Q2 Fy25 Results

great set of no.s (driven by fertilizers, crop nutrition segment)

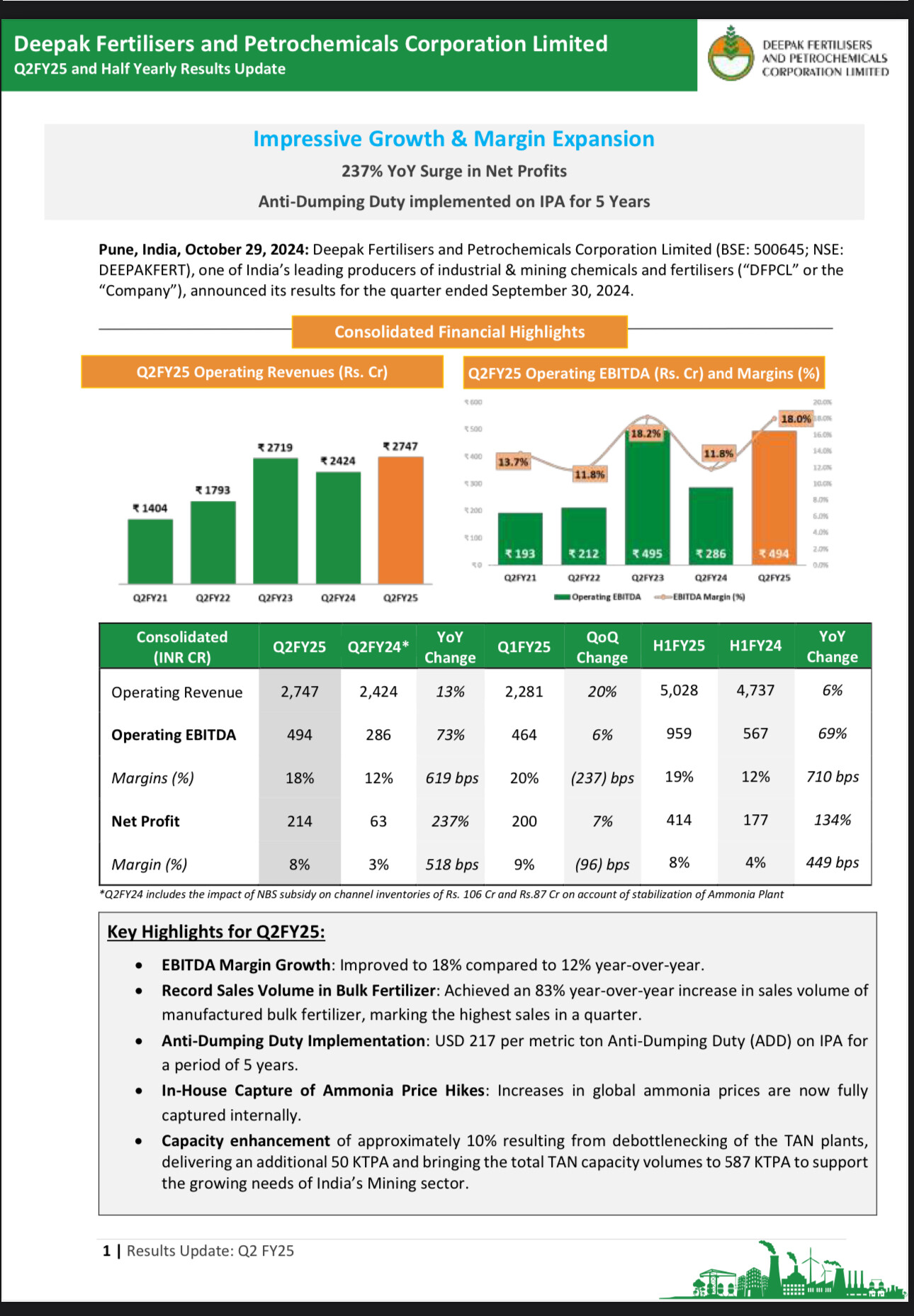

YoY revenue – 2,747cr Vs 2,424 cr ![]() 13%

13%

YoY PBT – 298 cr Vs 116 cr ![]() 156%

156%

YoY PAT – 214 cr Vs 63 cr ![]() 237%

237%

YoY EPS – 16.64 vs 4.76 ![]() 249.58%

249.58%

QoQ revenue – 2,747 cr Vs 2,281 cr ![]() 20%

20%

QoQ PBT – 298 cr Vs 269 cr ![]() 10.7%

10.7%

QoQ PAT – 214 cr Vs 200 cr ![]() 7%

7%

QoQ EPS – 16.64 vs 15.49 ![]() 7.42%

7.42%

• Debt Reduction: Prepaid ₹200 crores in debt, improving the Net Debt to EBITDA ratio from 2.66x to 1.64x.

• Change in key RM Prices in Q2FY25: Ammonia ~11% YoY; MOP ▼ ~40% YoY; Gas ~9% YoY

• Mining Chemicals (Technical Ammonium Nitrate):

• In Q2 FY25, premium product LDAN’s sales volume soared by 16% YoY and rose by an impressive 20% in H1 FY25 compared to H1 FY24

• Business Outlook: The mining and infrastructure is expected to pick up post monsoon as demand for Power (Coal), Cement & Steel is expected to increase thereby providing robust support for TAN demand.

Disc invested

| Subscribe To Our Free Newsletter |