So what I think is & tried to researcher deeper & found out:

- The report from where I took data is of Equirus initiative coverage report on APL Apollo tubes… I tried to go to many companies related to steel tubes company PPT & initiative coverage, but can’t able to verify the data about installed capacity higher than market size (might be it was just estimates & reality would be different as all companies have different estimates)

But I can verify data about ERW Pipes segment (where hariom has main focus)

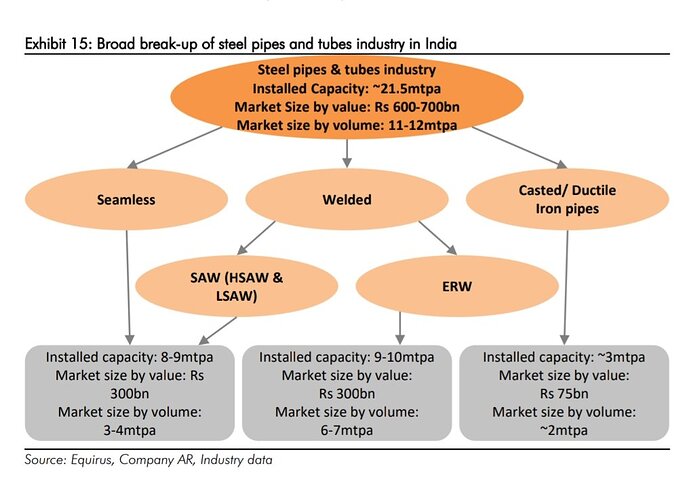

So, this was the original image… ERW Pipes has 9-10 mtpa installed capacity & 6-7 mtpa size… so this is somehow correct

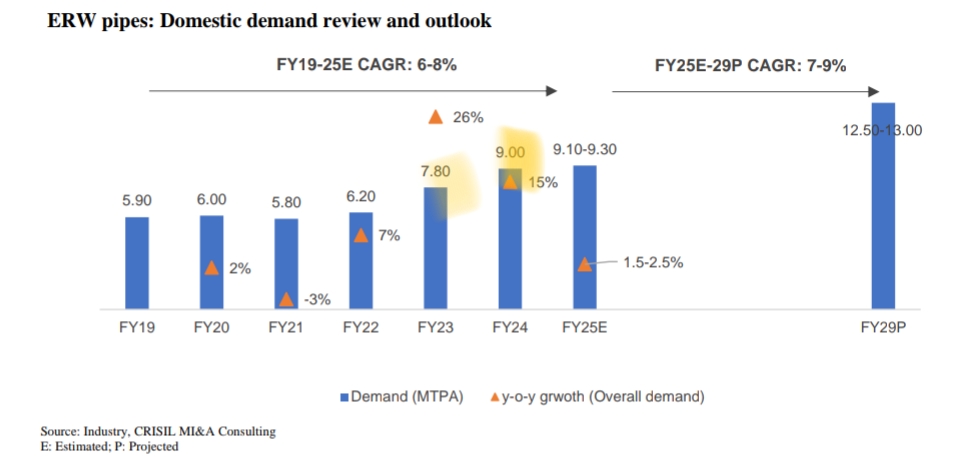

This is from DRHP of Vibhor steel tubes… here it stated as demand for ERW Pipes as of FY25 is 9 mtpa + their would be export market as well, so demand is almost maching installed capacity if Equirus is correct + industry is expected to grow at 7-9% CAGR for next few years (so feel not much over capacity issues in this segment)

- So for asset turnover… their asset turnover is lower because they are running at just 35-40% capacity utilisation… from last 3-4 years they are doing Capex & increasing capacity at full pace thatwhy their Asset turnover are lower + their WC cycle was worsen cause of such huge capex

They can match asset turnover of peers once their capacity utilisation reaches above 60%; also they are now Focusing on normalising WC cycle this can lower total assets (lowering inventory & Receivables + paying debt from that) and Asset turnover can increase drastically due to this + Deleveraging can lead to ROE & ROCE inching upward (above 20% can easily possible if management walk the talk)

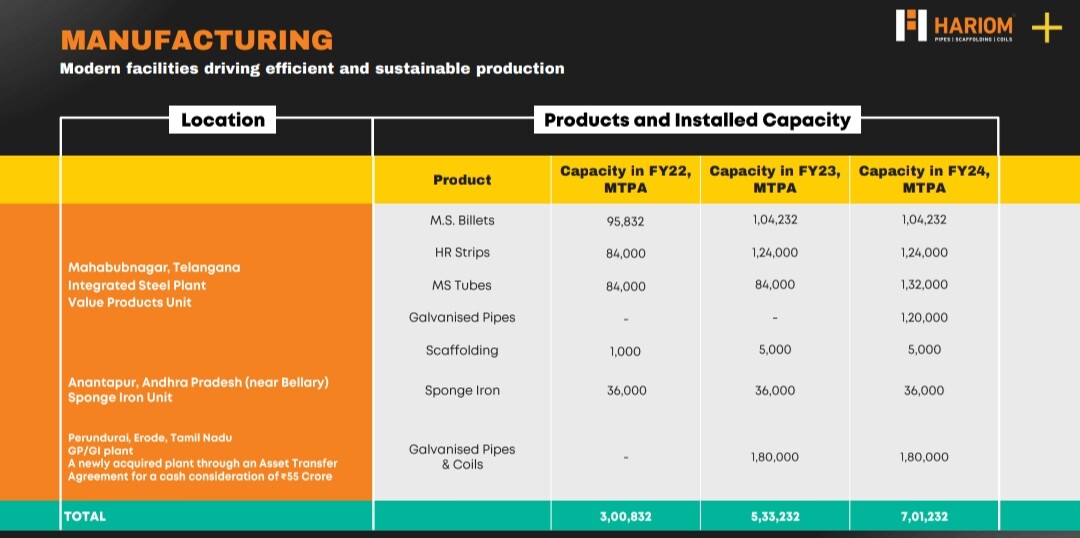

Last 3 yr capacity:

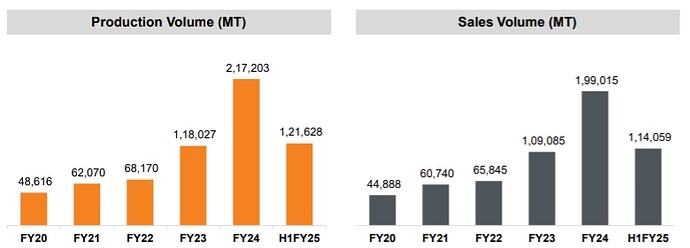

Last 3 year volume:

Hope I can answer ur query… open for future discussion

Disc: Invested & Biased

| Subscribe To Our Free Newsletter |