Commentary from Q2FY25 Earnings Call of Coforge, the Promoters of Cigniti.

Link: https://www.coforge.com/hubfs/Transcript-of-Earnings-Conference-Call-Q2-FY25pdf.pdf

- Growth

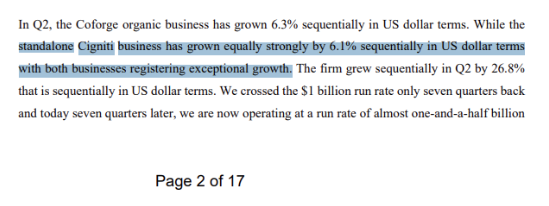

- Cigniti grew 6.1% QoQ

- This is very strong across growth across all IT companies

- Last 5-year revenue CAGR of Cigniti is 17% (Source:screener)

- We can assume that Cigniti can grow at 10% going forward, conservatively

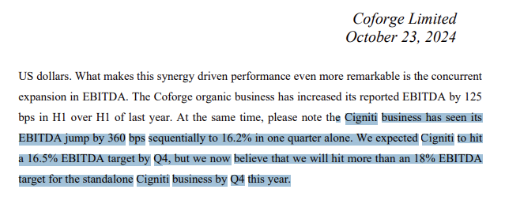

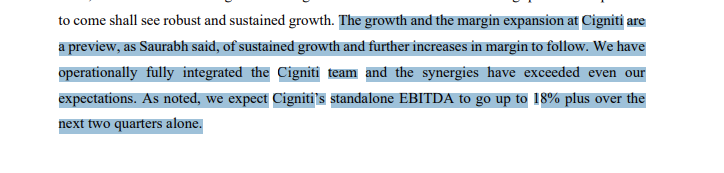

- Big turnaround in Profitability : Cigniti EBITDA margins are expected to go to 18% by Q4FY25

- Cigniti had 12% margins in FY24.

- It is a fair assumption that Cigniti will have 18% EBITDA margins in FY26,

- This margin expansion from 12% to 18% can lead to 50% increase in EBITDA

- Valuation

- Good RoE of 27% over last three years

- If we very conservatively assume 10% revenue growth in FY25 and FY26, FY26 revenue can be 2,200 crores. Management is very positive on revenue growth outlook of Cigniti.

- With 18% EBITDA margin on 2,200 crore, it can mean ~400 crores of EBITDA in FY26

- Cigniti is net cash company with cash of ~400 crores

- Market Cap is 3,800 crores

- EV = 3800 – 400 = 3,200 crores

- EV/EBITDA for FY26 = 3200/400 = ~8x

| Subscribe To Our Free Newsletter |