to Sonacom’s total revenue, demonstrating its growing importance to the company’s overall performance.

Profitability: Despite various challenges like the UAW strike, Sonacom managed to maintain stable EBITDA margins. The adjusted EBITDA margin for Q2 FY25 was 28.5%, slightly higher than the 28.3% recorded in Q2 FY24. This consistent profitability underscores Sonacom’s operational efficiency and ability to manage costs effectively, even amid a dynamic market environment.

PAT Margin: Sonacom’s adjusted PAT margin for Q2 FY25 was 17.1% compared to 16.3% in Q2 FY24. This growth in PAT margin indicates the company’s ability to translate its topline growth into even stronger bottom-line performance.

New Programs and Customers: Sonacom has secured new programs across various regions in Q2 FY25, demonstrating its continued success in acquiring new business. The company added 1 new program in Europe, 1 in Asia, and 14 in India, further expanding its global reach.

Key Takeaways about Sonacom’s Railway Equipment Division (RED)

-

Market Leader and Pioneer: RED is the market leader in railway brake systems in India. It introduced manufacturing compressed air brake systems for railway applications for the first time in India, making it a pioneer in the industry.

-

Diversified Portfolio: RED possesses a diversified portfolio of products, with brake systems being the largest segment. Other products include couplers, suspension systems, electrical panels, HVAC systems, automatic plug door systems, friction and rubber products, and brake cylinders.

-

Historical Growth and Profitability: RED boasts an attractive financial track record characterized by high growth, profitability, and return metrics. Its revenue grew consistently from FY21 to Q1FY25, with EBIT margins ranging from 13.8% to 20.5% and ROCE exceeding 38% in recent years.

-

High Growth Potential: RED is poised for high growth, driven by the introduction of new products and the overall expansion of the railway sector. The division is strategically positioned to capitalize on the increasing demand for railway equipment in India and potentially other regions.

Summary

Q2 FY25 performance underscores its resilience and strategic positioning within the evolving automotive landscape. The company’s focus on high-growth segments like BEVs, coupled with its operational excellence, positions it well for continued success.

Disclaimer: Invested and Biased. Less than 7% of PF. No transactions in the last 30 days. Post purely for study purposes. Consult your advisor before any transactions.

| Subscribe To Our Free Newsletter |