@SwapanBansal , thanks for your detailed analysis earlier. You have been quite passionate and very much consistent in providing the business level update for this scrip. Also thank everyone else for adding the details.

I have a few points that i want to mention here.

- @SwapanBansal : your analysis mention earlier as the below exhibit. Does this mean that the industry installed capacity is more than market size? I am sorry if this sound stupid question but do we have any view of estimate market size in India? ALso i see that other players are also doing capex to increase capacity what is the scenario here? I think it is important to understand this in order to be able to completely understand the 2x growth they are planning to achieve, though i do not deny their growth story.

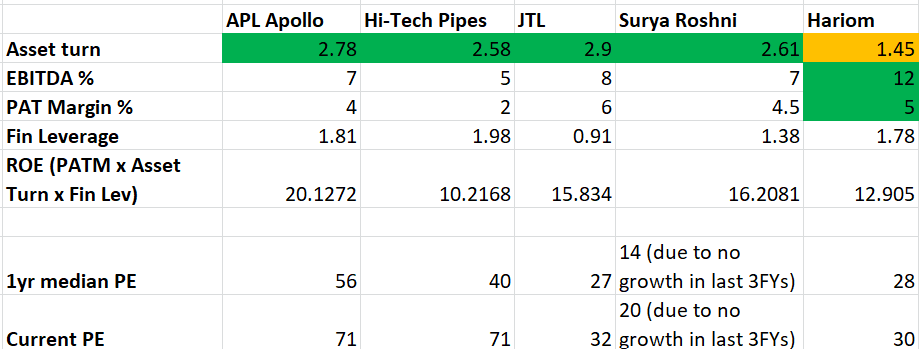

- I have observed that the ROE for Hariom is just matching the other players (if not below), and main reason i can see is the asset turns for Hariom is significantly lower. All other competitors operate at >2.5x of asset turns while Hariom is <1.5. WHat is the reason for this? I can understand that this may be partially because they produce VAP as opposed to the commodity. But this may not be the sole reason behind the significantly lower asset turn. If they can achieve the same asset turns as the peers, this can be a very big game changer given that they are already working to improve PAT margin by reduction of debt. Currently they are just able to match the ROE in fact it is lower than peers) as the peers because of a little higher PAT. This is also one reason they have lower PE than peers i believe.

| Subscribe To Our Free Newsletter |