Special Situation: Open Offer + Merger via share-swap

Summarizing the special situation opportunity in Cigniti Tech:

Current Situation

- Coforge owns 28% stale in Cigniti

- Coforge has made an open offer to acquire up to additional 26% in Cigniti.

- 12 November 2024 is the last date of open offer, Coforge will have 51%-54% shareholding in Cigniti. (There cannot be another open offer for next 1 year)

What happens after this? Coforge will have two options during the next 1 year

-

Option a) Run Cigniti as an independent company until next open offer 1+ years later

-

Option b) Do a merger of Cigniti with Coforge via share swap → The share swap ratio would require approval from minority shareholders.

-

The share swap ratio would require approval from majority of non-promoters

-

Example: Despite holding a 75% stake in Butterfly Gandhimathi, the promoter –Crompton Greaves, failed to secure public investors’ approval for its proposed merger with the company. This is because 72.61% of non-promoters voted against the merger since share swap ratio offered was deemed low.

-

Similarly, if the share swap ratio proposed by Coforge is not deemed appropriate by non-Promoter (i.e. Minority shareholders), then it can be rejected by non-promoter shareholders.

-

Hence, Coforge is likely to offer a fair valuation to minority shareholders

-

Does the current stock price represent a fair value that will be acceptable to minority shareholders? Looks unlikely. Reasons explained below:

-

How’s Cigniti’s Business doing?

- Historical Operating Performance on Growth, profitability and ROE

- Over last 3-years and 5-years, the revenue growth has been 27% and 17% CAGR; this can be considered very good. There are small acquisitions done. Organically the business has grown revenues at 13-14% CAGR over past few years

- PAT growth last 3Y/5Y is weaker at 16%/2% CAGR as margins have come down – this is getting resolved and margins are strongly recovering as explained in next section.

- ROE is v healthy 27%/31% over 3Y/5Y

- Overall, business has done reasonable good

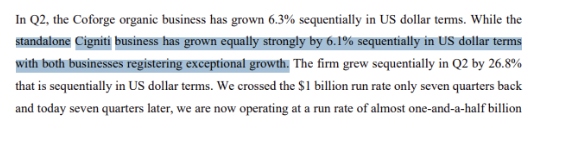

- Cigniti grew 6.1% QoQ in Q2FY25

- This is very strong across growth across all IT companies

- We can assume that Cigniti can grow at 10% going forward, given Last 5-year revenue CAGR of Cigniti is 17%

Source: https://www.coforge.com/hubfs/Transcript-of-Earnings-Conference-Call-Q2-FY25pdf.pdf

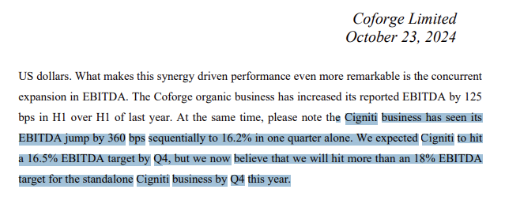

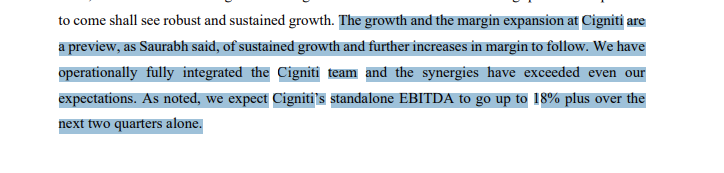

- Big turnaround in Profitability : Cigniti EBITDA margins are expected to go to 18% by Q4FY25 and will be 18%+ for FY26

- Cigniti had 12% margins in FY24.

- It is a fair assumption that Cigniti will have 18% EBITDA margins in FY26,

- This margin expansion from 12% to 18% can lead to 50% increase in EBITDA

- Valuation – Done at CMP of 1415 (Market Cap of 3,800 crores)

a) EV/EBITDA approach

- If we very conservatively assume 10% revenue growth in FY25 and FY26, FY26 revenue can be 2,200 crores. Management is very positive on revenue growth outlook of Cigniti.

- With 18% EBITDA margin on 2,200 crore, it can mean ~400 crores of EBITDA in FY26

- Cigniti is net cash company with cash of ~400 crores

- Market Cap is 3,800 crores

- EV = 3800 – 400 = 3,200 crores

- EV/EBITDA for FY26 = 3200/400 = ~8x

b) P/E approach

- FY 26 P/E Calculation

- FY26 EBITDA =400 crores

- Interest income of 20 crores @5% on 400 crores cash

- Depreciation expense of 33 crores, same as TTM reported

- PBT = 400+20-33 = 387 crores

- Tax = 97 crores@25%

- FY26 PAT = 290 crores

- FY26 P/E = 13x

- This probably makes Cigniti the cheapest company IT services, with one of the the best management team (i.e. Coforge leadership team)

-

Where does the peer group in IT trade at?

- Cigniti’s parent co., Coforge, trades at TTM P/E of 68x (screenshot below)

- Even if we assume 25% EPS growth for FY25 and FY26, then parent Coforge’s FY26 P/E is 43x

Fellow VP’ers

- What’s a fair valuation for Cigniti for minority shareholders?

- Is 13x a fair multiple for Coforge to buy-out the 49/46% minority?

- Will minority shareholders accept this?

- Will they demand a better exit multiple than 13x P/E?

- If yes, will it be 20x or 25x? Or will they demand a valuation closer to Coforge’s valuation of 43x?

Disclosure: Assume that I am biased and may have vested interest in the company, hence please do your own due diligence. I may also change my mind about the company at a future date without being able to update on the forum. This should be viewed as a pure analytical exercise and assessing special situations and not as a reccomednation.

| Subscribe To Our Free Newsletter |