Company has uploaded the earnings call transcript today. Few notable points from there:

- Margin and EBITDA guidance

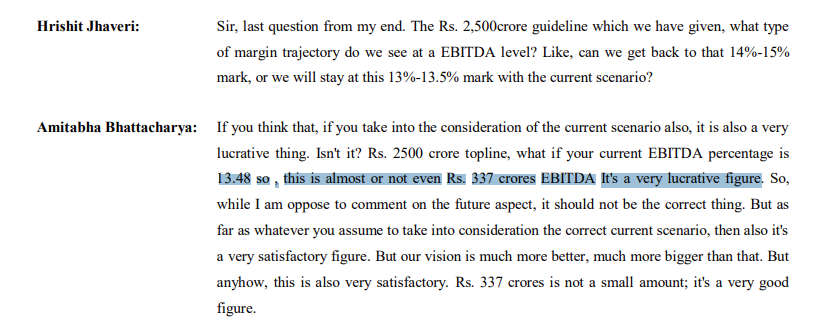

CFO is hinting towards margins to be closer to 13.5% in FY26 and hence EBITDA potential of 337 crores in FY26

(At the same time highlighting that “But our vision is much more better, much more bigger than that”)

So maybe 13.5% is a conservative guidance on margins for FY26?

- EPS guidance assuming dilution of due to potential ~700 crore fund raise.

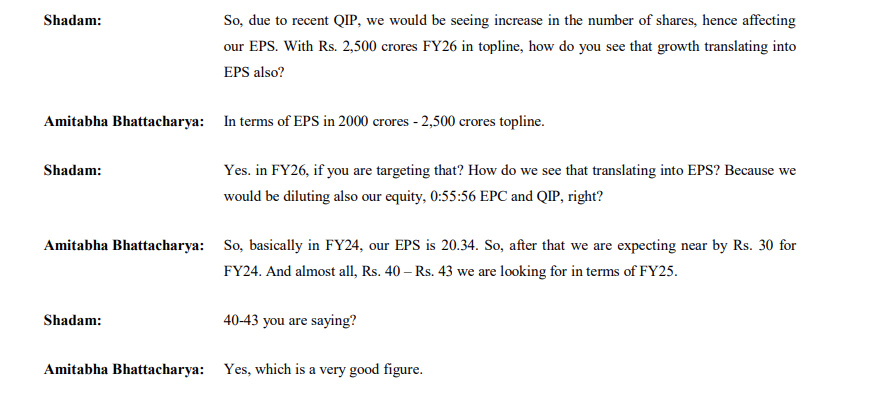

- EPS expected for FY25 = ~30

- EPS expected for FY26 = ~40-43 | This assumes dilution of a certain % at a certain stock price.

We need to do some math on back calculating the implied dilution % in-built in this EPS of 40-43

-

a) No dilution scenario:

- 337 crore of FY26 EBITDA mentioned by CFO above

- 50 crores of depreciation

- 40 crores of interest cost

- = expected PBT of 247 crores.

- Assume a 27% tax rate

- and this gives us 180 crores of PAT.

- 3.1 crores total shares outstanding gives an approximate FY26 EPS of ~58

-

b) Dilution Scenario

If we apply an EPS of 41.5 (mid-point of dilution scenario), on 180 crores of PAT, this assumes total shares outstanding of 4.33 crores which means ~40% dilution on share count basisCurrent Market Cap is ~1800 crores and 40% dilution means a fund raise of 1800*0.4 = 720 crores. So, basically the 40-43 EPS for dilution scenario assumes (1) QIP happens at CMP and (2) the entire 700 cr is raised and (3) No interest cost savings by debt paydown from QIP money (4) No incremental revenue or profits from incremental fund raise.

PS: There seems to be a typo in the transcript. it should read Rs. 30 for FY25 (instead of FY24).

What do others think of this calculation? Please point out any mistakes that you see.

| Subscribe To Our Free Newsletter |