Q2 FY 2025 CONCALL HIGHILGHTS

Yatharth attracting leading doctors across NCR.

Deloitte is appointed as internal auditor.

Rise in employee cost due to new therapeutic areas, new doctors joining. Margins will be sustainable (25 to 26% at group level) with two more additional new hospitals. Mature Hospital margins is 28 to 29%.

Dropping occupancy in Noida hospitals due to reduction on government business. It is reduced by 1 to 2%. IPD volume increase. Focus on increasing cash and insurance segment. It will have positive impact in coming quarters.

EBIDTA loss in Faridabad Hospital, started in Q2 FY2025 is 28% Negative and reducing.

Planned CAPEX is from Internal accruals, 60 to 70 L per bed for expansion of beds in existing hospitals.

Decline in Jhansi ARPOB due to reduction in cash payments. Government panel drags in margin. It will be 15000 to 20000.

Max Hospital opened near Yatharth Hospital will build ecosystem in Noida, should benefit every operator. Continuous improving standards.

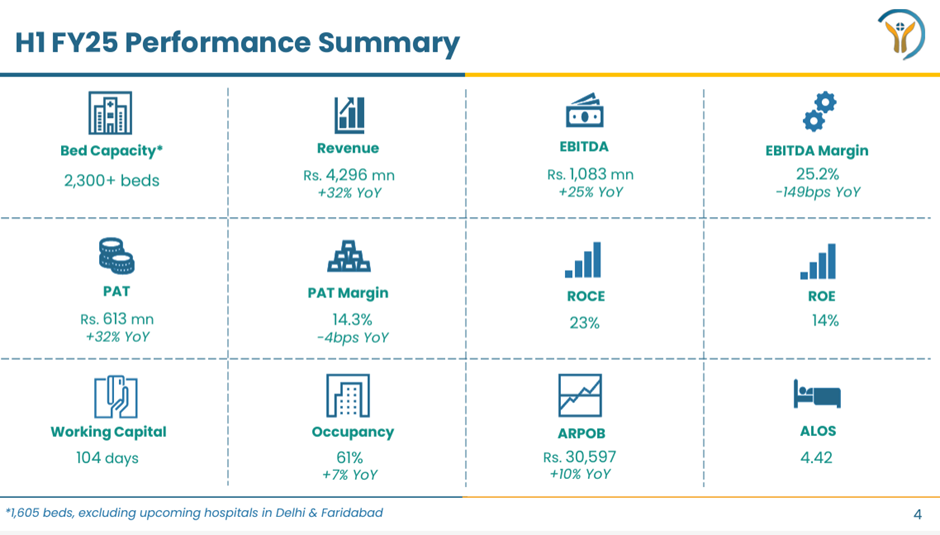

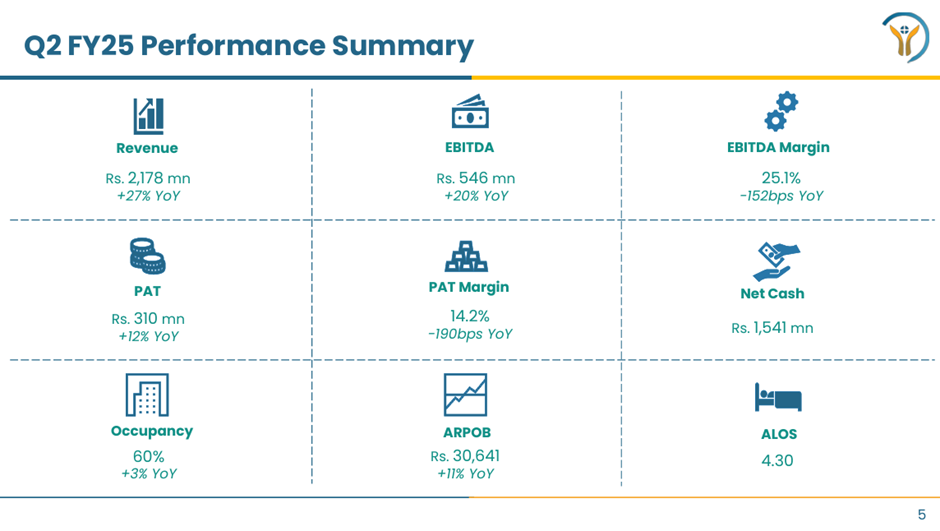

No difference between Q1 and Q2 Revenues due to no breakout of flu in areas of operation for Yatharth. Government business is reduced as per strategy by company.

Government business is reduced by 4% Q to Q, 6% H1 to H1. Target is to reduced government business to 25% in 3 years.

To fill available capacity government business is taken.

Expect Q3 and Q4 will be higher. Expect near to 1000cr. Revenue.

New Hospital in Model Town:

160cr. Will be paid to Union Bank. 25% paid by company’s book.

Additional 60 to 70 cr. For improving infrastructure and medical equipment. With this It will be 300 beds.

ARPOB in this hospital will be more than Noida hospital, will be super specialty in day one. It can be close to 40000 ARPOB easily achievable.

Existing capacity is 150 to 170 beds.

Hospital currently non-operational. It was operated by family of doctors. Face financial issue and bank take over. It was acquired by online auction.

Land, structure belong to Yatharth. No Rent.

Pay back period will be 3 to 3.5 years.

New Hospital in Faridabad:

Keep on investing on 60/40 % basis.

Minority shareholder is family from MGA. They do not operate any other hospital. One of the son is cardiologist.

Additional 90 cr will be spend to complete structure and medical equipment including Radiology.

Land, structure belong to Yatharth. No Rent.

Reason of adding one more hospital in Faridabad as they will be 15 to 20 km distance. Model of big player in city, which gives benefit of brand position, star doctors can be shared between two hospitals. Doctors wants to join as head of department as capacity will be 600 beds. Near to Airports and have great drainage of population and have massive expansion.

Expected ARPOB in this hospital can be 38000 Rs. Can be with start of and can go beyond.

Conclusion:

Revenue can continue grow with sustainable margin of 25 to 26%.

Have more debt, dilution in equity as company continue to acquire more hospitals.

Valuation is attractive compared to peers.

Room for improvement in ARPOB compared to peers.

Disclosure: Invested, may exit anytime. Reviewing.

| Subscribe To Our Free Newsletter |