I don’t have a view beyond the commentary of global jack-up operators. What is clear and should have a bearing on the cycle, is that new supply is almost non existent.

And as you rightly pointed out, even at current day rates, justifying ordering a new jack-up rig is not sensible because return on capital is well below cost. Newbuild jack-up rig quotes range from 200mn-300mn USD depending on specifications and at 90k USD/day jack-up rates and even assuming aggressive EBITDA margins of 50%, the return on capital employed ranges between 5.5%-8.5%, significantly below any reasonable estimate of cost of capital.

This is why you see offshore asset managers like Valaris talking about returning cash to shareholders rather than deploying them on new assets. This is why the orderbook to fleet ratio is as low as it is and thinking logically, this supply crunch should continue for the foreseeable future. Also time to build a new rig ranges between 2-3 years, so even if new orders come in, for the rig to add to fleet supply, there will be a delay of 2-3 years.

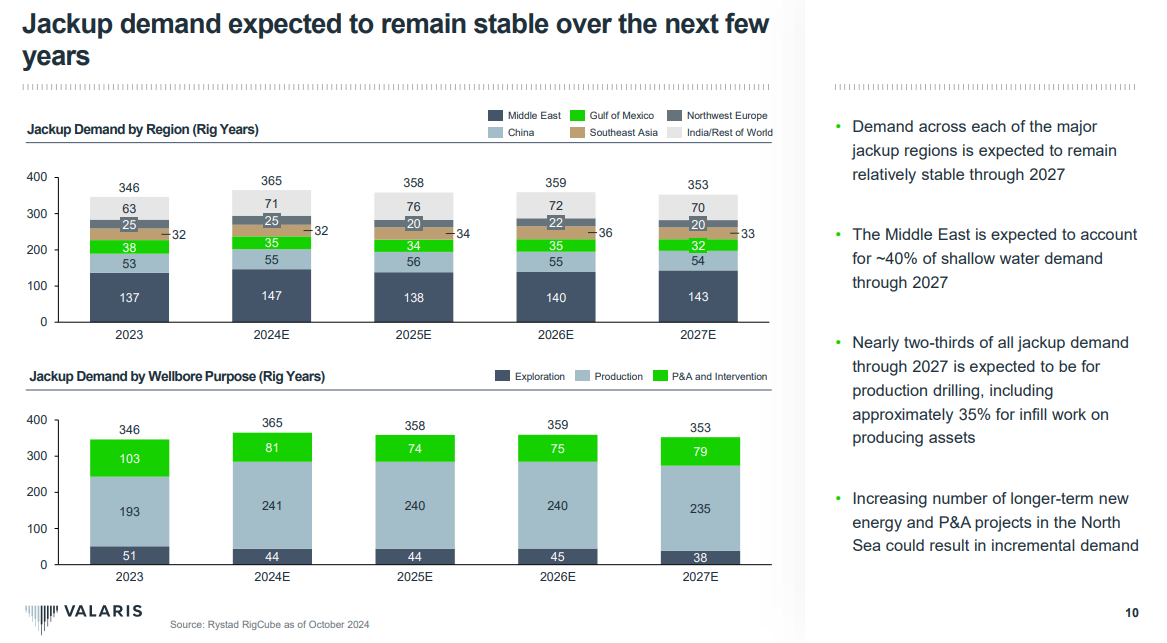

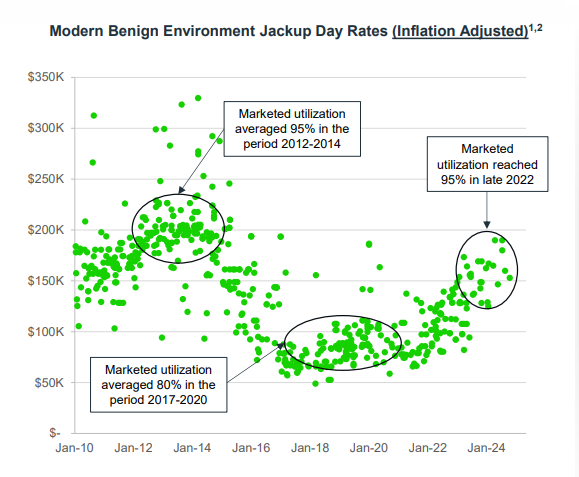

Some data on current jackup outlook, utilisation and day rates from Valaris’s Q3 PPT and Shelf Drilling’s Q2 PPT.

So the global cycle looks robust judged in terms of the supply side. The jack in the box is of course global demand which nobody can predict. But as long as oil prices are above 60$/barrel, industry research seems to suggest that there will be no significant cutdown in offshore drilling volumes by E&P companies.

Some near term risks specific to Jindal Drilling which should be closely tracked

- Further suspension of rigs by Saudi Aramco can sour the mood for the entire jackup market (27 rigs dehired by them so far in CY24)

- ONGC has been trying hard to bring down day rates for their contracts as seen by them playing hardball by cancelling/postponing two tenders for 7 jackups in June and Sep. How that resolves will be critical for Jindal Drilling in the medium term. In the near term (8-12 Qs) it may not matter as much because the three rigs coming off contract in CY25 and CY26 all have present operating day rates in the range of 38k-48k/day and any new contracts in CY25 and CY26 should be at higher prices as things stand.

| Subscribe To Our Free Newsletter |