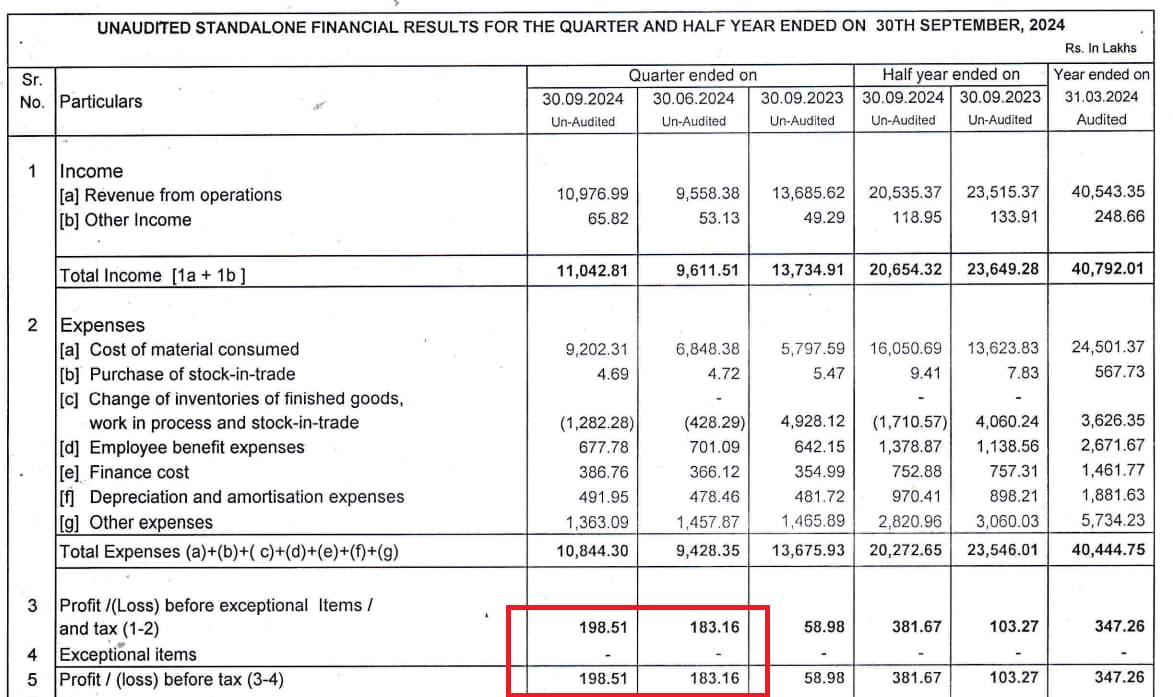

Results do seem underwhelming and probably driven by the underperformance in B2B segment. As per the investor presentation, B2C is not part of standalone financials. As per the results, standalone profitability has hardly budged from Q1Fy25 nos – INR 198 lakhs PBT in Q2FY25 vs INR 183 lakhs in Q1FY25. Probably couldn’t renew contracts / get hikes from large institutional buyers. Even presentation emphasizes primarily on RM cost reduction as profitability driver. Additionally, couldn’t come across if their plant is US FDA approved, something that players like OAL and Privi emphasis upon, wherein they manage some premium for quality.

| Subscribe To Our Free Newsletter |