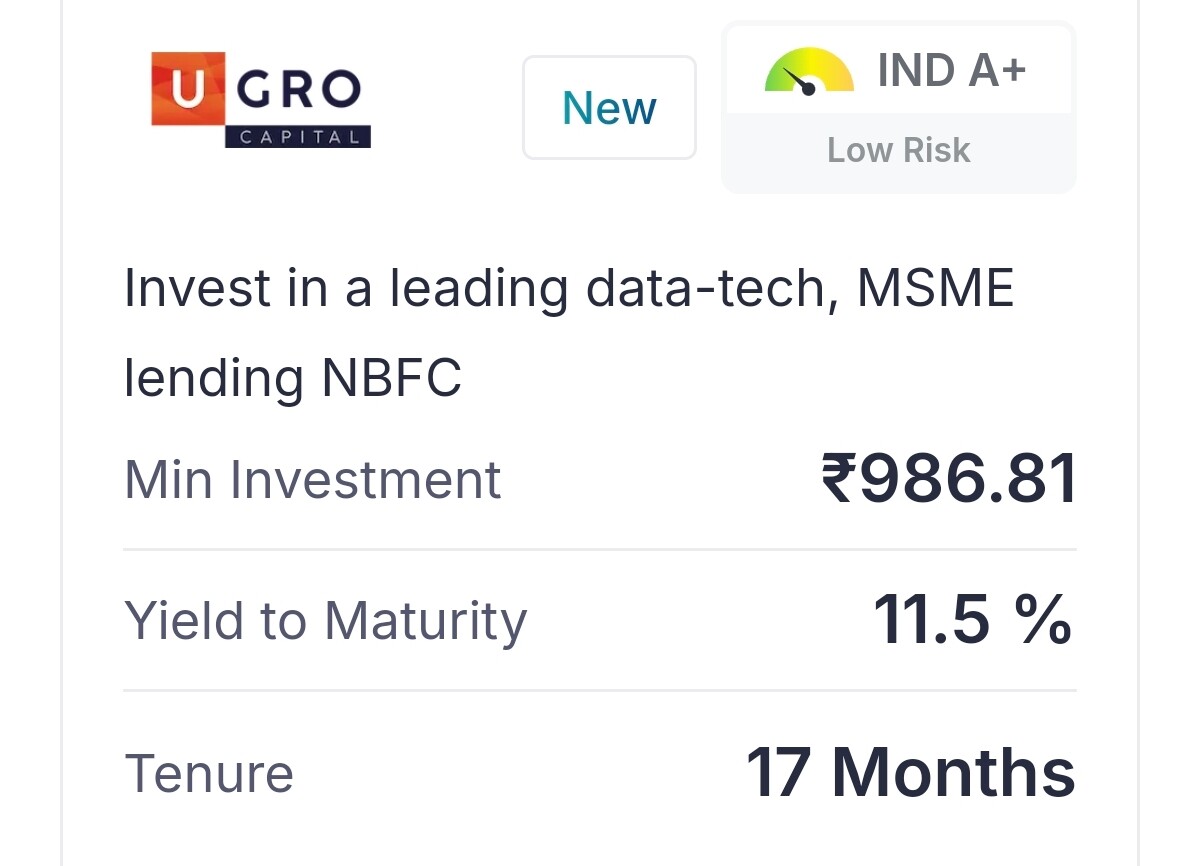

From a shareholder’s perspective, the significant increase in yield to 11.5% for this investment in U Gro Capital could indicate rising borrowing costs for the company. While this higher rate may help attract more retail investors in the short term, it raises questions about U Gro’s financial strategy and cost structure.

For shareholders, such high yields could mean either a squeeze on profit margins or a potential increase in the risk profile of the company’s lending book, especially if they pass on these costs to MSME borrowers who may already be under financial pressure. In the long term, sustained high yields might impact profitability, dividend payouts, or even share value if U Gro faces challenges in maintaining healthy growth without compromising asset quality.

Could anyone explain the reasons behind such a steep increase? It would be helpful to understand if this is specific to U Gro or an industry-wide phenomenon for MSME lenders. Knowing this could provide insights into the future trajectory and risks associated with investments in this sector.

| Subscribe To Our Free Newsletter |