I think the primary reason is valuation. On 10th October, it was trading at 45 times PE multiple. Now the valuation is is in more reasonable 27-28 times. That is not to say that it cannot fall further. In general FMCG space is falling a bit more than market. Many of the more established players in FMCG market has fallen quite a bit, much more than index. In such a market micro caps stocks do fall more.

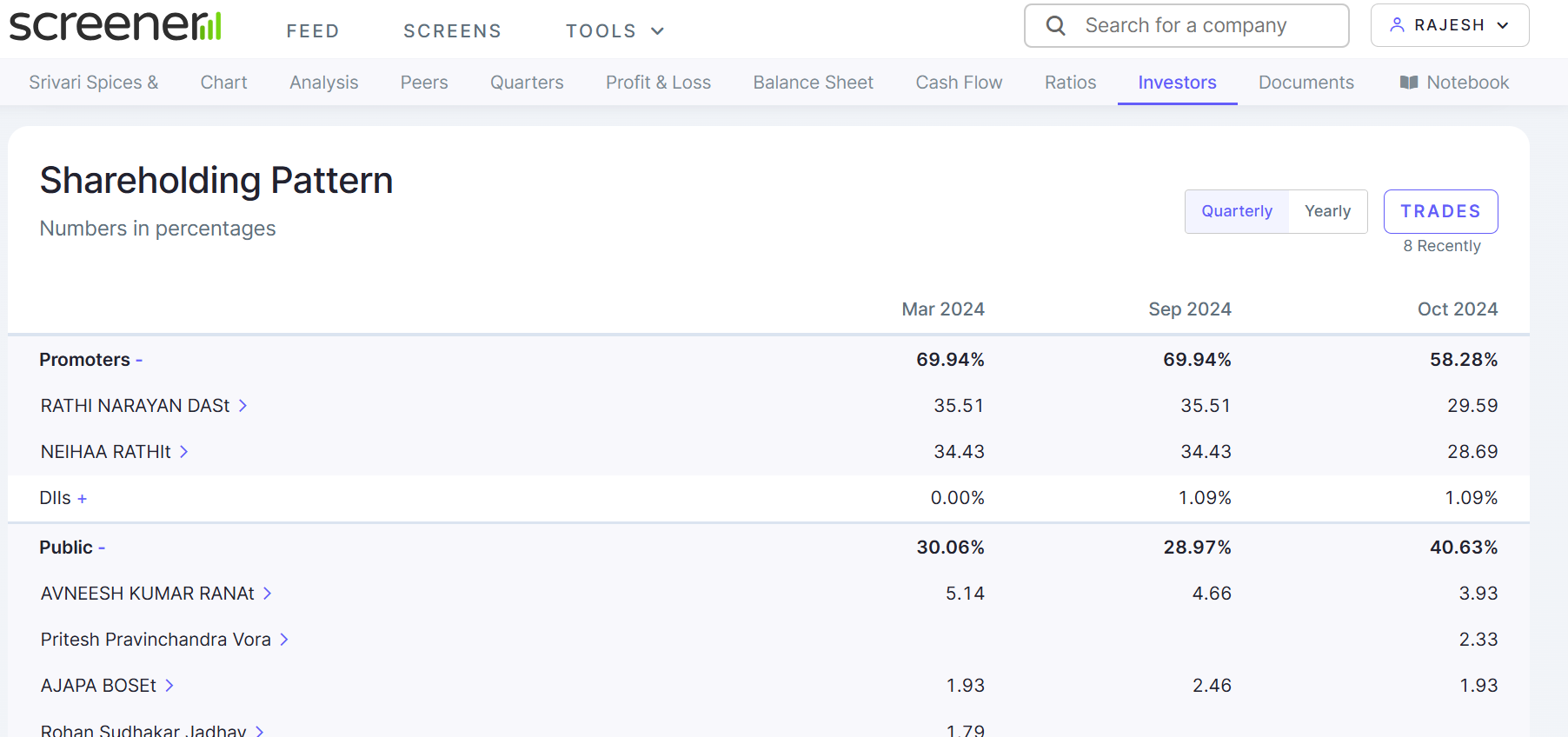

Looking at the company, there is no negative news about the company; however even the positives are missing. There has been no announcements about entry into oil and other products they planned. Further, the shareholding of management has come down in October fling, from 69.94% to 58.28%. Further, shareholding of one Avneesh Rana has gone down.

There is no news of promoters selling anything in market or any notice on exchanges. I think promoters should explain this.

On positive side, the company is expected to do well in H1. Further, the company has received around 25 Crores in rights issue. It should give financial strength to the company to grow at the projected rate. Even the management participated fully in the rights issue at Rs. 175 per share, as declared by management earlier. Thus, things are not looking that bad.

Yes, as an investor we don’t know everything, we cant know everything. Investing is all about taking bets in uncertain future.

| Subscribe To Our Free Newsletter |