Answer

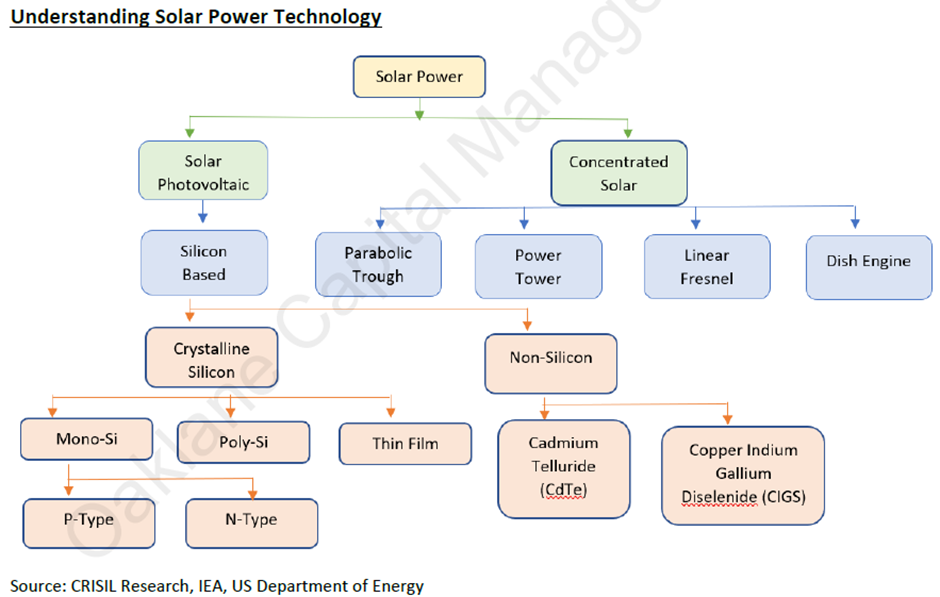

Before delving into solar PV basics, it is crucial to note two primary solar power manufacturing technologies: Photovoltaics (PV) and Concentrated Solar Power (CSP). PV, being more cost-effective, is the prevailing choice for solar power generation.

• Solar PV technology bifurcates into two primary categories based on the primary raw material: crystalline silicon-based and non-silicon-based. The predominant share, exceeding 95% of global capacity, is held by crystalline silicon, with First Solar being the only large contributor in the non-silicon-based module sector.

• Within the crystalline silicon domain, the developmental trajectory has transitioned from polysilicon to multi-crystalline and presently to mono crystalline. Mono-crystalline, particularly in N-type cells, is gaining traction due to enhanced efficiency, especially on a smaller scale, superior performance in lower light conditions, and a higher Internal Rate of Return (IRR).

• CdTe (cadmium telluride) ranks as the second-most prevalent PV material post-silicon and finds application in thin film PVs. Another material, copper indium gallium diselenide (CIGS), is utilized in the same context. Despite their cost-effectiveness, these alternatives do not parallel the efficiencies achieved by silicon cells.

• Another material which Is gaining prominence is Perovskite which is also used in thin film cells. Though the efficiencies have matched silicon-based cells in labs, it is yet to become commercially viable for large scale usage.

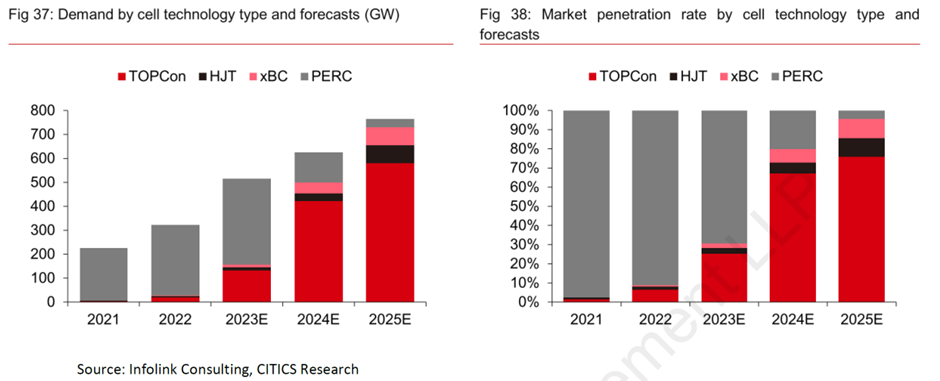

Within crystalline silicon N-type technology continues to upgrade, with opportunities in cost cuts and efficiency gains- TOPCon may swiftly become a mainstream technology in the industry, the industrialization of HJT will likely accelerate and xBC is poised for a breakthrough in the higher-end market segment.

Technology cycle

-

Historically, a new technology has come every 3 years and companies have had to tweak their plant & machinery accordingly. In 2022, with super normal profits for Chinese companies, this technology cycle was faster, and they moved swiftly from Mono PERC to TOPCon.

-

Currently, CLSA believes solar technology innovation is progressing slower than anticipated due to reduced willingness to invest in solar capital expenditures during the sector’s down-cycle. Among the key technology introductions for 2024, only laser-enhanced contact optimization (LECO) is on track, while the adoption of 0 bus bar (0BB) and HJT technologies may proceed more slowly than expected. This situation could benefit Indian players, as capex planned around a three-year technology cycle may be extended by one to two years.

-

Chinese companies are the technology leaders along with First Solar for Thin Film, currently Indian companies have been doing tech tie-ups to get latest technologies. Research institutes in India are focusing on developing new technologies, however this may take its time. Waaree Energies has collaborated with IIT Bombay for R&D.

-

Transition from Mono PERC (P type) to TOPCon (N type) is at solar cell level, which can be done with an incremental capex of 100-150 cr. At solar module level there are no changes in the manufacturing process.

| Subscribe To Our Free Newsletter |