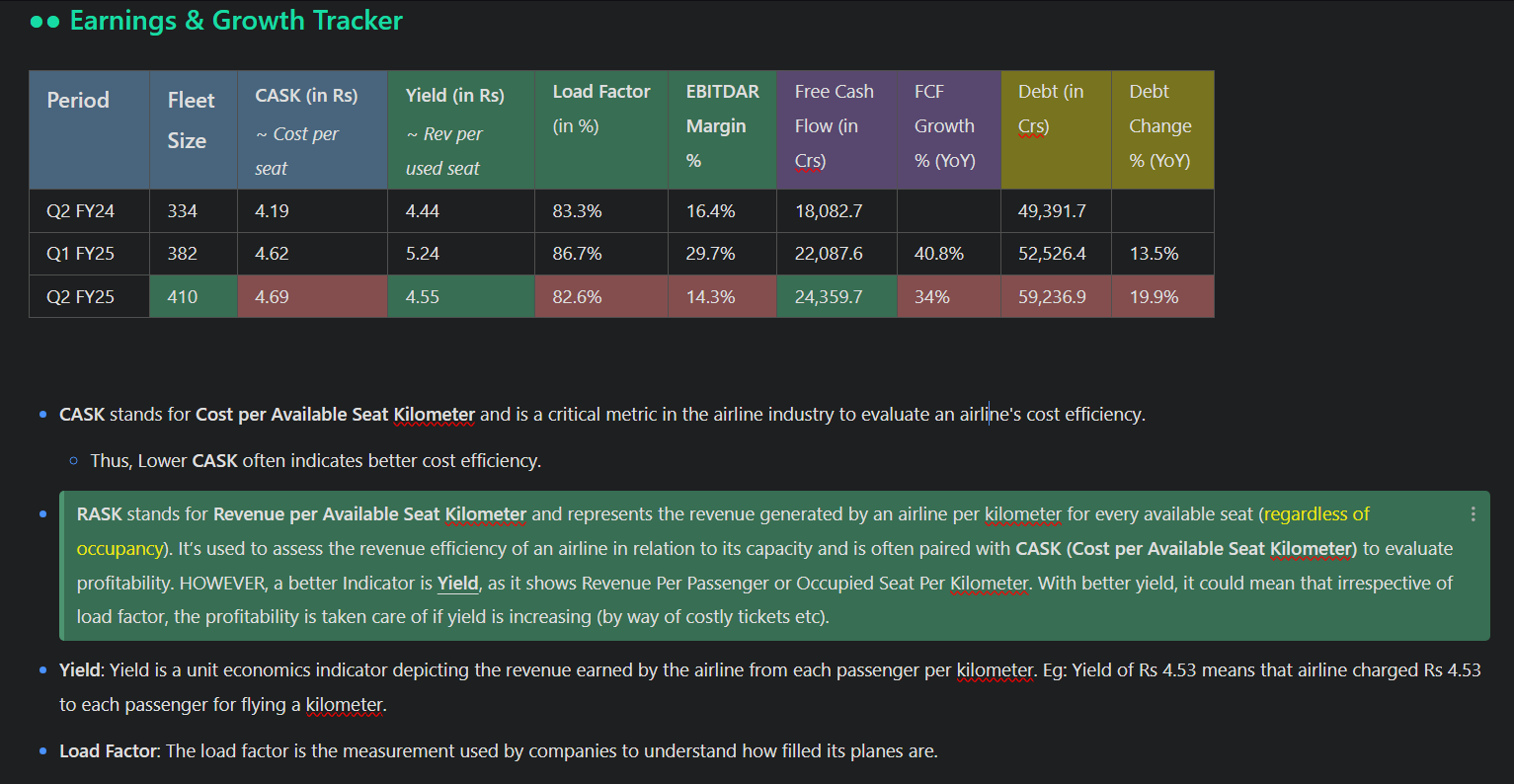

Results are saddening. I put up a table to analyse if there are some green sides I might be missing. Here it is:

Analysis:

- Its Yield has decreased, revenue per passenger…

- Its Load factor has decreased, the occupancy of flight. More Vacant seats.

- Debt has increased and the pace of debt increment has also increased.

- Cost and Expenses have increased.

Not much of an exciting results. Only good things I could find were:

- Free cash flow has improved, working capital seems to be not constrained.

- Fleet size has expanded, potential of more revenue stream.

Some inferences I could make are:

- The pricing power of Indigo seems to be losing. A quick search of flights between metro cities will show you that Air India’s low cost variant – Air India Express has better pricing than Indigo in many cases, and where it doesnt have, it is just shy of one-two hundred.

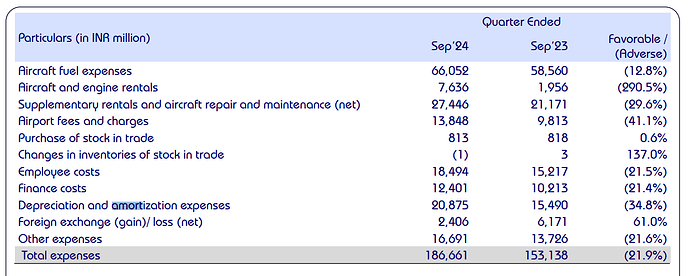

- The Depreciation-Amortization cost had increased this time, may be a one-time high increment as new aircrafts join the fleet. (2k from 1.5K Cr)

- Aircraft related costs were also high as seen below

Overall, a setback results. Perhaps, next quarter may bring back the profitability given the festival seasons and launch of business class adding to top line.

However, yield, load factor, and debt would be very crucial factors to follow.

Discl: Remain invested. Above words not to be construed as any advice.

| Subscribe To Our Free Newsletter |