• Sales growth in Q1FY25 was lower as the company prioritized high EBITDA margin projects. We believe the rest of FY25 will have a higher growth rate with margins greater than that of FY24.

• The slowing order book presents a concern; however, we anticipate growth to resume once the U.S. capacity is operational. Additionally, the domestic business—spanning both utilities and franchisees—has shorter execution cycles, which we will be able to monitor more closely post-listing.

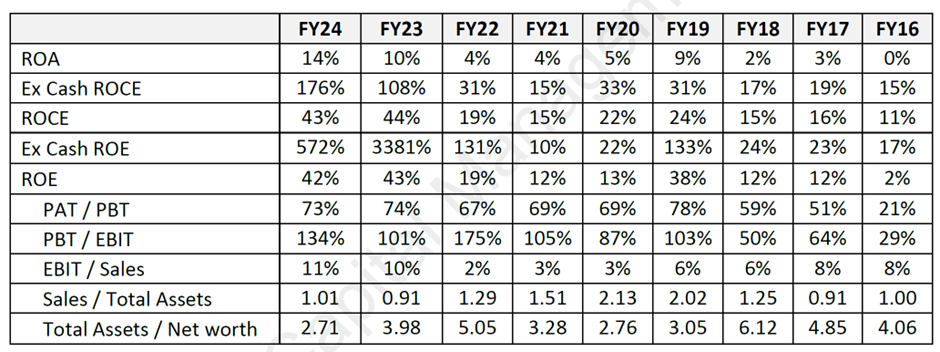

Healthy Profitability –

Buoyed by margins, return ratios were strong in FY24. Before FY23, the ROE ranged from 2% to 38%. The trend of healthy return ratios is anticipated to persist, driven by sustained robust margins and higher asset turnover resulting from improved capacity utilization.

ROCE of 9.45% in Q1FY25 is not annualized number, hence can not be compared with ROCE of full year.

| Subscribe To Our Free Newsletter |