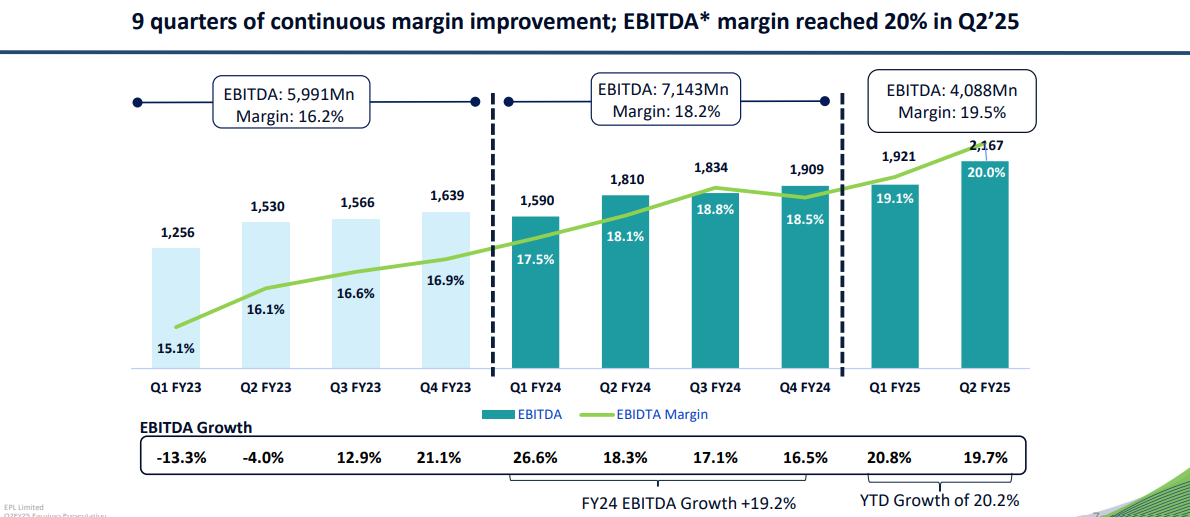

Reversion-to-mean and operating leverage playing out superbly here! Revenue growth at 8%, but EBITDA/PAT has grown 20%/70% respectively (YoY).

Gross margin up from ~54% to ~60% and the prior front-loading of expenses which had been depressing profits is reversing (Interest + depreciation has stabilized over the last 4 quarters, while revenue is growing).

Business momentum looking good (personal care and recyclable tubes).

PS: Invested

| Subscribe To Our Free Newsletter |