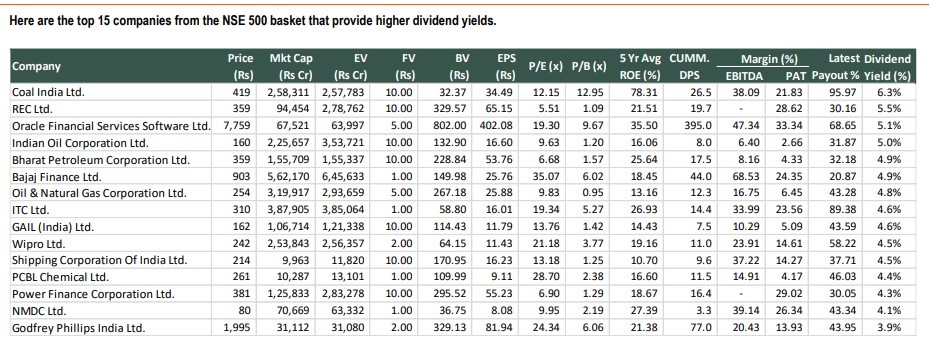

top 15 companies that provide higher dividend yields Post navigation Previous Previous post: Top 15 companies from the NSE 500 basket that provide higher dividend yields of up to 6.3% by IDBI Capital Leave a Reply Cancel replyYour email address will not be published. Required fields are marked *Comment * Name * Email * Website Current ye@r * Leave this field empty