Thanks for the detailed thread @nirvana_laha .

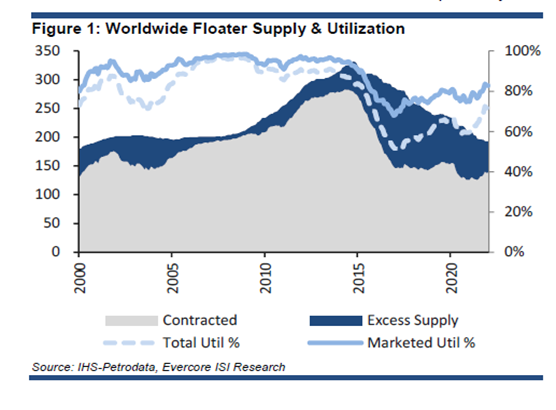

I have done some work on the largest offshore drilling operator (Transocean) which operates Ultra Deepwater floaters (UDW) and semi-subs. I agree the supply side of the market in offshore drilling has tightened with almost no new drillships being ordered in last 8 years.

-

Do you have a view on longevity of the cycle for jackups? In UDWs, the last cycle lasted for almost 10 years with utilization being above 90% which peaked in 2014 for reasons you have already mentioned above. It is important to see how long can these elevated earnings last.

-

Do you know how the current day-rates stack up vs the last upcycle? In UDWs, day-rates had touched $600k/day for high spec rigs in 2014. However, in the current cycle, we are seeing day-rates just levelling at those levels and no higher for contracts which are being signed for 2026-27. I would have expected day rates to be at-least 20-30% higher if we just adjust for inflation and also keeping in mind that the current fleet of rigs is much higher spec (8th gen now vs 6/7th gen in last cycle). Do you see significant upside in day-rates in jackups from where they currently stand because the cash flows will look very different then.

-

How does the current orderbook in jackups look like and where do day-rates have to be to incentivize new-builds? I’m looking at the current day-rates of average 80k and if I assume 40% EBITDA margin, that would be (80k * 365 *0.4) $13mm of annual EBITDA for a jackup which costs $200mm, i.e. 6.5% annualized returns which are below cost of capital. So my preliminary understanding is for rates to be much higher with a higher visibility on contract duration to incentivize any newbuilds. So either supply will remain constrained or day-rates increase materially which should both be positive for Jindal Drilling.

I also see that the operating margins have gotten materially impacted year on year despite increase in revenue which seems odd given the operating leverage.

| Subscribe To Our Free Newsletter |