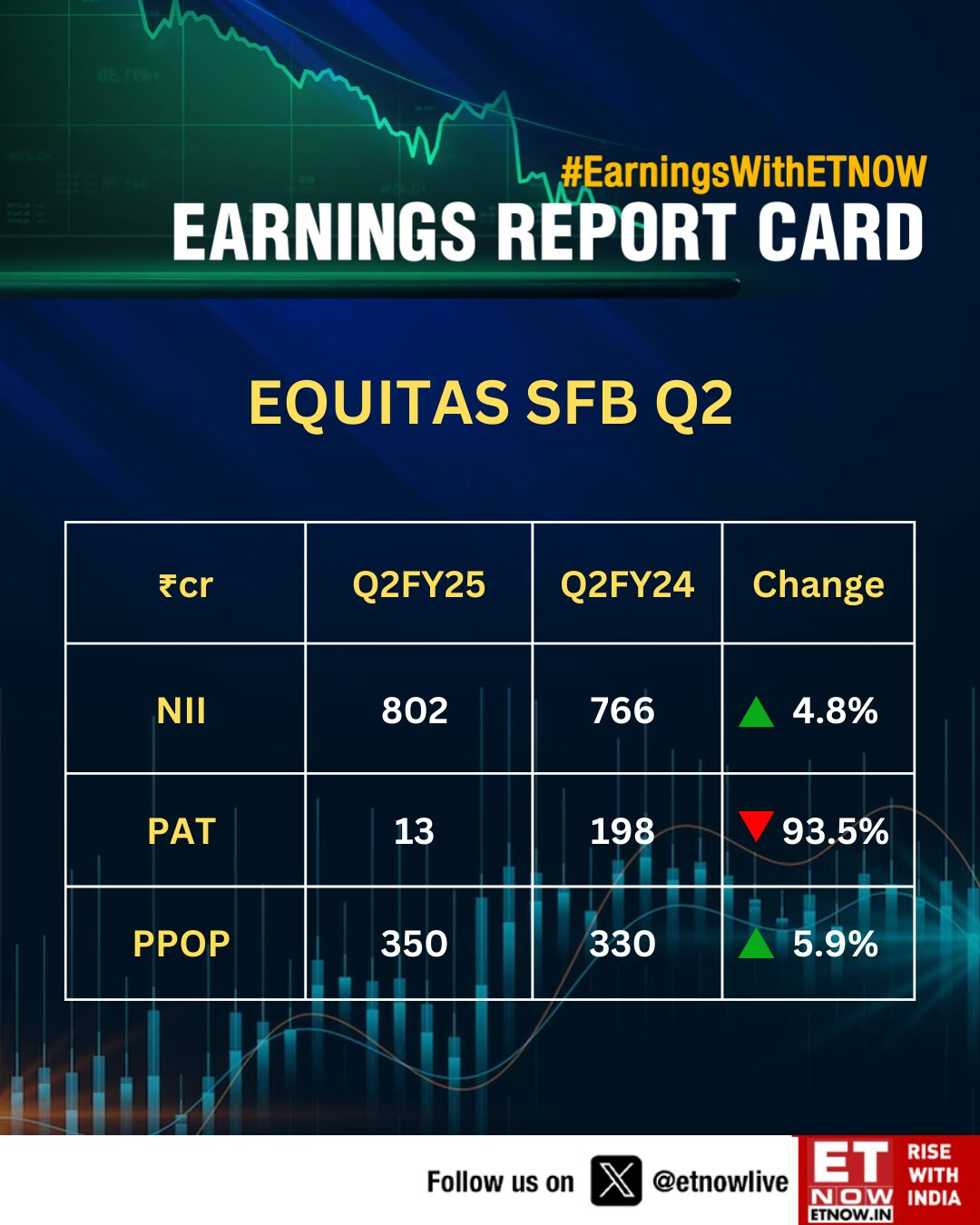

Equitas Small Finance Bank’s Q2 financial performance showed mixed results, with a sharp decline in net profit but solid growth in interest earned year-over-year.

Key Points from Q2 Results:

- Net Profit: The bank’s net profit fell drastically to ₹13 crores, a ~93.4% year-over-year (YoY) decline from ₹198 crores. This sharp drop was well below the market’s estimate of around ₹158 crores and was largely impacted by an increase in provisioning for potential loan defaults.

- Interest Earned: On a positive note, the bank saw a YoY growth of ~14.7% in interest earned, reaching ₹156 crores, up from ₹136 crores in the previous year. This increase suggests a growing loan book or higher interest rates that boosted the interest income.

- Asset Quality: The bank’s asset quality weakened, with Gross Non-Performing Assets (GNPA) rising to 2.95% from 2.73% quarter-over-quarter (QoQ), and Net Non-Performing Assets (NNPA) increasing to 0.97% from 0.83%. The rise in NPA levels signals a deterioration in loan quality, possibly due to macroeconomic challenges affecting borrowers’ ability to repay.

- Provisions: Equitas increased its provisions for potential loan losses to ₹33 crores, up from ₹30 crores in the previous quarter. This conservative approach to provisions may be in response to the rise in NPAs, which often indicate higher risk in the loan portfolio.

The decline in net profit despite an increase in interest income reflects the pressure from rising NPAs and higher provisioning costs. The positive growth in interest earned shows that the bank’s core lending business is growing, but the increase in provisions and deterioration in asset quality suggest challenges in maintaining profitability amidst economic uncertainties. Equitas’s conservative provisioning could help safeguard against future risks, but it will be important for the bank to improve asset quality to stabilize earnings.

This Q2 performance may also affect investor sentiment, given the gap between actual and estimated net profit, and the rising NPA levels are likely to remain a key area of focus in the coming quarters.

| Subscribe To Our Free Newsletter |